United States Surtax Remission Order

Customs Notice 18-16

Ottawa, October 11, 2018

Revised on July 10, 2019

Revised on February 13, 2020 (see footnote)

1. This notice provides information on the introduction and application of the United States Surtax Remission Order, 2018-1272, which is intended to minimize the negative effects of the surtaxes on Canadian companies and the economy by providing relief in exceptional situations.

2. The remission order remits the surtaxes imposed by the United States Surtax Order (Steel and Aluminum): SOR/2018-152 and the United States Surtax Order (Other Goods): SOR/2018-153 which were in effect from until (25% in the case of certain steel products, 10% in the case of certain aluminum products and 10% for certain other goods listed in the order) under the following situations:

- Pursuant to section 115 of the Customs Tariff, in respect of the goods listed in Schedule 1, Schedule 2, Schedule 3 and Schedule 4 of the remission order;

- Pursuant to section 115 of the Customs Tariff, in respect of goods classified under tariff item No. 8903.10.00, 8903.91.00, 8903.92.00 or 8903.99.90 in the List of Tariff Provisions set out in the schedule to the Customs Tariff, excluding those that have been exported from Canada and then subsequently re-imported into Canada; and

- Goods temporarily imported into Canada for the purposes of repair, alteration, or storage, including those classified under tariff item No. 8903.10.00, 8903.91.00, 8903.92.00 or 8903.99.90 that have been exported from Canada.

3. The administration of the remission order is the responsibility of the Canada Border Services Agency (CBSA).

Application (Steel and Aluminum)

4. Remission is granted for those goods described in Schedule 1, Schedule 2 and Schedule 3 attached to the remission order under the following conditions:

- (a) in the case of a good listed in Schedule 1, imported into Canada on or after until and subject to surtaxes;

- (b) in the case of a good listed in Schedule 2, it is imported into Canada during the period beginning on and ending on ;

- (c) in case of a good listed in Column 2 of Schedule 3, it is imported into Canada by the importer listed in Column 1 of Schedule 3 during the period specified in Column 3 of Schedule 3, and subject to any other applicable condition listed in Column 4 of Schedule

- (d) no other claim for relief of the surtax has been granted under the Customs Tariff in respect of the good;

- (e) the importer makes a claim for remission to the Minister of Public Safety and Emergency Preparedness within two years after the date of importation.

- (f) the importer files, on request, the evidence or information that the Canada Border Services Agency requires to determine eligibility for remission;

- (g) the importer agrees that it is subject, at any time, including after the remission, to review by the Canada Border Services Agency for the purpose of determining whether the information supplied by the importer under paragraph (c) or (d) is accurate and complete and whether the facts on which the Canada Border Services Agency relied or intends to rely to determine the eligibility for remission remain unchanged in all material respects; and

- (h) at the time when the Canada Border Services Agency conducts the review referred to in paragraph (e), the Canada Border Services Agency must be able to conclude that the information supplied remains accurate and complete and that the facts remain unchanged in all material respects.

- (i) goods described in Schedule 2 must be imported into Canada no later than .

5. All claims for relief of surtax under the remission order for these goods described in Schedule 1, Schedule 2 and Schedule 3 must attach all relevant documents (e.g. B3 form, purchase order, commercial invoice, Canada customs invoice, bill of lading, way bill, etc.) that demonstrate that the goods imported match the description of one of the goods described in Schedule 1, Schedule 2 and Schedule 3 of the remission order.

Application (Other Goods)

6. Remission is granted for goods listed in Schedule 4, under the following conditions:

- (a) the good was imported into Canada on or after until and subject to surtaxes;

- (b) in the case of goods classified under tariff item No. 8903.10.00, 8903.91.00, 8903.92.00 or 8903.99.90 in the List of Tariff Provisions set out in the schedule to the Customs Tariff;

- i. the good was purchased and sold under contract by the importer before May 31, 2018; and

- ii. the good has not been exported from Canada and subsequently re-imported into Canada.

- (c) no other claim for relief of the surtax has been granted under the Customs Tariff in respect of the good;

- (d) the importer makes a claim for remission to the Minister of Public Safety and Emergency Preparedness within two years after the date of importation;

- (e) the importer files, on request, the evidence or information that the Canada Border Services Agency requires to determine eligibility for remission;

- (f) the importer agrees that it is subject, at any time, including after the remission, to review by the Canada Border Services Agency for the purpose of determining whether the information supplied by the importer under paragraph (d) or (e) is accurate and complete and whether the facts on which the Canada Border Services Agency relied or intends to rely to determine the eligibility for remission remain unchanged in all material respects; and

- (g) at the time when the Canada Border Services Agency conducts the review referred to in paragraph (f), the Canada Border Services Agency must be able to conclude that the information supplied remains accurate and complete and that the facts remain unchanged in all material respects.

7. Goods identified in paragraph 6 (b) that have been exported from Canada and then subsequently re-imported into Canada are excluded and thus not eligible for relief of surtax, unless they are temporarily imported into Canada for the purposes of repair, alteration, or storage and the conditions of paragraph 9 are met.

8. All claims for relief of surtax under the remission order for these goods must also attach all relevant documents (e.g. copy of original Form B3-3, bill of lading, sales invoice, waybill, sales contract, etc.) that demonstrate that:

- (a) the good was imported into Canada on or after until and subject to surtaxes; and

- (b) for goods identified in paragraph 6 (b), that the good was both purchased under contract and sold under contract by the importer prior to ;

Application (Goods Temporarily Imported Into Canada)

9. Goods temporarily imported into Canada for the purposes of repair, alteration, or storage are granted remission of surtaxes paid or payable pursuant to the United States Surtax Order (Other Goods). Remission for these goods is granted under the following conditions:

- (a) the goods are exported immediately after having been repaired, altered or removed from storage, whichever occurs last, but no later than twelve months after the date on which the imported goods were released; and

- (b) no other claim for relief of the surtax has been granted under the Customs Tariff in respect of the goods.

- (c) the importer makes a claim for remission to the Minister of Public Safety and Emergency Preparedness within two years after the date of importation;

- (d) the importer files, on request, the evidence or information that the Canada Border Services Agency requires to determine eligibility for remission;

- (e) the importer agrees that it is subject, at any time, including after the remission, to review by the Canada Border Services Agency for the purpose of determining whether the information supplied by the importer under paragraph (c) or (d) is true, accurate and complete and whether the facts on which the Canada Border Services Agency relied or intends to rely to determine the eligibility for remission remain unchanged in all material respects; and

- (f) at the time when the Canada Border Services Agency conducts the review referred to in paragraph (e), the Canada Border Services Agency must be able to conclude that the information supplied remains true, accurate and complete and that the facts remain unchanged in all material respects.

10. All claims for relief of surtax under the remission order for these goods must also attach all relevant documents (e.g. storage contract, repair invoices, alteration invoices, payment for services, etc.)

11. Goods temporarily imported for any purpose other than repair, alteration or storage at time of importation are not eligible for relief under this order.

12. Most goods imported for storage are not eligible for GST/HST relief. However, vessels imported for storage of less than 12 months may be eligible for GST/HST relief under section 7 of the Vessel Duties Reduction or Removal Regulations. When documenting vessels which are eligible for relief under the remission order and under section 7 of the Vessel Duties Reduction or Removal Regulations, GST Code 66 should be entered in Field 35 of the Form B3-3 to provide for GST/HST relief.

Accounting for the relief of surtax where the United States Surtax Remission Order is applicable at time of importation for goods processed in the commercial stream

13. Surtax imposed is still required to be accounted for as described in the United States Surtax Order (Steel and Aluminum) or the United States Surtax Order (Other Goods) and in accordance with Customs Notice CN18-08, with the following modification. Specifically, the amount of surtax owing and therefore remitted, is still required to be entered in Field 39 - SIMA Assessment of Form B3-3, however this amount is not to be included in Field 41 -Value for Tax.

14. For the relief of the surtax, the remission order number is to be entered in Field 26 – Special Authority of Form B3-3.

15. When a surtax amount is relieved by a remission order, code “50” is to be used in Field 32 - SIMA Code of Form B3-3.

Example 1:

On the Form B3-3 the remission order number is entered in Field 26 - Special Authority, 50 is entered in Field 32 - SIMA Code, an amount of $150 entered in Field 37 - Value for Duty, a surtax amount of $15 is entered in Field 39 - SIMA Assessment, an amount of $150 is entered in Field 41 - Value for Tax, and an amount of $7.50 is entered in Field 42 - GST.

Note: This example is for illustrative purposes on how to complete Form B3-3 only. The HS code and surtax rate may not reflect actual goods subject to surtax and also subject to the United States Surtax Remission Order.

16. Please refer to Memorandum D17-1-10, Coding of Customs Accounting Documents, for additional information on completing Form B3-3. Refer to Memorandum D8-4-1, Information Pertaining to Remission Orders, for additional information on remission orders.

Accounting for the relief of surtax where the United States Surtax Remission Order is applicable at time of importation for goods processed in the casual (traveller) stream

17. Form BSF715 or BSF715-1 Casual Goods Accounting Document for the accounting of goods subject to this remission order, will be prepared according to standard procedures without collection of surtax.

Corrections, Re-Determinations, and Refunds

18. Where the remission order is applicable, and an overpayment of surtax has been identified on commercial importations, Form B2, Canada Customs – Adjustment Request may be filed in a regional CBSA office requesting a refund of the overpaid amount under section 74(1)(g)Footnote 1 of the Customs Act. Please refer to Memorandum D17-2-1, The Coding, Submission and Processing of Form B2 Canada Customs Adjustment Request, for additional information on completing Form B2.

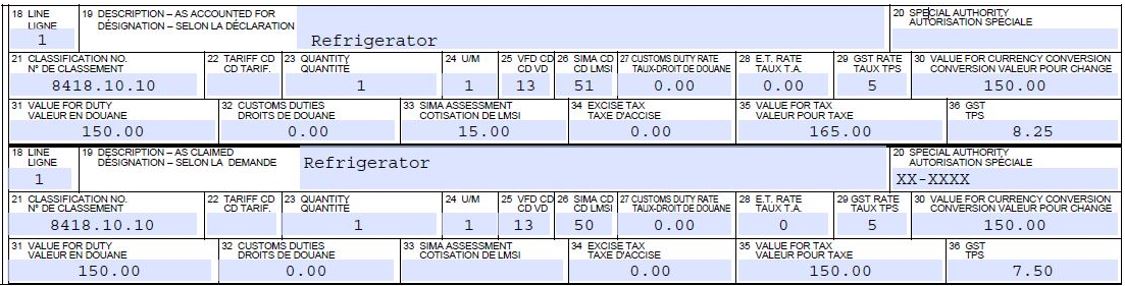

Example 2:

This example shows the format for the line completion of a Form B2 when requesting a refund of duties and taxes for surtax assessed on Form B3-3 Canada Customs Coding Form due to the application of the remission order.

The “as accounted for” section of Form B2 shows the surtax assessed on Form B3-3: code 51 is entered in Field 26 – SIMA Code, an amount of $150 is entered in Field 31 - Value for Duty, a surtax amount of $15 is entered in Field 33 - SIMA Assessment, an amount of $165 is entered in Field 35 - Value for Tax, and an amount of $8.25 is entered in Field 36 - GST.

The “as claimed” portion of Form B2 shows the request for the surtax to be relieved by the remission order: the remission order number is entered in Field 20 - Special Authority, code 50 is entered in Field 26 -SIMA Code, an amount of $0 is entered in Field 33 - SIMA Assessment, an amount of $150 is entered in Field 35 - Value For Tax, and an amount of $7.50 is entered in Field 36 - GST.

Note: This example is for illustrative purposes on how to complete Form B2 only. The HS code and surtax rate may not reflect actual goods subject to surtax and also subject to the United States Surtax Remission Order.

19. A Blanket B2 request may be submitted for requests to refund of the surtax on more than 25 transactions. For the procedures surrounding the preparation and presentation of Blanket B2 Adjustment Requests, please refer to Memorandum D17-2-4, Preparation and Presentation of Blanket B2 Adjustment Requests.

20. Where the remission order was applicable and surtax has been paid on non-commercial importations, Form B2G, Informal Adjustment Request may be sent to one of the CBSA’s five casual refund centres, in accordance with the instructions outlined in Memorandum D6-2-6, Refund of Duties and Taxes on Non-Commercial Importations.

21. The CBSA may re-determine or further re-determine the origin, tariff classification, and/or value for duty on its own initiative or in response to a self-adjustment. In so doing, as with customs duties and taxes, the CBSA may assess any undeclared amount of surtax, or deny remission of surtax that is not eligible.

22. The imposition of a surtax is not subject to an appeal under the Customs Tariff or the Customs Act. Accounting documents are normally reviewed by the CBSA to ensure that the correct amount of surtax was self-assessed by the importer. Determinations, re-determinations or further re-determinations made by the CBSA may be subject to appeal under the Customs Act.

Examinations and Verifications

23. Importations may be subject to examination at the time of importation and to post-release verification for compliance with the Tariff Classification, Valuation, Origin and Marking programs, and any other applicable programs or provisions administered by the CBSA. If non-compliance is encountered by the CBSA, in addition to assessments of surtax, customs duties and taxes, penalties and interest will be assessed, where applicable.

Additional Information

24. Refer to Memorandum D16-1-1, Information pertaining to the application, collection, and adjustment of a surtax, for additional information concerning the administration and enforcement of surtax orders under sections 53(2), 55(1), 60, 63(1), 68(1), 77.1(2), 77.6(2) or 78(1) of the Customs Tariff.

25. For more information on the administration of the surtax orders or remission orders, within Canada call the Border Information Service at 1-800-461-9999. From outside Canada call 204-983-3500 or 506-636-5064. Long distance charges will apply. Agents are available Monday to Friday (08:00 – 16:00 local time / except holidays). TTY is also available within Canada: 1-866-335-3237.

- Date modified: