CBSA Invoice Requirements

Memorandum D1-4-1

Note to reader

Canada Border Services Agency is currently reviewing this D-memo. It will be updated in the context of the CBSA Assessment Revenue Management (CARM) initiative and made available to stakeholders as soon as possible. Find out about CARM.

Ottawa, March 1, 2013

This document is also available in PDF (131 Kb) [help with PDF files]

In Brief

1. The increase in the Low Value Shipment (LVS) threshold has been reflected.

2. The name of the issuing office has been updated.

This memorandum explains the CBSA invoice requirements for commercial goods imported into Canada.

Legislation

For the Regulations governing the guidelines and general information contained in this memorandum, refer to the Accounting for Imported Goods and Payment of Duties Regulations available on the Department of Justice Canada Web site at: http://laws.justice.gc.ca.

Guidelines and General Information

1. This memorandum outlines the invoice requirements for Customs Automated Data Exchange (CADEX) participants to present as part of the interim accounting documents for release on minimum documentation (RMD). Non-participants must meet these requirements at the time of final accounting as explained in Memorandum D17-1-5, Registration, Accounting and Payment for Commercial Goods, and Memorandum D17-1-1, Documentation Requirements for Commercial Shipments.

2. For all commercial shipments entering Canada, except those described in paragraph 4, the Canada Border Services Agency (CBSA) requires, in English or French, one of the following:

- (a) a commercial invoice prepared by any means (typed, handwritten, or computer prepared) giving all the information listed in Appendix A;

- (b) a commercial invoice prepared by any means indicating the buyer and seller of the goods, the price paid or payable, and an accurate description including the quantity of goods in the shipment, together with a Canada Customs Invoice, Form CI1, giving the remaining information listed in Appendix A; or

- (c) a fully completed Form CI1 (a sample is shown in Appendix B).

3. Other than described in paragraph 2(b), the exporter, importer or owner, or their agent can add the information required in field 6, and in fields 23 to 25 of the commercial invoice (see Appendix A).

4. Commercial invoices or other documents validating the information provided on the invoices can be used to support the declared value of commercial goods entering Canada if:

- (a) the value for duty is not exceeding CAD$2,500;

- (b) the value of Canadian goods being returned has been increased, but is not exceeding CAD$2,500;

- (c) the goods qualify for unconditional duty-free entry (not including cases where entry is contingent on end use) regardless of the selling price. Goods subject to duty at specific times of the year cannot be considered unconditionally exempt; or

- (d) the goods qualify for the benefit of classification No. 9810.00.00.00 in the schedule to the Customs Tariff.

5. The CBSA is responsible for verifying the accuracy of the data submitted and, if necessary, to begin enforcement and investigative activities. To do this, the CBSA needs to review all relevant documentation. The availability of the documentation at the time of final accounting may significantly affect the nature and extent of the verification, enforcement, and investigative activities undertaken by the CBSA.

6. Although the CBSA is willing to accept importer or owner prepared documentation to assist in obtaining release of commercial shipments, supporting evidence may be necessary. The commercial invoice is the main document the CBSA relies on to provide this evidence.

7. The importer or owner, or agent is allowed seven days from the date of the request to provide the required supporting documentation to the CBSA. This time period may be extended at the discretion of the Regional Trade Director of the CBSA office in the region making the request.

8. When an importer or owner, or agent has submitted inaccurate information or has failed to provide supporting documentation as requested, the CBSA may withhold release pending receipt of supporting documentation. On such occasions, the CBSA normally requires that the exporter or agent prepare a commercial invoice or Form CI1 before authorizing release.

9. The CBSA will not review or approve commercial invoices or privately printed customs invoices. It is the responsibility of the importer or owner to ensure that all the information listed in Appendix A is provided to the CBSA at the time of final accounting (or interim accounting in the case of CADEX participants).

10. The CBSA requires two copies of the non-warehouse documents and three copies of the warehouse documents. The importer or owner also requires one copy for his or her records. (For CADEX participants, the CBSA requires three copies of the non-warehouse invoice documents).

11. Form CI1, Canada Customs Invoice, is available at CBSA offices or on our site at www.cbsa.gc.ca.

Appendix A

Instructions on How to Complete the Canada Customs Invoice or a Commercial Invoice

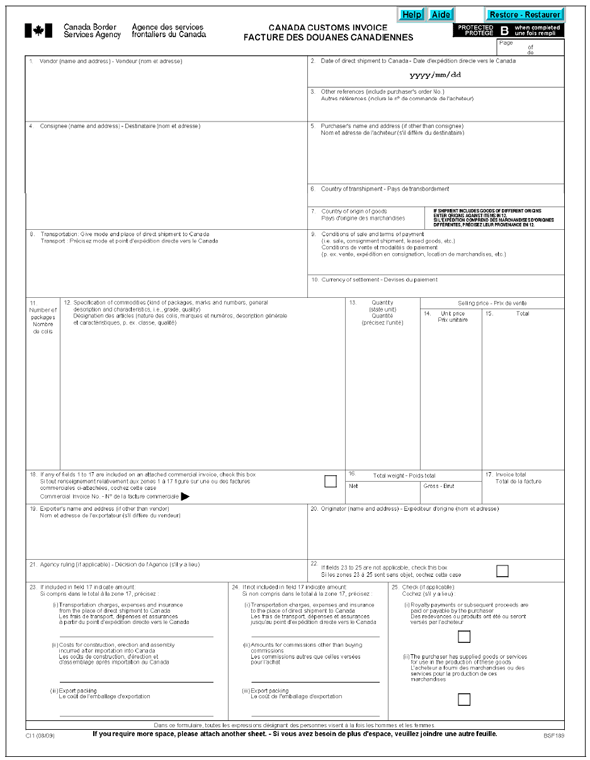

Below is a brief description of how to complete each required field on Form CI1, Canada Customs Invoice, or a commercial invoice. The field name as shown on Form CI1 is in bold face, with similar commercial terms in parenthesis for certain fields.

| Field | Description |

|---|---|

| 1 | Vendor - (seller, sold by, remit to, consignor, shipper) – Indicate the complete name, including the company name if applicable, and address (street, city, location) of:

|

| 2 | Date of direct shipment to Canada - Indicate the date the goods began their continuous journey to Canada. |

| 3 | Other references - Use to record other useful information (e.g., the commercial invoice number, the purchaser's order number). |

| 4 | Consignee - The name and address of the party to which the goods are being “shipped to” as shown on the commercial sales contract (i.e. commercial invoice, bill of sale, or other sales contract). |

| 5 | Purchaser's name and address - (sold to, buyer) – The last known entity to whom the merchandise is sold leased or otherwise transacted. |

| 6 | Country of transhipment - The country through which the goods were shipped in transit to Canada under customs control. |

| 7 | Country of origin of goods - The country of origin of invoiced goods is the country in which the goods have been grown, produced, or manufactured according to criteria laid down for the application of the Customs Tariff or quantitative restrictions, or any measure related to trade. Each manufactured article on the invoice must have been significantly transformed in the country specified as the country of origin to its present form ready for export to Canada. Certain operations such as packaging, splitting, and sorting may not be considered as sufficient operations to confer origin. Note: The origin of goods as applied to the assignment of tariff treatment is dealt with in Memorandum D11-4-2, Proof of Origin. |

| 8 | Transportation: Give mode and place of direct shipment to Canada - Indicate the mode of transportation and the place from which the goods began their uninterrupted journey to Canada. |

| 9 | Conditions of sale and terms of payment -Describe the terms and the conditions agreed upon by the vendor and the purchaser. |

| 10 | Currency of settlement - Indicate the currency in which the vendor's demand for payment is made. |

| 11 | Number of packages - Indicate the number of packages. |

| 12 | Specification of commodities - The following information must be provided:

|

| 13 | Quantity - Indicate the quantity of each item included in the description field in the appropriate unit of measure. |

| 14 | Unit price - (price per article, item amount) – Provide a value in the currency of settlement (as defined under Field 10) for each item described in the description field. |

| 15 | Total - Indicate the price paid or payable in the currency of settlement (as defined under Field 10) for the number of items recorded in the quantity field when they were sold by the vendor to the purchaser. Where there is no price paid or payable for the items recorded in the description field, N/A should be indicated. |

| 16 | Total weight - Show both net and gross weight. |

| 17 | Invoice total - (total value, pay this amount) – The total price paid or payable for goods described on the invoice or on the continuation sheet if used. |

| 18 | Self-Explanatory. |

| 19 | Exporter's name and address - Indicate the name and address of the person or organization shipping the goods to the consignee/purchaser. |

| 20 | Originator - Where the invoice is completed on behalf of a company, the company's name and address must be indicated. The name of the person completing the invoice may also be indicated. Invoices completed on behalf of individuals must indicate the name and address of the person completing the invoice. This field may be left blank if this information is provided elsewhere on the invoice. |

| 21 | CBSA ruling - Give the number and date of any CBSA ruling applicable to the shipment. |

| 22-25 | Indicate the currency used when Field 23 or 24 is applicable. The actual completion of Fields 22 to 25 is self-explanatory with the exception of export packing. The amount of export packing must be indicated if additional packing was required solely for the overseas transportation of goods. Detailed information on the remaining sub-components of these fields can be found in Memorandum D13-4-7, Adjustments to the Price Paid or Payable (Customs Act, Section 48). |

Appendix B

Form CI1, Canada Customs Invoice, page 1 of 1

References

- Issuing office

- Assessment Unit

Trade Policy Division

Trade Programs Directorate

Programs Branch - Headquarters file

- 7600-6

- Legislative references

- Customs Tariff, chapter 98

- Other references

- D11-4-2, D13-4-7, D17-1-1, D17-1-5

- Superseded memorandum D:

- D1-4-1, January 6, 2012

- Date modified: