Release of Commercial Goods

Memorandum D17-1-4

Note to reader

Canada Border Services Agency is currently reviewing this D-memo. It will be updated in the context of the CBSA Assessment Revenue Management (CARM) initiative and made available to stakeholders as soon as possible. Find out about CARM.

Ottawa,

This document is also available in PDF (748 KB) [help with PDF files]

In brief

This memorandum replaces Memorandum D17-1-4 dated . The following changes have been made:

- Updated timeframes for release of commercial goods. Timeframes listed in Appendix B are no longer valid and have been removed.

- Removed references to legacy Other Government Department (OGD) release service options: SO463 and SO471 and included information for the Integrated Import Declaration (IID) release service option.

- Updated and added additional information related to release processing for "hand-carried goods" (HCG), paragraphs 112 thru 120.

- Added information on non-terminal offices (NTO) and the procedures to seek release in those instances.

- New information added regarding the e-longroom process.

- New information added regarding returning Canadian vehicles.

- Shifted focus of the entire document from paper release processing to electronic processing of release documents.

- Added procedures for release processing when corrections/cancellations are required, post release and after final accounting.

- Removed Appendix E: Sample of a Pre-arrival review system (PARS) Lead Sheet and Appendix F: PARS Consist Sheet and Stack Manifest.

- Added section about the consolidation of release documents.

- Various minor policy updates and clarifications throughout the document.

This memorandum outlines and explains the terms and conditions for the release of commercial goods from the Canada Border Services Agency.

Table of contents

- Legislation

- Guidelines and general information

- Release prior to payment privilege

- Business number

- Transaction number

- Electronic transmission

- Customs brokers

- CBSA Offices with no licensed customs brokers

- Hours of release: regular office hours

- After hours procedures

- E-longroom

- Inland alternate service

- Non-terminal office

- Compliance verification

- Release of goods

- Low value goods

- Courier low value shipments

- Postal importation

- Customs self-assessment

- Temporary importations

- Returning canadian vehicles

- Form C6, Permission for special purposes

- Timeframes for the release of goods

- Proof of release

- Release options

- Integrated import declaration

- Pre-arrival review system

- Release on minimum documentation

- Form B3-3

- Documentation requirements for release

- Electronic transmission

- Paper release requests

- Release processing

- Consolidated release documents

- Corrections

- Form A48

- Corrections to importer bn using form A48

- Corrections to transaction number using form A48

- Corrections to ccn, container number(s) using form A48

- Corrections to the customs office of release or sub-location code using form A48

- Corrections to invoice information

- Corrections after final accounting

- Cancelling

- Exceptional processes

- Release rejected, not on file, or not yet reviewed

- Split shipments: air mode

- Short-shipped goods

- Short-shipped goods processing

- Short-shipped goods documentation

- Known short shipments

- Known short shipments documentation

- Hand-carried goods release process

- Qualifying shipments authorized to use the HCG release process

- HCG carrier codes

- Additional information

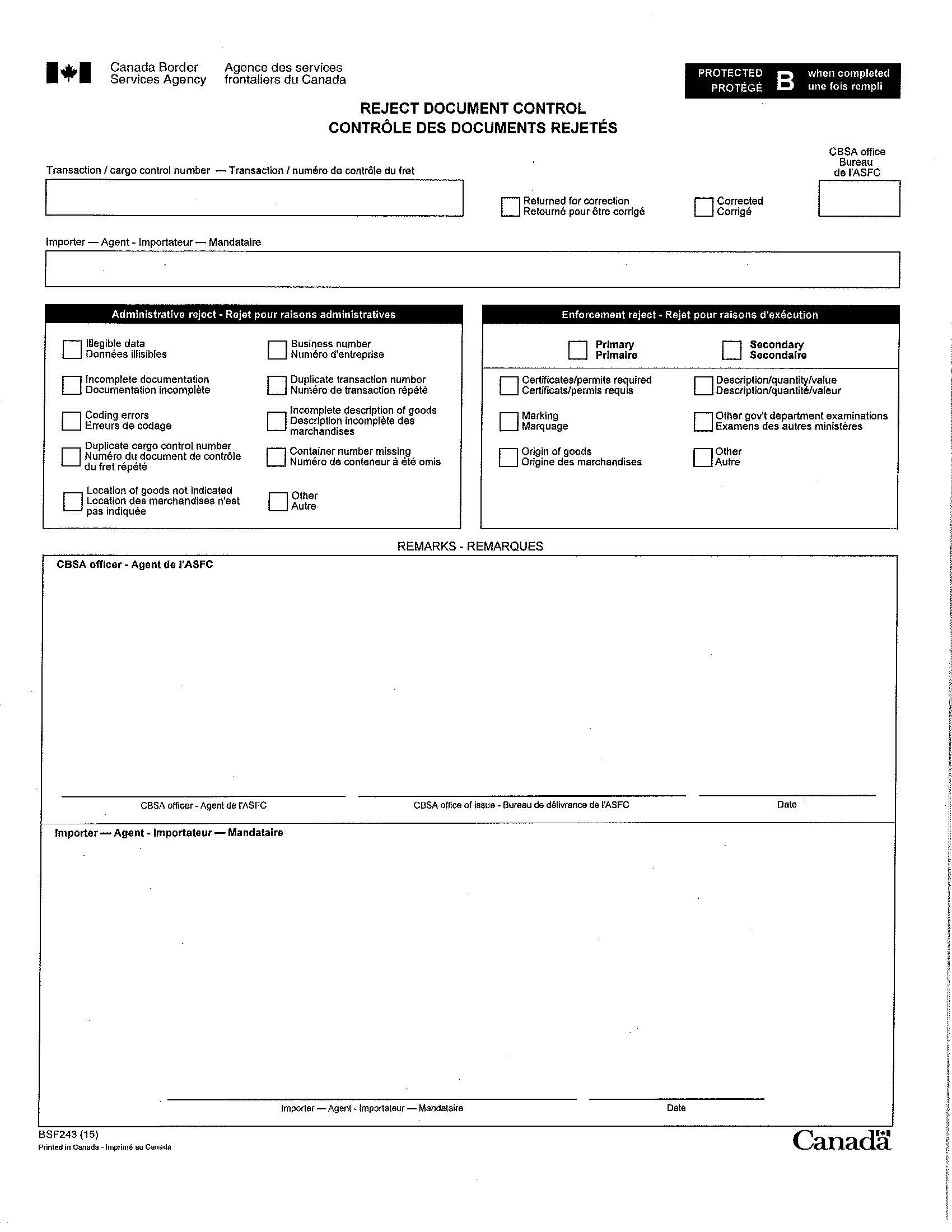

- Appendix A: Form BSF243 (Y50), Reject Document Control

- Appendix B: Exception Lead Sheet

- Appendix C: Release Information Sheet

Legislation

Importers and customs brokers who want to obtain release of goods must account for them as described in sections 32 and 33 of the Customs Act. In addition, goods will not be eligible for release until the goods have been reported in accordance with section 12(1) and 12.1 of the Customs Act (unless otherwise exempt from reporting) and the goods have arrived at the destination release office.

Guidelines and general information

1. Importers and customs brokers can obtain release of commercial goods from the CBSA by:

- presenting a properly completed accounting document, Form B3-3, which accounts for the duties owing on the goods; or

- submitting a properly completed interim accounting document (release request), along with all required supporting documentation (see paragraph 58)

Release prior to payment privilege

2. Release prior to payment (RPP) privilege allows importers or customs brokers to submit an interim accounting document (herein used interchangeably with release or release request) to obtain release of goods before duties and taxes are paid. Importers or customs brokers may utilize RPP if they post security with the CBSA, account for the goods within the prescribed time limit, and pay duties and taxes owing in full by the due date. Refer to Memorandum D17-1-8, Release Prior to Payment Privilege and D1-7-1, Posting Security for Transacting Bonded Operations. Refer to Memorandum D17-1-5, Registration, Accounting and Payment for Commercial Goods, for information on customs accounting requirements and payment of duties.

Business number

3. Importers must have a Business number (BN) with an importer account when submitting release information. More information on the BN, including how to obtain a BN can be found in Memorandum D17-1-5, Registration, Accounting and Payment for Commercial Goods, Section 4, Business Number Registration.

Transaction number

4. Each release request is identified by a unique 14-digit transaction number. This transaction number is used to identify shipments at various times throughout the customs process. When using the cash option, a transaction number is assigned by the importer or broker to the documents in the accounting package presented to obtain release of the goods.

5. If the importer or customs broker has posted security with the CBSA, the account security number appears as the first five digits of the transaction number on all accounting documentation. Information on the transaction number is available in Memorandum D17-1-10, Coding of Customs Accounting Documents.

Electronic transmission

6. Release requests must be submitted electronically using Electronic Data Interchange (EDI) unless otherwise exempted. See paragraph (60) for a list of exceptions to mandatory EDI.

7. EDI allows for the electronic transmission of IID, PARS and Release on Minimum Documentation (RMD) release requests directly to the Accelerated Commercial Release Operations Support System (ACROSS). Border services officers (BSO) review the information and transmit the release decision back to the client via the Release Notification System (RNS) and/or eManifest notices system.

8. Advanced Commercial Information (ACI)/eManifest notices offer importers and brokers visibility into the status of the shipment as it travels (in-bond) through Canada. The ‘Reported' notice can be transmitted to importers and brokers when the shipment arrives and is processed at the first port of arrival (FPOA). This notice is available to importers and brokers, as well as carriers and freight forwarders.

9. Clients using EDI must abide by the requirements outlined in the applicable Electronic Commerce Client Requirements Document (ECCRD) or Participants Requirements Document (PRD).

10. Copies of the applicable ECCRD or PRD can be obtained by contacting:

Technical Commercial Client Unit tccu-ustcc@cbsa-asfc.gc.ca

Customs brokers

11. Importers may choose to transact business directly with the CBSA or they may authorize a licensed customs broker to conduct business on their behalf. Customs brokers are not government employees and importers are charged a fee by the brokerage company for their services. The CBSA does not regulate fees charged by brokerage companies.

12. For additional information on customs brokers, see Memorandum D17-1-5 Registration, Accounting and Payment for Commercial Goods.

CBSA offices with no licensed customs brokers

13. Offices which do not have a customs broker physically located on site must still transmit their release requests electronically, unless otherwise exempt from electronic submission. See paragraph (60) for a list of EDI exceptions.

Hours of release: regular office hours

14. The CBSA will process a release request and examine shipments during authorized hours of service. If release is requested outside the authorized service hours, special service charges may apply. Memorandum D1-2-1, Special Services, contains additional information concerning service hours and special service charges. The directory of CBSA office locations and business hours is available by visiting the CBSA website at Directory of CBSA Offices and Services.

15. Release requests may be transmitted electronically 24 hours a day, seven days a week without imposition of special service fees. However, should a shipment require examination, the examination will be conducted in accordance with the related CBSA business hours.

After hours procedures

16. Documentation requirements for goods released outside business hours are the same as authorized hours. Release documents must be submitted electronically unless otherwise exempted. See paragraph (60) for a list of EDI exceptions.

e-Longroom

17. The electronic e-Longroom service offers an alternate way to submit documentation to the CBSA. In lieu of submitting paper documents in person, select documents may be submitted by email using a PDF file.

18. For a list of ports offering e-Longroom services, see e-Longroom - Release. For more information on the e-Longroom process and accepted documents, see Electronic Longroom.

Inland alternate service

19. Under the Inland Alternate Service (IAS) program, a number of small, designated CBSA service sites no longer have a physical CBSA presence. Commercial services for these de-staffed offices are provided by larger offices, referred to as "hubs." Local importers and customs brokers provide documentation to the CBSA for processing at the hub by mail, courier, fax, email, or EDI. The hub is responsible for processing release requests and examining shipments where required. See paragraph (60) for a list of EDI exceptions.

20. Importers at an IAS site should contact the hub office, as indicated in the directory of CBSA offices, located here: Inland Alternate Service.

Non-terminal office

21. The CBSA does not accept electronic release requests at NTO's. Importers seeking release at these offices must submit the release request in paper format. Please refer to the CBSA's website for a list of NTOs.

Compliance verification

22. The CBSA monitors all release and accounting documents for completeness and accuracy of information. Importers must comply with the statutory or regulatory provisions for release to the same extent as final accounting.

23. Information is verified at the time of release by the CBSA to ensure it meets government requirements. Incorrect or incomplete documents will be returned for correction with a Form BSF243 (Y50), Reject Document Control (see Appendix A), indicating the reasons for rejection. For documents submitted through EDI, the CBSA will transmit this form to the importer or customs broker electronically. The goods rejected on a Y50 will not be eligible to be released until the CBSA receives the corrected documents or data.

24. The CBSA wants to facilitate the release of goods whenever possible and will not delay release requests due to minor errors in the paperwork. CBSA may release the shipment and issue a "reject document", if the error is not relevant to the release decision. However, the BSO retains the right to ask for information to ensure the goods comply with all applicable legislation.

25. Voluntary disclosure of errors to the CBSA by importers or customs brokers is encouraged at all times. Such disclosure may lead to waiver of penalties and a reduction of interest. For more information on voluntary disclosure, see Memorandum D11-6-4 Relief of Interest and/or Penalties Including Voluntary Disclosure.

Release of goods

Low value goods

26. Memorandum D17-1-2, Reporting and Accounting for Low Value Commercial Goods and D8-2-16, Courier Imports Remission outline the requirements for the release of low value goods.

Courier low value shipments

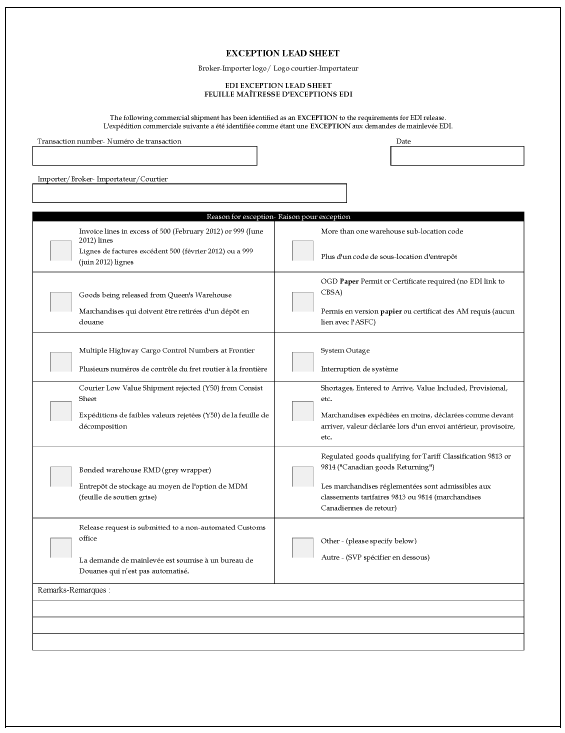

27. Goods imported through the Courier Low Value Shipments (CLVS) Program, that are removed post-arrival by the CBSA from the cargo/release list, must be submitted as a paper release request or accounting package (B3-3) to the CBSA office that issued the reject notice. An EDI Exception Lead Sheet (Appendix B) must accompany the paper release package.

28. Should a CLVS Program participant identify that a shipment no longer qualifies for report and release privileges under the CLVS Program prior to the shipment's arrival in Canada, there is an obligation to provide ACI/eManifest pre-load/pre-arrival data to the Agency. In addition, electronic release or accounting package (B3-3) must also be submitted.

29. For more information on the CLVS program, see Memorandum D17-4-0, Courier Low Value Shipment Program.

Postal importation

30. In the case where commercial goods have been imported through the mail stream and the value for duty exceeds the Low Value Shipment (LVS) threshold, the importer/owner or broker can obtain release of the goods by presenting the appropriate documentation to a CBSA office or submit an electronic release request to CBSA using "E14-" as the carrier code in the Cargo Control Number (CCN) field. This will ensure a related cargo document is not required to release the shipment. Where the importer/owner or broker has posted the required security for release prior to payment privileges, electronic release is permitted. Form B3-3, Canada Customs Coding Form, Type M (Mail) payment is required for importers who have not posted security for release prior to payment. Once the release documentation has been approved, the CBSA commercial office advises the applicable International Mail Centre to release the mail shipment to the CPC for delivery.

31. For more information on Postal processing, see Memorandum D5-1-1, International Mail Processing System.

Customs self-assessment

32. Customs self-assessment (CSA) streamlines the import process for pre-approved Canadian importers by using their internal business systems and processes in place of the traditional customs process. Under CSA, most elements of the import process from release, accounting, adjustment and payment of duties are modified.

33. CSA-approved importers may use IID, PARS and RMD service options for release when goods/carriers do not qualify for the CSA process.

34. For more information on CSA, see Memorandum D23-3-1, Customs Self-Assessment Program for Importers.

Temporary importations

35. Memoranda D8-1-4, Administrative Procedures Related to Form E29B, Temporary Admission Permit, and D8-1-7, Use of A.T.A. Carnets and Canada/China-Taiwan Carnets for the Temporary Admission of Goods, outline the documentation requirements for goods temporarily imported into Canada.

Returning canadian vehicles

36. Canadian goods returning to Canada, (including Canadian registered vehicles), from a foreign country are considered an importation by the CBSA.

37. If the vehicle is being transported back to Canada by someone other than the importer/owner, the Canadian resident may utilize the services of a customs broker to release and account for their vehicle and any goods contained therein. A broker may submit an EDI release request to CBSA for the purposes of getting release of the vehicle. One invoice line is to be used for the Canadian registered vehicle and additional lines for additional goods. The HCG release process may be utilized depending on the individual that is transporting the vehicle, or when the vehicle is being driven back to Canada by a third party service provider (e.g. drive-away company) that is not a commercial carrier. Refer to paragraphs (112-120) for more information on the HCG release process.

38. If the importer/owner hires a transportation company to provide transport of the vehicle back to Canada, the importer/owner may utilize the services of a customs broker. However, the HCG release process may not be used, as ACI (cargo and conveyance) information will be required and the release request must be linked to the cargo document. For more information on returning Canadian vehicles, see Vehicles transported back to Canada from the U.S. by commercial carrier.

Form C6, Permission for special purposes

39. A CBSA Regional Director General may authorize a paper Form C6, Permission for Special Purposes in the following situations:

- to allow raw leaf tobacco to be delivered directly to a licensed packer or licensed manufacturer to determine the standard weight prior to preparation of the final accounting

- to allow imported spirits to be delivered directly to a distillery to determine the quantity and strength prior to preparation of the final accounting

- to obtain release of imported bulk cargoes, which have to be weighed or gauged prior to preparation of the final accounting documentation or

- allow an importer or customs broker to open a parcel in a warehouse to get documents that are needed to obtain release of goods

40. The importer or customs broker should state on the form why permission is required before submitting it to the local CBSA office.

Timeframes for the release of goods

41. Goods are eligible for release upon arrival at the final destination in Canada (i.e. arrival at the location where the importer is seeking release).

42. Shipments will be eligible for release only after all related cargo documents attain "arrived" status. Cargo will be considered "arrived" in CBSA systems only when the cargo reaches the port of destination specified in the cargo document. Before release can occur, all associated cargo(s) must be accepted and attain arrived status before a release decision (via RNS or eManfiest notices) is transmitted to the importer or broker.

43. Importers seeking release using PARS, or the IID release service options may submit their release to the CBSA as early as 45 days for PARS and 90 days for IID, before the goods have arrived at their final destination (arrived at the customs office of release or related sufferance warehouse).

44. Importers seeking release using the post-arrival RMD release option or Form B3-3 must submit their release request to the CBSA after the goods have arrived at their final destination (arrived at the customs office of release or related sufferance warehouse).

45. It should be noted that when carriers, freight forwarders or agents provide a Cargo Control Document (CCD) to the importer or customs broker before the goods arrive, they must specifically advise the importer or customs broker that the goods have not yet arrived. The carrier or freight forwarder must also provide an estimated time and date of arrival for the goods. A penalty may be issued to the carrier or freight forwarder if the CBSA refers goods for examination and discovers that the importer or customs broker was not advised of the arrival status of the goods (i.e., the goods were not available for examination). For more information, please refer to Memorandum, D3-1-1, Policy Respecting the Importation and Transportation of Goods.

46. For more information on the cargo reporting requirements please refer to: Memorandum, D3-2-1 Air Pre-arrival and Reporting Requirements, Memorandum, D3-3-1 Freight Forwarder Pre-arrival and Reporting Requirements, Memorandum, D3-4-2 Highway Pre-arrival and Reporting Requirements, Memorandum, D3-5-1 Marine Pre-load/Pre-arrival and Reporting Requirements and Memorandum, D3-6-6 Rail Pre-arrival and Reporting Requirements.

Proof of release

47. As per Section 31 of the Customs Act, no goods shall be removed from a customs office, sufferance warehouse, bonded warehouse or duty free shop by any person other than an officer in the performance of his or her duties under this or any other Act of Parliament unless the goods have been released by an officer or by any prescribed means. Proof the goods have been authorized for release take the form of the following:

- An RNS released message or ACI/eManifest released notice is received directly from CBSA as an RNS participant or ACI/eManifest notice participant or

- An RNS released message or ACI/eManifest released notice is received through an intermediary such as a dedicated service provider or customs broker or

- A released stamped copy of the CCD/manifest, or release information sheet

48. For more information on sufferance warehouses and when goods can be removed from a warehouse, see Memorandum D4-1-4, Customs Sufferance Warehouses.

49. An unaltered RNS release message printed directly from CBSA can be used to show proof of release to a warehouse operator, in the event the goods were released by CBSA, but the warehouse where the goods are located did not receive a copy of the RNS release message. If the warehouse has concerns the RNS release message may be fraudulent, they may contact the applicable port and verify, or send an RNS query message using the CCN or transaction number, which will inform them of the status of the shipment.

Release options

50. Several types of release requests are available:

- IID

- PARS

- RMD and

- Form B3-3

Integrated import declaration

51. The IID allows importers and brokers to submit interim accounting documentation to CBSA for review and processing to obtain release of goods. The IID can be submitted electronically up to a maximum of 90 calendar days before the goods arrive at the CBSA office of release. One IID document can link up to 999 related cargo control documents using the related CCN, reducing the need for multiple release document submissions.

52. The IID is designed to accommodate the CBSA and Participating Government Agencies (PGAs) data requirements for regulated goods. Importers or brokers will transmit the IID to CBSA and a BSO will review the IID information. Once the BSO has completed their review, the ACROSS system will be updated with a recommendation whether to release or refer the goods for examination. For regulated goods, information will be verified by the applicable PGA(s) and validated on the importers behalf.

53. In accordance with PGA legislative requirements and/or international agreements, in certain exceptional cases, there is a requirement for importers or brokers to submit paper documents with their IID. The Document Image Functionality (DIF) allows importers and brokers to transmit paper Licenses, Permits, Certificates and Other Documents (LPCOs) electronically, as images through EDI. Please refer to the D19 series memoranda for additional information.

Pre-arrival review system

54. PARS allows importers and customs brokers to submit pre-arrival interim accounting documentation to CBSA for review and processing to obtain release of goods. The BSO reviews the PARS information pre-arrival, and updates ACROSS with a recommendation whether to release or refer the goods when they arrive in Canada. Submitting PARS expedites the release or referral for examination process when the goods physically arrive. PARS can be submitted electronically or in paper format up to a maximum of 30 calendar days before the goods arrive at the CBSA office of release.

Release on minimum documentation

55. RMD allows importers and customs brokers to submit post-arrival interim accounting documentation to CBSA for review and processing to obtain release of goods after the goods have arrived in Canada. RMD can be submitted electronically or in paper format and can be submitted any time after the associated cargo(s) attain "arrived" status.

56. Post-arrival EDI RMDs will provide a release decision to the importer or broker within 45 minutes as per published service standards, CBSA Service Standards.

Form B3-3

57. This form is a customs document used to account for imported goods, regardless of value, destined for commercial use in Canada according to sections 6 and 7 of the Accounting for Imported Goods and Payment of Duties Regulations. The CBSA requires this information to verify the value, classification, country of origin, tariff treatment, and exchange rate on imported goods. This data, as well as a breakdown of the duties and taxes owing must be shown on Form B3, Canada Customs Coding Form. For more information on this form, see Memorandum D17-1-10, Coding of Customs Accounting Documents.

Documentation requirements for release

58. An importer or customs broker opting to submit interim accounting documentation must provide the following information to the CBSA, regardless if submitting in EDI or paper format:

- commercial invoice information from a Canada customs invoice or another acceptable supporting document, such as a bill of sale, or both, containing the following:

- vendor's name and address

- consignee/ultimate consignee's name and address

- purchaser's name and address (if other than consignee/ultimate consignee):

- in cases where both a purchaser and a consignee/ultimate consignee are identified on the invoice, the purchaser, not the consignee/ultimate consignee, will be the importer of record

- where only a consignee/ultimate consignee is listed, the consignee/ultimate consignee will be the importer of record

- the party identified as the importer at the time of release must be the party identified as the importer at the time of final accounting

- importer's BN

- clients with more than one RM account must specify the account identifier and enter all 15 characters of the BN (e.g., 123456789RM0003)

- the name of the importer of record must correspond with the name under which the company registered for its RM account

- unit of measure and quantity of goods

- value of the goods and currency of settlement

- detailed description of the goods

- 10-digit HS code for all commodities/lines

- when multiple-page paper invoices are presented, all the HS code(s) must also be shown on the first page

- importers and customs brokers are encouraged to use bar-coded format, if available

- CSA importers, using interim accounting (e.g., PARS, RMD or IID release options) are exempt from providing HS codes at time of release, unless the goods are subject to OGD or PGA requirements

- country of origin of the goods

- transaction number (bar-coded) for paper format as outlined in Memorandum D17-1-10, Coding of Customs Accounting Documents. The requirement for the bar-coded format does not apply to goods released through a sub-agent at a non-terminal CBSA office

- permits, licences, certificates, and/or any other documentation or authorizations required by OGDs/PGAs.

- CCN, both electronic and paper release documents require that a CCN be provided.

Electronic transmission

59. Importers using interim accounting must transmit their documentation electronically as per guidelines stipulated by the applicable IID ECCRD or ACROSS PRD. Contact the Technical Commercial Client Unit, TCCU-USTCC@cbsa-asfc.gc.ca for a copy of the ECCRD/PRD.

60. Certain exceptions to the requirement to transmit interim accounting documentation electronically using EDI apply. The exceptions are as follows:

- goods are subject to the requirements of another government department or agency and the required information cannot be transmitted using the IID

- the invoice for the release transaction contains more than 999 invoice lines

- the release request is for shortages, entered to arrive, value included, provisional, etc. where there is no EDI option

- there is more than one warehouse sub-location code per release transaction

- the CBSA has issued a paper Form BSF243 (Y50), Reject Document Control, to the importer or customs broker for shipments refused clearance through the Courier Low Value Shipment Program

- goods are moved into a bonded warehouse using the RMD option (grey wrapper)

- goods are to be released from a Queen's warehouse

- CBSA or client system outages or

- regulated goods qualifying for tariff classification 9813 or 9814 ("Canadian Goods Returning")

Paper release requests

61. A paper release request will only be accepted if one of the above exceptions apply. An EDI exception lead sheet (Appendix B) must accompany the paper release package indicating the applicable exception. The BSO retains the right to refuse the paper package if it does not meet one of the exceptions listed in paragraph (60).

62. Importers who are not set-up to transmit electronic release documentation to the CBSA, will be required to submit Form B3-3 in order to obtain release of their goods.

63. For paper submissions of RMD and PARS, the documents must be submitted to the CBSA in the following order:

- EDI exception lead sheet (see Appendix B)

- OGD or PGA required documentation (e.g. permits, licences, certificates)

- CBSA documentation, release information sheet: optional (see Appendix C), invoice(s), and supporting documentation

64. The transaction number or CCN must be in bar coded format on paper release requests submitted to the CBSA. Technical specifications for bar-coded CCNs can be found in Memorandum D3-1-1, Policy Respecting the Importation and Transportation of Goods.

65. When shipments do not arrive within 30 days, in the case of PARS, documents, paper permits, etc., are returned to the importer or customs broker.

Release processing

66. Release requests, whether submitted in EDI or paper formats, are processed in the same manner by the BSO in the ACROSS system and are subject to the same validation, admissibility and risk assessment rules.

67. The exporter provides information on the goods to be imported to the importer or customs broker, e.g., CCN, weight etc. Documentation may include an invoice or bill of lading. The importer or customs broker submits a release request to CBSA. If using IID, the importer or broker can submit the release request a maximum of 90 calendar days before the goods arrive at the CBSA office of release. If using PARS, the release request can be submitted a maximum of 30 calendar days before the goods arrive at the CBSA office of release. If using RMD, it must be submitted after the goods have arrived at the CBSA office of release.

68. Cargo will be considered "arrived" in CBSA systems only when the cargo reaches the port of destination specified in the cargo document. Before release can occur, all associated cargo(s) must be accepted and attain arrived status before a release decision (via RNS or ACI/eManfiest notices) is transmitted to the importer or broker.

69. The BSO reviews the release request, and updates ACROSS with a recommendation whether to release or refer the goods when they arrive, or will make a final decision if the goods have arrived at their final destination in Canada.

70. For importers seeking release at FPOA, once the conveyance arrives at FPOA, all cargo and housebill documents associated to the conveyance will be placed in ‘reported' status. In addition, any cargo or housebill with a port of destination equal to FPOA will be placed in ‘arrived' status. If the release request is on file and in good standing, the corresponding release or refer for examination notices will be transmitted to all relevant parties, including the importer or broker.

71. For importers seeking release in-land at a sufferance warehouse, the warehouse operator will advise the CBSA when the goods have arrived. Once the CBSA accepts and processes the warehouse arrival certification message (WACM), and if the release request is on file and in good standing the corresponding release or refer for examination notices will be transmitted to all relevant parties, including the importer or broker.

Consolidated release documents

72. Importers and brokers are encouraged to utilize functionality available on all release documents that consolidate (group together) imported shipments by the same importer, within the same release document.

73. Multiple shipments with multiple CCNs can be accommodated and transmitted to CBSA using a single release document, if managing shipments in such a manner is beneficial to the importer or broker. Consolidated release documents grouped together into a single release document reduce the number of EDI transmissions and simplify the processing at time of release. All pertinent invoice/release data requirements remain the same, regardless if one or multiple release documents are transmitted.

74. The IID, PARS and RMD release service options allow up to 999 invoices with 999 commodity lines for each invoice to be transmitted if imported by the same importer, and captured in a single release document. More information on the IID or other release option limitations can be found in the applicable ECCRD or PRD.

Corrections

Form A48

75. Importers and brokers submitting interim accounting documentation to CBSA, must present true, accurate and complete information. However, when errors occur, the CBSA will accept corrections to certain data elements using form A48, R.M.D. Correction.

76. Form A48, can only be submitted after release, but prior to final accounting (B3-3).

77. Form A48 can be used to correct any interim accounting document, including IID, PARS and RMD, as well as paper PARS and paper RMD.

78. Form A48 can only be used to correct the following data elements:

- importer BN

- transaction number

- CCN

- container number(s)

- sub-location code

- customs office

79. The CBSA will only process a form A48 that contains the proper supporting documentation, as described below. Importers or customs brokers are encouraged to submit form A48 to the CBSA as soon as the error is discovered to avoid the possibility of late accounting penalties.

Corrections to importer BN using form A48

80. A change to the BN after the goods have been released poses a higher level of concern to the CBSA. Such requests may result in additional questioning regarding why the error occurred. In addition to form A48, a waybill, purchase order, commercial invoice (not Canada Customs Invoice) or a similar document which clearly establishes that the claimant is the true importer of record, must be presented as supporting documentation.

81. The A48 is not to be used for changes to the importer BN once final accounting has been submitted to the CBSA. For procedures on correction to the importer BN after final accounting, please refer to Memorandum D17-2-3, Importer Name/Account Number or Business Number Changes.

Corrections to transaction number using form A48

82. A completed form A48 from the proper customs broker (or designate) responsible for the accounting will be required. The A48 must be signed by both customs broker managers (or supervisor/senior staff person) and attached to a hard copy paper release package or B3-3 "C" type entry. The original date of release will be used as the date of release for the corrected transaction. Sub-agents acting on behalf of another customs broker must ensure they provide the primary customs broker's bar coded transaction number.

Corrections to CCN, container number(s) using form A48

83. When providing a correction to the CCN(s), the client must provide the corrected CCN(s) on form A48. A paper copy of the cargo control document can be provided. The correct CCN(s) and/or container number(s) must be in a valid cargo status for purposes of release.

84. The IID does not contain a container number(s) data element. Importers or brokers cannot send this data element when submitting the IID to CBSA and, therefore, form A48 should not be submitted to CBSA for the purposes of correcting container numbers on the IID.

Corrections to the customs office of release or sub-location code using form A48

85. Form A48 requesting a change to the CBSA office of release and sub-location code are to be submitted to the CBSA office where the goods are physically located and will only be accepted if the goods are still under CBSA control (i.e. they have not been removed from the sufferance warehouse).

86. An RNS message and/or ACI/eManifest notice will be generated by CBSA for the client and the applicable sufferance warehouse.

Corrections to invoice information

87. Form A48 is not to be used to make corrections to invoice information.

88. Importers and brokers can make corrections to invoice information using the IID, up until the IID has been released by CBSA. Corrections to invoice information can be completed using the "amend" function available only on the IID. Details on the amend function can found in the IID ECCRD. PARS and RMD corrections to invoice information can be completed electronically up until the associated cargo has attained reported status.

89. If a correction is required to invoice data after release and before final accounting, the importer or broker must submit a paper RMD release package (in a salmon wrapper) with the correction(s) highlighted. The same transaction number should be used as the original release. The BSO will cancel the original transaction and enter the new information based on the paper RMD release package presented.

Corrections after final accounting

90. Changes requested to interim accounting after final accounting (B3-3) has been submitted will only be considered in circumstances where the goods are still under CBSA control in a sufferance warehouse (e.g., changes to CCN, sub-location code or container number). If accepted, the importer or broker must submit a paper RMD release package (in the salmon wrapper) with the original transaction number and the correction(s) highlighted.

91. Depending on the correction, an RNS message and/or ACI/eManifest notice may be generated by CBSA for the client and the applicable sufferance warehouse.

Cancelling

92. Importers or brokers can electronically cancel a release request at any time before associated cargo(s) linked to the release have been reported to CBSA.

93. Importers or brokers seeking to cancel a release request, after the associated cargo documents have been reported or arrived must do so by requesting a cancellation in writing on a company letter head explaining the reason for the cancellation. Similarly, if the release request has been released, but a B3-3 has not been submitted, the same procedures apply.

94. In cases where a cancellation to a release request has been requested after final accounting has been submitted, consideration to this request will be given depending on the circumstances.

Exceptional processes

Release rejected, not on file, or not yet reviewed

95. If a shipment enters arrived status before the release request has been processed, a small delay can be expected until the BSO reviews the transaction(s) and makes a release or refer decision. In most cases, the shipment is released with little delay.

96. When a shipment arrives at its final destination and a release request is not on file, the goods will not be released until the release request is submitted and processed accordingly. In the highway mode, cargo/housebills which have attained arrive status at the FPOA are normally released when a release request is on file and in good standing. If the importer or broker failed to submit the release request the goods may not be released at FPOA (this scenario is commonly referred to as Failed PARS). The carrier and importer/broker have two options to have the goods released.

- The goods can be held at the FPOA until the release request is submitted and processed by the CBSA or

- The shipment can be moved to an in-land location for release at a sufferance warehouse. If the goods are moved in-land the carrier should notify the importer or broker of the change in location of the release office

97. In cases where a shipment arrives and the release request is in a reject status, the onus is on the importer or broker to make the correction before release can occur. A note is often provided in the reject message identifying the cause of the reject and the corrective actions that must be taken.

Split shipments: air mode

98. Please refer to Memorandum D3-2-1, Air Pre-arrival and Reporting Requirements for information regarding split shipments in the air mode.

Short-shipped goods

99. Goods are "short-shipped" when the quantity of goods originally reported to the CBSA is different from that received by the importer or customs broker. In the event of a full shortage, Entered to Arrive (ETA)/Value Included (VI) should not be used. There are two shortage situations:

- the total number of packages originally reported does not match the number of packages received by the consignee or importer. These short-shipped goods can be documented on an ETA release request; and

- the number of articles originally reported as contained in a package does not match the contents of the package. These short-shipped goods can be documented on a VI release request

100. Goods cannot be released under ETA and VI release options when:

- the importer or customs broker is aware that the entire quantity of the goods reported on the invoice will not be in the shipment when it arrives in Canada

- the BSO finds that the quantity reported does not match the quantity found during examination of the goods

- the goods are reported to be on back-order or

- the goods are bonded warehouse shortages. Refer to Memorandum D7-4-4, Customs Bonded Warehouses

Short-shipped goods processing

101. ETA and VI shipments must be presented as paper release requests only, regardless of the service option used for the original release request.

102. If a shortage is discovered after release but before final accounting, the importer or customs broker has two options:

- to account for the total quantity and have the balance of the goods released as an ETA or VI when they arrive or

- to provide the CBSA with evidence of the shortage with the final accounting document and account for the goods on hand only. When the remaining goods arrive, they should not be reported as a shortage. Instead, standard release procedures will apply

103. When goods are released as an ETA or VI, the accounting time limits will start on the date of release of the first shipment.

104. If the shortage is discovered after final accounting, either the balance of the short-shipped goods may be released as an ETA or VI, or a claim may be made for a refund if the importer does not expect the goods to be delivered at a later date. To obtain a refund, a claim, with evidence of the shortage, must be submitted to any CBSA office in the region where the goods were released. Memorandum D6-2-3, Refund of Duties, contains further information on refund procedures.

Short-shipped goods documentation

105. The documents required to release short-shipped goods as ETA are:

- one copy of the documentation supporting the claim for the shortage, e.g., a shipping order or letter from the shipper/carrier, vendor or manufacturer indicating that the goods were not shipped

- Reference to the original CCD (CCN) and the CCN for the new CCD. When more than one carrier is involved, a loading sheet from the original carrier is required to substantiate the shortage. Note: ACI (cargo and conveyance) data is required for all ETA shipments, and

- two copies of the invoices covering the original shipment. This invoice should contain the following information:

- importer BN

- transaction number of the original shipment

- notation "ETA Shortage"

- indication of which goods were short-shipped and

- original CBSA release office

106. The documents required for short-shipped goods to be released as a VI transaction are:

- two copies of the original documentation supporting the claim for the shortage

- Reference to the original CCD (CCN) and the CCN for the new CCD. Ensure a reference to the original shipment in the description field is required. Note: ACI (cargo and conveyance) data is required for all VI shipments, and

- two copies of an invoice containing an accurate description of the short-shipped goods. This invoice should contain the following information:

- importer/exporter account number or BN of the importer

- transaction number of the original shipment (a new transaction number is not acceptable)

- a notation "VI shortage"

- name of the original CBSA release office and

- invoice page and line number for the original transaction relating to the short-shipped goods

Known short shipments

107. A commodity invoiced as a single transaction may have to be imported in separate loads due to the nature of the shipment. For example, certain machinery, equipment, and large systems such as an oil rig must be shipped in multiple loads over time. In these cases, the entire quantity of goods will be accounted for when the first shipment arrives, and the remainder will be processed on importation as ETA. All the ETA shipments have to be processed within 12 months from the date of accounting of the first shipment.

108. Before the goods arrive, a written request must be submitted to the chief or superintendent at the CBSA office where the first shipment is to be imported. The request should include the following information:

- reason for shortage

- name and BN of the importer

- name of the exporter

- unit of measure and quantity of goods

- value of the goods

- detailed description of the goods

- country of origin

- number of ETAs and

- estimated date(s) of arrival including the completion date

109. If the request is approved, the CBSA will send a letter of authorization to the importer or customs broker and retain the information pending arrival of the first shipment and all ETAs.

110. For the first shipment, the importer or customs broker must submit a paper release request with the letter of authorization to the designated CBSA office.

Known short shipments documentation

111. The documents required for this type of ETA release are:

- a copy of the letter of authorization

- Reference to the CCD, (CCN). Note: ACI (cargo and conveyance) data is required for all ETA shipments, and

- two copies of the invoice(s) covering the original shipment containing the following information:

- importer BN

- transaction number of the original shipment

- name of the original customs release office

- notation "ETA Shortage" and

- actual quantity being released

Hand-carried goods release process

112. The HCG release process provides importers and customs brokers with the option of using PARS, IID, or RMD release options in order to obtain release of commercial goods being transported to Canada by an individual who is not a carrier.

113. The HCG release process is applicable to all modes for qualifying shipments and may be used as an alternative release option to submitting a paper Form B3-3, Canada Customs Coding Form.

114. Release must occur at FPOA. In-bond shipments are not eligible for the HCG release process.

Qualifying shipments authorized to use the HCG release process

115. Commercial shipments qualifying for release using the HCG release process are strictly limited to shipments being transported by an individual who does not meet the definition of a "carrier". Examples of qualifying shipments include:

- Commercial goods carried by paying passengers on board traveller commercial conveyances (bus, taxi, plane, ship, ferry etc.)

- Commercial goods being transported by and accounted for at the FPOA by the owner of a business, or an employee, driving a "not for hire," conveyance

- Commercial shipments being imported into Canada by any individual who does not meet the criteria of "carrier" and who is not required under regulations to have, use and maintain a valid CBSA issued carrier code

- Commercial vehicle or conveyance being imported into Canada where a non-carrier is driving the vehicle into Canada (e.g., where the conveyance is the good being imported – e.g., dealer, drive-away company)

- Importation of new Canadian aircraft

- Canadian aircraft returning to Canada after having been repaired abroad and to account for those repairs and

- Non-Canadian aircraft temporarily being imported into Canada for repairs

Shipments not eligible to use the HCG release process

116. Shipments transported to Canada by a carrier are not considered hand-carried goods. As such, the shipment cannot be released using the HCG release process.

117. If the release request doesn't meet the criteria of the HCG release process, the CBSA will reject the release request and the importer or broker may have to account for the goods using a paper Form B3-3.

HCG carrier codes

118. All release requests require a CCN (assigned by the importer or their customs broker) to be accepted in ACROSS. In order to facilitate the release of qualifying shipments under the HCG release process using any release option, mode specific HCG codes have been designated. The importer or customs broker seeking to use the HCG release process will use the applicable 4 character HCG code in order to assign the required CCN needed to process a release request.

The mode specific HCG codes are shown below:

| Mode specific HCG code | Mode of import/transport | Release option |

|---|---|---|

| HCGA | Air | PARS-EDI, IID, RMD-EDI, B3-3 |

| HCGM | Marine | PARS-EDI, IID, RMD-EDI, B3-3 |

| HCGH | Highway | PARS-EDI, IID, RMD-EDI, B3-3 |

| HCGR | Rail | PARS-EDI, IID, RMD-EDI, B3-3 |

119. For purposes of the HCG release process only, the HCG CCN is not required to be in bar coded format. Hand written HCG CCNs will be accepted providing it is legible. Technical specifications for bar-coded CCNs can be found in Memorandum D3-1-1, Policy Respecting the Importation and Transportation of Goods.

120. Paper PARS or paper RMD release requests will only be accepted if the shipment is excluded from mandatory EDI. Exceptions to mandatory EDI are listed in paragraph 60.

Additional information

121. For more information on release procedures or completing CBSA documents, please call the Border Information Service (BIS):

- from within Canada, call 1-800-461-9999 (toll free) or TTY 1-866-335-3237

- from outside Canada, call 204-983-3500 or 506-636-5064 (long-distance charges will apply)

122. BIS provides recorded information on many common topics 24 hours a day. An agent is available during regular business hours, Monday to Friday (except holidays) from 8:00 a.m. to 16:00p.m. local time, across Canada for more specific inquiries.

123. D memoranda and other CBSA information are also available on the CBSA website.

Appendix A: form BSF243 (Y50), Reject Document Control

Form BSF243 (Y50), Reject Document Control, page 1 of 1

Appendix B: Exception Lead Sheet

Exception Lead Sheet, page 1 of 1

Appendix C: Release Information Sheet

Release Information Sheet, page 1 of 1

References

- Issuing office:

- Importer and Exporter Programs Unit, Program and Policy Management Division

Commercial Program Directorate - Headquarters file:

- 7632-0

- Legislative references:

- Customs Act, sections 31, 32, 33, and 35

- Other references:

- D1-2-1, D1-7-1, D3-1-1, D3-2-2, D5-1-1, D6-2-3, D7-4-4, D8-1-4, D8-1-7, D17-1-2, D17-1-5, D17-1-7, D17-1-8, D17-1-10, D17-2-3, D17-5-1, D19-10-2

- Superseded memorandum D:

- D17-1-4,

- Date modified: