Accounting for the Harmonized Sales Tax, Provincial Sales Tax, Provincial Tobacco Tax and Alcohol Markup/Fee on Casual Importations in the Courier and Commercial Streams

Memorandum D17-1-22

Ottawa, September 19, 2016

ISSN 2369-2391

This document is also available in PDF (459 Kb) [help with PDF files]

In Brief

This memorandum has been revised to reflect the Harmonized Sales Tax (HST) implementation in Prince Edward Island (PEI) and the reimplementation of the Provincial Sales Tax (PST) in British Columbia.

This memorandum provides information on the collection and accounting of the Harmonized Sales Tax (HST), Provincial Sales Tax (PST), provincial tobacco tax and alcohol markup/fee on all casual goods cleared in the courier and commercial streams, i.e. goods imported for individual use or mail-order goods. For additional information on HST/PST or information on casual goods cleared in the traveller stream, see Memorandum D2-3-6, Non-commercial Provincial Tax Collection Programs. For information on casual goods cleared in the postal stream, see Memorandum D5-1-1, Canada Border Services Agency International Mail Processing System.

Legislation

Canada Border Services Agency Act - Subsections 5(1)(c) and 14(1)

Guidelines and General Information

Definitions

1. Casual goods means any goods imported into Canada other than goods imported for sale or for any commercial, industrial, occupational, institutional or other like use.

2. The HST is the federal Goods and Services Tax (GST) blended with the PST to create a single rate in the participating provinces.

3. The provincial taxes include, unless otherwise specified, the PST, provincial tobacco tax, alcohol markup/fee, and, in Quebec only, alcohol specific tax.

Authority

4. Subsection 5(1)(c) of the Canada Border Services Agency Act authorizes the Canada Border Services Agency (CBSA) to implement agreements between the CBSA and the government of a province to administer a tax or program.

5. Subsection 14(1) of the Canada Border Services Agency Act authorizes the CBSA to enter into or amend an agreement with a provincial government to administer a tax if the agreement is in accordance with guidelines relating to agreements of that kind established jointly by the Minister of Public Safety and Emergency Preparedness and the Minister of Finance of Canada.

Harmonized Sales Tax

6. The Government of Canada has signed agreements with the provincial governments of Nova Scotia, New Brunswick, Newfoundland and Labrador, Ontario and Prince Edward Island (PEI) to have the Canada Revenue Agency (CRA) and the Canada Border Services Agency (CBSA) administer a HST on behalf of these provinces. The HST is applied to casual goods that are destined to New Brunswick, Ontario and Newfoundland and Labrador at a rate of 13%, to PEI at a rate of 14%, and to Nova Scotia at a rate of 15%.

Provincial Agreements

7. The Federal-Provincial Fiscal Arrangements Act and the subsequent Order in Council, P.C. 1992-1268 dated June 11, 1992, provide authority to enter into agreements with the provinces and territories with respect to the collection of the PST, provincial tobacco tax and alcohol markup/fee.

8. Amendments have also been made to the respective provincial acts of those provinces with which the CBSA has agreements, which provide the CBSA with the legal authority to collect and remit the PST, provincial tobacco tax and alcohol markup/fee, and to detain goods should an individual refuse to pay the applicable provincial taxes and/or alcohol markup/fee.

9. To date, agreements to collect the PST, and/or provincial tobacco tax, and/or alcohol markup/fee on casual goods imported by courier or through the commercial stream have been passed with the provinces of Quebec, Manitoba, Saskatchewan, Ontario, New Brunswick, Alberta and British Columbia (see Memorandum D2-3-6).

10. Provinces can exempt certain types of goods from the PST and/or apply the exemptions according to provincial legislation. For assistance in determining the tax status of a good, contact the province's tax authority or the CRA for participating HST provinces.

11. The applicable rates for the PST, HST and provincial tobacco tax on casual goods and rates and calculation formula for the alcohol markup/fee can be found in Memorandum D2-3-6.

General

12. Where casual goods are GST-exempt under federal administrative policy, which provides for exemptions and remissions, the HST, PST, provincial tobacco tax and/or alcohol markup/fee will not be collected.

Application

13. The following describes the application of the HST, PST, provincial tobacco tax and alcohol markup/fee on casual goods.

14. The decision as to whether or not the HST or PST will be collected on casual goods is based on whether the goods are in fact casual, in which case they must be properly reported and accounted for as such. These goods may not be accounted for as commercial goods. For example, where a foreign company sells goods and arranges with a Canadian customs broker or courier to obtain release and account for the duties and taxes on the goods on behalf of the Canadian resident purchasers, if the goods are not for sale or for any commercial, industrial, occupational, institutional or other like use by the purchasers, then the HST or PST must be collected on these goods as required.

15. It should be noted that, while in many cases commercial accounting documents are used for importations of this nature, indicating the foreign or non-resident vendor as the importer on the documents may not in itself make the vendor the importer of the goods for purposes of the Customs Act. In the case where a Canadian resident orders casual goods from a foreign company, even if the goods are imported and accounted for on a Form B3-3, Canada Customs Coding Form, with the name of the foreign company in the importer name field, it is the CBSA's position that the importer of the goods is the person in Canada to whom the goods have been addressed. Therefore, if these goods are casual, the HST or applicable provincial taxes must be collected.

Harmonized Sales Tax

16. The HST applies to all casual goods* that are destined to the participating provinces regardless of their point of entry or release into Canada. In the case of imported commercial goods, only the 5% federal portion of the HST is payable at the time of importation. The remaining provincial portion is payable through the importers' self-assessment provided for in the legislation.

*Note: A point-of-sale rebate on the provincial portion of the HST or of the PST (see Provincial Taxes below) is provided on certain items sold in the participating provinces. Therefore, all casual importations of these exempted items into the participating provinces will be assessed the federal portion of the HST (5%) only. The tariff classification of exempted items that qualify for the point-of-sale rebate in each province can be obtained by contacting the province's tax authority or the CRA for participating HST provinces.

17. The HST may be accounted and paid for in the normal manner for federal duties and taxes, i.e. by means of a Low Value Shipment (LVS) consolidated entry, a Customs Automated Data Exchange System (CADEX) transmission or a Form B3-3. The HST is calculated "off-entry" (on the working papers, invoices) and accounted using a "dummy" classification line separate from the tariff classification line of the goods. "Dummy" classification numbers have been designated for each province (see Appendix A). An example of accounting for the HST can be found in Appendix B. The CADEX format is available through your CADEX representative.

Provincial Taxes

18. The PST, provincial tobacco tax and/or alcohol markup/fee may be accounted for in the normal manner for federal duties and taxes, i.e. by means of a LVS consolidated entry, a CADEX transmission or a Form B3-3.

19. The provincial taxes are calculated "off-entry" (on working papers, invoices) and accounted using a "dummy" classification line separate from the tariff classification and GST lines. "Dummy" classification numbers have been designated for each province and for each type of tax (see Appendix A). Procedures on how to complete the fields in Form B3-3 are explained in appendices B, C and D. The CADEX format is available through your CADEX representative.

20. The application of the PST and provincial tobacco tax on casual goods cleared in the courier or commercial stream is assessed based on the goods being released within the province of residency. For example, casual goods released in Ontario by a courier that are destined to a Quebec consumer will not be assessed the Quebec sales tax as the goods were not released within Quebec. The Ontario HST will not be applicable either, as the goods are not consigned to that province.

21. The following schedule indicates, in general, which provincial taxes the CBSA is authorized to collect on casual goods imported by the courier or commercial stream, and which provincial tobacco and alcohol tax markups/fee the CBSA is authorized to collect on casual goods imported by the courier or commercial stream.

| Province | PST/HST | Tobacco Tax | Alcohol Markup/Fee |

|---|---|---|---|

| Newfoundland and Labrador | HST | No | No |

| Nova Scotia | HST | No | No |

| New Brunswick | HST | Yes | Yes |

| PEI | HST | No | No |

| Quebec | PST | Yes | No |

| Manitoba | PST | Yes | Yes |

| Ontario | HST | Yes | No |

| British Columbia | PST | Yes | No |

| Saskatchewan | PST | No | No |

| Alberta | n/a | Yes | No |

Release and Accounting

22. To prevent delays in the release of imported casual goods, the CBSA will authorize the importer or agent to account for the applicable provincial taxes under normal customs practices.

23. Couriers and customs brokers who have "release prior to payment" privileges and wish to receive release of goods before payment of the HST, PST, provincial tobacco tax and/or alcohol markup/fee may do so on the understanding that the taxes and/or alcohol markup/fee are to be remitted to the CBSA under their normal accounting procedures.

24. In the case of couriers and customs brokers who do not remit the HST, PST, provincial tobacco tax and/or alcohol markup/fee at the time of accounting when it is due, their casual shipments will not be released until payment of all taxes and/or alcohol markup/fee is made.

25. Casual importers who do not have account security with the CBSA are required to pay the duties and taxes, including payment of the HST and all applicable provincial taxes, and/or alcohol markup/fee, before release of the goods.

26. As required under the Importation of Intoxicating Liquors Act, the alcohol markup/fee will be assessed based on the province of importation, regardless of the goods' intended final destination.

Adjustments and Refunds

27. To request an adjustment or refund of duties and taxes on casual goods, individuals should submit Form B2G, CBSA Informal Adjustment Request, along with the receipt copy from the courier, to the appropriate Casual Refund Centre (CRC), as indicated in the completion instructions for Form B2G.

28. The CBSA will also refund to the importer, where applicable, the HST, PST, provincial tobacco tax and/or alcohol markup/fee. However, disputes over the collection of the PST, provincial tobacco tax and/or alcohol markup/fee will be forwarded to the appropriate provincial government for processing.

29. Any interest refundable will only be payable on the amount of federal duties and taxes such as the GST and HST. Interest on the PST, provincial tobacco tax and/or alcohol markup/fee portion will not be refunded by the CBSA.

30. If a commercial shipment has been assessed as casual, a refund of the HST, PST, provincial tobacco tax and/or alcohol markup/fee will be processed by a CBSA Casual Refund Center (CRC) using Form B2G or Form B2, Canada Customs – Adjustment Request. The Form should quote the appropriate "dummy" classification number.

Additional Information

31. For more information, within Canada call the Border Information Service at 1-800-461-9999. From outside Canada call 204-983-3500 or 506-636-5064. Long distance charges will apply. Agents are available Monday to Friday (08:00 – 16:00 local time / except holidays). TTY is also available within Canada: 1-866-335-3237.

Appendix A

| Provinces | HST or PST | Tobacco Tax | Alcohol Markup/Fee |

|---|---|---|---|

| Nunavut | 0000.99.99.02 | 0000.99.99.42 | 0000.99.99.22 |

| Newfoundland and Labrador | 0000.99.99.03* | 0000.99.99.43 | 0000.99.99.23 |

| Nova Scotia | 0000.99.99.04* | 0000.99.99.44 | 0000.99.99.24 |

| New Brunswick | 0000.99.99.05* | 0000.99.99.45* | 0000.99.99.25* |

| Prince Edward Island | 0000.99.99.06 | 0000.99.99.46 | 0000.99.99.26 |

| Quebec | 0000.99.99.07* | 0000.99.99.47* | 0000.99.99.27 |

| Ontario | 0000.99.99.08* | 0000.99.99.48 | 0000.99.99.28 |

| Manitoba | 0000.99.99.09* | 0000.99.99.49* | 0000.99.99.29* |

| Saskatchewan | 0000.99.99.10* | 0000.99.99.50 | 0000.99.99.30 |

| Alberta | 0000.99.99.11 | 0000.99.99.51* | 0000.99.99.31 |

| British Columbia | 0000.99.99.12* | 0000.99.99.52* | 0000.99.99.32 |

| Yukon | 0000.99.99.13 | 0000.99.99.53 | 0000.99.99.33 |

| Northwest Territories | 0000.99.99.14 | 0000.99.99.54 | 0000.99.99.34 |

| * "Dummy" classification numbers have been issued for all provinces and territories in anticipation of agreements being reached. At this time, only those identified with an asterisk are to be used, as agreements with these provinces are already in place. | |||

Appendix B - Accounting for The Harmonized Sales Tax and Provincial Sales Tax on Form B3-3, Canada Customs Coding Form

The example on the following page shows how to complete Form B3-3, an "AB" type entry, when accounting for the HST and PST on casual goods entering Manitoba in the commercial stream. In this example, there are a total of ten shirts valued at $40 CAD each. However, five shirts are destined for Manitoba and five shirts are destined for New Brunswick.

Form B3-3 is completed according to normal reporting procedures as detailed in Memorandum D17-1-10, Coding of Customs Accounting Documents. The HST and PST are calculated "off-entry" and accounted for on a separate line using "dummy" classification numbers specific to the province as listed above in Appendix A. For the calculation and rates of the applicable PST, please refer to Appendix A of Memorandum D2-3-6.

Notes:

- To account for the HST on an entry where there is no GST or PST, use code 99 in the GST field (No. 35) to exempt the GST on the normal classification line.

- Field 50 for the GST should include the total GST, HST and PST.

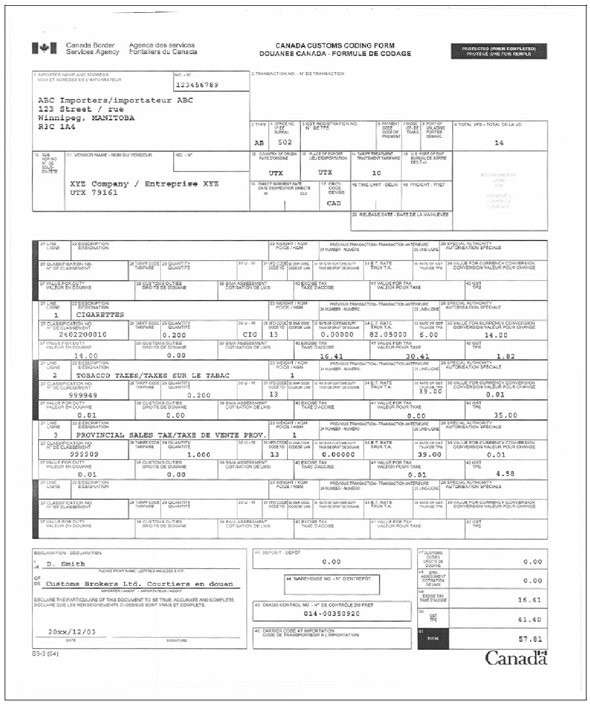

Appendix C - Accounting for the Provincial Tobacco Tax and Alcohol Markup/Fee on Form B3-3, Canada Customs Coding Form

Provincial Tobacco Tax

The customs duties and GST amounts are to be shown according to normal reporting procedures as detailed in Memorandum D17-1-10, Coding of Customs Accounting Documents. Provincial taxes, and HST where applicable, are accounted for using the "dummy" classification numbers listed above in Appendix A. The rates and calculation formula for provincial tobacco tax can be found in Appendix A of Memorandum D2-3-6.

The example on the following page shows how to complete Form B3-3 when reporting Manitoba tobacco tax and PST information on a casual importation of 200 UST (United States tariff) cigarettes, marked "CANADA DUTY PAID * DROIT ACQUITTÉ," with a value for duty of $14 CAD, that were released and are destined for Manitoba.

Notes:

- Fields 36 and 37 can be left blank or you can enter ".01" or "0" (zero).

- Field 50 for the GST should include the total GST, HST, PST and provincial tobacco tax.

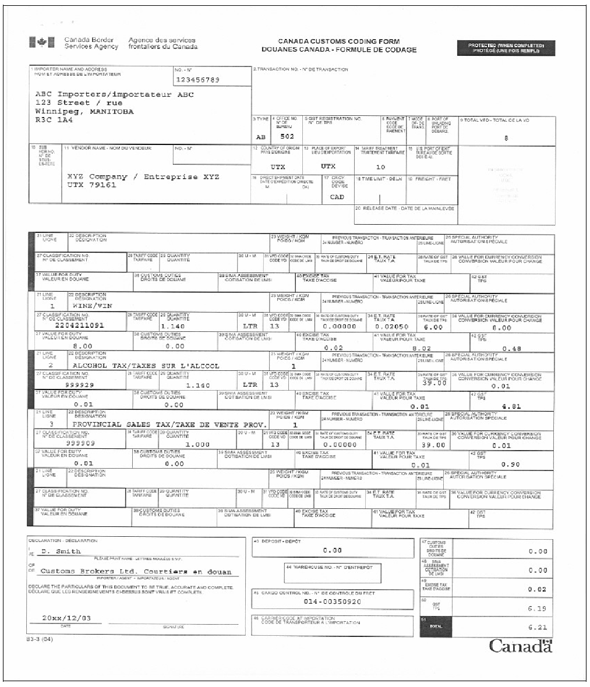

Appendix D - Alcohol Markup/Fee

The customs duties and GST amounts are to be shown according to normal reporting procedures as detailed in Memorandum D17-1-10, Coding of Customs Accounting Documents. Provincial taxes and/or HST are accounted for using the "dummy" classification numbers listed above in Appendix A.

Instruction on how alcohol markup/fee are applied in each province can be found in Appendix B of Memorandum D2-3-6 and the rates and calculation formula for the alcohol markup/fee can be found in Appendix B of Memorandum D2-3-6.

The example on the following page shows how to complete Form B3-3 when reporting the Manitoba alcohol markup/fee and PST information on a casual importation of a 1.14 liters bottle of wine, with a value for duty of CAN$8, that was released and is destined for Manitoba.

Notes:

- Fields 36 and 37 can be left blank or you can enter ".01" or "0" (zero).

- Field 50 for the GST should include the total HST, PST and alcohol markup/fee.

- Alcohol importations, as they pertain to non-commercial shipments, must meet the requirements of the Importation of Intoxicating Liquors Act and Memorandum D2-3-6.

References

- Issuing office:

- Commercial Program Directorate

- Headquarters file:

- 7983

- Legislative references:

-

- Canada Border Services Agency Act

- Customs Act

- Importation of Intoxicating Liquors Act

- Federal-Provincial Fiscal Arrangements Act

- Order in Council P.C. 1992-1268, June 11, 1992

- Other references:

- Superseded memorandum D:

- D17-1-22 dated July 1, 2010

- Date modified: