GB 2021 ER: Gypsum board

Statement of Reasons: Expiry review determination

Concerning an expiry review determination under paragraph 76.03(7)(a) of the Special Import Measures Act respecting the dumping of certain gypsum board originating in or exported from the United States of America, imported into Canada for use or consumption in the provinces of British Columbia, Alberta, Saskatchewan, and Manitoba, as well as the Yukon and Northwest Territories

Decision

Ottawa,

On May 12, 2022, pursuant to paragraph 76.03(7)(a) of the Special Import Measures Act, the Canada Border Services Agency determined that the expiry of the finding made by the Canadian International Trade Tribunal on January 4, 2017, in Inquiry No. NQ-2016-002, is likely to result in the continuation or resumption of dumping of certain gypsum board originating in or exported from the United States of America, imported into Canada for use or consumption in the provinces of British Columbia, Alberta, Saskatchewan, and Manitoba, as well as the Yukon and Northwest Territories.

On this page

Executive summary

[1] On December 13, 2021, the Canadian International Trade Tribunal (CITT), pursuant to subsection 76.03(3) of the Special Import Measures Act (SIMA), initiated an expiry review of its finding made on January 4, 2017, in Inquiry No. NQ-2016-002, concerning the dumping of certain gypsum board originating in or exported from the United States of America (US), imported into Canada for use or consumption in the provinces of British Columbia, Alberta, Saskatchewan, and Manitoba, as well as the Yukon and Northwest Territories (Western Canada).

[2] As a result of the CITT’s notice of expiry review, on December 14, 2021, the Canada Border Services Agency (CBSA) initiated an expiry review investigation to determine, pursuant to paragraph 76.03(7)(a) of SIMA, whether the rescission of the finding is likely to result in the continuation or resumption of dumping of the subject goods.

[3] The CBSA received four responses to its Canadian Producer Expiry Review Questionnaire (ERQ) from; Cabot Manufacturing ULC (Cabot)Footnote 1, Atlantic Wallboard Limited Partnership (AWLP)Footnote 2, CertainTeed Canada Inc. (CT Canada)Footnote 3, and CGC Inc. (CGC)Footnote 4. It should be noted that CT Canada, the complainant in the original investigation, is the only producer of like goods in Western Canada. The remaining Canadian producers all produce gypsum board outside of Western Canada. As both CGC and CT Canada imported subject goods during the period of review, both provided information on those imports in their response to the Canadian Producer ERQ and were not required to provide an additional response to the Importer ERQ.

[4] The ERQ responses submitted by CT Canada and Cabot include information supporting their position that continued or resumed dumping of certain gypsum board from the US is likely if the CITT’s finding is rescinded. The ERQ response submitted by CGC includes information supporting its position that continued or resumed dumping of certain gypsum board from the US is unlikely if the CITT’s finding is rescinded. In its ERQ response, AWLP did not express its position regarding the likelihood of the continuation or resumption of dumping, preferring to defer to the views of parties more directly involved in Western Canadian Market.

[5] The CBSA received one response to the Importer ERQ from Georgia-Pacific Canada LP (GP Canada)Footnote 5 which includes information supporting its position that continued or resumed dumping of certain gypsum board from the US is unlikely if the CITT’s finding is rescinded.

[6] The CBSA also received three responses to the Exporter ERQ from: USG Corporation (USG)Footnote 6, Saint-Gobain Gypsum USA, Inc. (CT US)Footnote 7, and Georgia-Pacific Gypsum LLC (GP US)Footnote 8. CT US did not directly state its position, instead citing CT Canada’s ERQ response which supports the position that continued or resumed dumping of certain gypsum board from the US is likely if the CITT’s finding is rescinded. The ERQ responses submitted by USG and GP US include information supporting their position that continued or resumed dumping of certain gypsum board from the US is unlikely if the CITT’s finding is rescinded.

[7] The CBSA received case briefs filed on behalf of CabotFootnote 9, CT CanadaFootnote 10, GP Canada/GP USFootnote 11, and USG/CGCFootnote 12. The CBSA also received reply submissions filed on behalf of CT CanadaFootnote 13 and GP Canada/GP USFootnote 14. The case briefs and reply submission filed on behalf of CT Canada and Cabot submit arguments supporting the position that continued or resumed dumping of certain gypsum board from the US likely if the CITT’s finding is rescinded. Conversely, the case briefs and reply submission filed on behalf of GP Canada/GP US and USG/CGC submit arguments supporting the position that the expiry of the finding is unlikely to result in the continuation or resumption of dumping of the subject goods from the US.

[8] Analysis of information on the administrative record indicates a likelihood of continued or resumed dumping of certain gypsum board originating in or exported from the US, imported into Canada for use or consumption in Western Canada, should the CITT’s finding be rescinded. This analysis relied upon the following factors:

- Dumping of subject goods during the period of review

- Substantial imports of subject goods during the period of review

- Western Canada remains an important market for US exporters

- Significant excess capacity in the US

- US market demand

- Differences between the price of exports to Western and Eastern Canada

[9] For the forgoing reasons, the CBSA, having considered the relevant information on the administrative record, determined on May 12, 2022, pursuant to paragraph 76.03(7)(a) of SIMA, that the expiry of the finding is likely to result in the continuation or resumption of dumping of the goods from the US.

Background

[10] On June 8, 2016, pursuant to subsection 31(1) of SIMA, the CBSA initiated an investigation respecting the dumping of certain gypsum board originating in or exported from the US, imported into Canada for use or consumption in Western Canada. The investigation followed receipt of a properly documented complaint from CertainTeed Gypsum Canada Inc., now known as CertainTeed Canada Inc. (CT Canada).

[11] On December 5, 2016, pursuant to subsection 41(1) of SIMA, the CBSA made a final determination of dumping concerning certain gypsum board originating in or exported from the US, imported into Canada for use or consumption in Western Canada.Footnote 15

[12] On January 4, 2017, pursuant to subsection 43(1) of SIMA, the CITT found that the dumping of certain gypsum board originating in or exported from the US, imported into Canada for use or consumption in Western Canada, had caused injury to the Canadian domestic industry.Footnote 16

[13] On February 24, 2017, the Governor General in Council, on the recommendation of the Minister of Finance, pursuant to section 115 of the Customs Tariff, issued P.C. 2017-175 Gypsum Board Products Anti-dumping Duty Remission Order, 2017. The remission order followed a report issued by the CITT recommending that the anti-dumping duties be reduced in order to ensure the duties would not impose an unnecessary burden for downstream users of certain gypsum board while, at the same time, maintaining duties at a level that protected the domestic producer from the injurious effects of dumped imports as provided for under SIMA.Footnote 17

[14] On June 8, 2020, an importer of subject goods, CGC, requested that the CITT initiate an interim review of the finding. CGC contended that a regional market no longer existed and as such the legal basis for the CITT’s finding was no longer present. On October 22, 2020, pursuant to subsections 76.01(3) and (4) of SIMA, the CITT decided not to conduct an interim review of its finding. The decision not to conduct an interim review was based on CGC’s inability to convince the CITT that there was a reasonable indication that a regional market no longer existed with respect to the subject and like goods.Footnote 18

[15] On October 22, 2021, the CITT issued a notice concerning the expiry of its finding, which was scheduled to occur on January 3, 2022. Based on the information filed during the expiry process, the CITT decided that a review of the finding was warranted. On December 13, 2021, the CITT initiated an expiry review of its finding pursuant to subsection 76.03(3) of SIMA.Footnote 19

[16] On December 14, 2021, the CBSA commenced an expiry review investigation to determine whether the rescission of the finding is likely to result in continued or resumed dumping of the subject goods from the US, imported into Canada for use or consumption in Western Canada.

Product definition

[17] The goods subject to this expiry review investigation are defined as:

“Gypsum board, sheet, or panel (“gypsum board”) originating in or exported from the United States of America, imported into Canada for use or consumption in the provinces of British Columbia, Alberta, Saskatchewan, and Manitoba, as well as the Yukon and Northwest Territories, composed primarily of a gypsum core and faced or reinforced with paper or paperboard, including gypsum board meeting or supplied to meet ASTM C 1396 or ASTM C 1396M or equivalent standards, regardless of end use, edge-finish, thickness, width, or length, excluding:

- gypsum board made to a width of 54 inches (1,371.6 mm)

- gypsum board measuring 1 inch (25.4 mm) in thickness and 24 inches (609.6 mm) in width regardless of length (commonly referred to and used as “paper-faced shaft liner”)

- gypsum board meeting ASTM C 1177 or ASTM C 1177M (commonly referred to and used primarily as “glass fiber re-enforced sheathing board” but also sometimes used for internal applications for high mold/moisture resistant applications)

- double layered glued paper-faced gypsum board (commonly referred to and used as “acoustic board”)

- gypsum board meeting ISO16000-23 for sorption of formaldehyde

All dimensions are plus or minus allowable tolerances in applicable standards.”

Additional product information

[18] For greater certainty, the gypsum board considered subject goods includes but is not limited to:

- Abuse-resistant gypsum board offering greater resistance to surface indentation, abrasion and penetration than standard gypsum board

- Eased edge gypsum board, which has a tapered and slightly rounded or beveled factory edge. It may be used as an aid in custom finishing of joints

- Gypsum base for veneer plaster serves as a base for thin coats of hard, high strength gypsum veneer plaster

- Impact-resistant gypsum board offers greater resistance to the impact of solid objects from high traffic and vandalism than standard gypsum board

- Mold-resistant gypsum board or Mold and moisture resistant gypsum board has a mold/moisture resistant gypsum core and paper facing that incorporates various methods of preventing the growth of mold and mildew on the board's surface

- Regular gypsum board (gypsum wallboard) is used as a surface layer on walls and ceilings

- Sag-resistant gypsum board is a ceiling board that offers greater resistance to sagging than regular gypsum products used for ceilings where framing is typically spaced 24 inches

- Type C or Proprietary Type-X gypsum board is available in 1/2 inch and 5/8 inch thicknesses and is required in some fire rated assemblies. Additional additives give this product improved fire resistive properties

- Type X gypsum board is available in 1/2 inch and 5/8 inch thicknesses and has an improved fire resistance made possible through the use of special core additives. Type X gypsum board is used in most fire rated assemblies

[19] Gypsum board has long been used as a building material because of its fire-resistant properties. It provides a durable, economical, non-combustible and easily decorated surfacing material for construction use. Gypsum board is the most widely used material for ceilings and interior walls for residential, commercial, and institutional buildings in developed countries. Paper-covered gypsum board is well suited to the application for which it was designed, that is interior non-load bearing construction.

Classification of imports

[20] The subject goods are usually classified under the following tariff classification numbers:

- 6809.11.00.19

- 6809.11.00.90

[21] This listing of tariff classification numbers is for convenience of reference only. The tariff classification numbers provided may include goods that are not subject goods and subject goods may be imported into Canada under tariff classification numbers other than those provided. Refer to the product definition for authoritative details regarding the subject goods.

Period of review

[22] The period of review (POR) for the CBSA’s expiry review investigation is from January 1, 2018 to September 30, 2021.

Regional market

[23] The CITT finding relates to subject goods imported into a regional market, namely, certain gypsum board imported into Canada for use or consumption in the provinces of British Columbia, Alberta, Saskatchewan, and Manitoba, as well as the Yukon and Northwest Territories (collectively referred to as Western Canada).

[24] In accordance with SIMA, two conditions must be met for the existence of a regional market. As per subsection 2(1.1) of SIMA, they are that:

- the producers in that market sell all or almost all of their production of like goods in the market

- the demand in that market is not to any substantial degree supplied by producers of like goods located elsewhere in Canada

[25] Further, where subsection 2(1.1) of SIMA applies, subsection 42(5) of SIMA provides that the CITT shall not find that the dumping of the goods has caused injury or is threatening to cause injury unless:

- there is a concentration of those goods into the regional market

- the dumping of those goods has caused injury or is threatening to cause injury to the producers of all or almost all of the production of like goods in the regional market

[26] As previously noted, CGC filed a request for an interim review with the CITT regarding its finding respecting certain gypsum board in June 2020. CGC’s request was based on its view that a regional market no longer existed given that following the finding, considerable volumes of gypsum board produced in Eastern Canada were now being sold into the Western Canadian market. Without a regional market, CGC contended that the legal basis for the CITT”s finding no longer existed and that the finding should be rescinded.Footnote 20

[27] In October 2020, the CITT decided not to conduct an interim review of its finding as CGC had not convinced the CITT that there was a reasonable indication that a regional market no longer existed for the subject and like goods. In that decision, the CITT noted that CGC did not provide any evidence demonstrating that shipments from Eastern Canada into Western Canada were a result of anything other than the imposition of anti-dumping duties or that such shipments would continue in the absence of duties. With no structural changes in the circumstances which led to its finding, the CITT concluded there was an insufficient factual basis on which to initiate an interim review.Footnote 21

[28] The CITT will again give consideration to the issue of a regional market as part of its expiry review to determine whether the continued or resumed dumping of the subject goods are likely to result in injury.

Western Canadian industry

[29] Information provided by all known producers of gypsum board in Canada in response to CBSA ERQs indicates that the composition of the Western Canadian industry has not changed since the original investigation. The Canadian industry for certain gypsum board remains entirely comprised of a single Western Canadian producer, CT Canada (the complainant).

[30] As such, based on the information on the record, the CBSA has based its estimates of domestic production of like goods on the production figures supplied by CT Canada in its ERQ response. However, with respect to sales of certain gypsum board in Western Canada and the estimation of the apparent market, the CBSA has included sales of goods produced in Western Canada by CT Canada as well as goods produced by other Canadian producers in the rest of Canada (i.e. AWLP, Cabot, and CGC).

Certainteed Canada Inc. (CT Canada)

[31] The only producer in Western Canada, CT Canada, was founded in Winnipeg, Manitoba in 1929 as Western Gypsum Products Limited. Later known as Westroc Industries, the company was acquired by the BPB group in 1954 and became BPB Westroc. In 2003, the company changed its name to BPB Canada. BPB Canada was subsequently acquired by Saint-Gobain in late 2005 and became part of the North American CertainTeed group of companies at the beginning of 2007, where it remains today.Footnote 22

[32] During the POR, CT Canada produced gypsum board at three facilities in Western Canada located in Calgary, Alberta; Delta, British Columbia; and Winnipeg, Manitoba. CT Canada also produced gypsum board during the POR at three other facilities outside of Western Canada located in McAdam, New Brunswick; Mississauga, Ontario; and Sainte-Catherine, QC. It should be noted that the MacAdam facility was permanently closed by CT Canada in February 2021.Footnote 23

Western Canadian market

[33] The CBSA cannot release specific quantitative data respecting the value and volume of Western Canadian production of certain gypsum board sold for domestic consumption as it would lead to the disclosure of confidential information submitted by CT Canada, the only Western Canadian producer of like goods. The CBSA is also unable to present specific quantitative data respecting the value and volume of goods produced in the rest of Canada and sold into Western Canada as it would lead to the disclosure of confidential information submitted by those producers. As a result, the CBSA can only discuss the apparent Western Canadian market for certain gypsum board over the POR in non-specific terms. Specifics regarding the volume and value of imported goods are discussed later in the imports section.

[34] Based on the information submitted by the parties and available to the CBSA on the administrative recordFootnote 24, the total estimated apparent Western Canadian market declined in 2019 in both volume and value as compared to 2018. In 2020, the market was completely flat in terms of both volume and value. In extrapolating the data for the fist three quarters of 2021 to arrive at annualized figures, the figures suggest that both volume and value will rise when compared to 2020, reaching totals near those calculated for 2018.

[35] The information on the administrative record also showed that during the POR, CT Canada maintained a consistent share of the estimated apparent Western Canadian market. In 2019, the market share of imports sold in Western Canada declined, most of which was lost to Canadian goods produced outside the regional market. In 2020, the market share of imports increased and then increased slightly in the first three quarter of 2021.

[36] The information available also showed that between 2018 and 2020, GP Canada managed to substantially increase its share of the estimated apparent Western Canadian market. Data for the first three quarters of 2021 also suggests that GP Canada is likely to hold onto the market share it gained during the POR.

[37] With respect to CGC, the data showed that its overall share of the estimated apparent Western Canadian market was consistent in 2018 and 2019 before declining in 2020.Footnote 25 Between 2018 and 2019, CGC’s sales of goods imported from USG declined in terms of Western Canadian market share as CGC switched to selling a greater amount of Canadian goods produced outside of the Western Canadian market. While CGC’s share of the Western Canadian market in 2020 remained flat, data for the first three quarters of 2021 shows its market share from sales of imports from USG increased.

Western Canadian production and capacity utilization

[38] CT Canada’s production in Western Canada declined in 2019 as compared to 2018. In 2020, CT Canada’s production increased, although it remained below the peak reached in 2018. Annualizing the production figures for the first three quarters of 2021 suggests that CT Canada’s production could increase compared to 2020 and exceed the volume of production reported for 2018.Footnote 26

[39] CT Canada’s Western Canadian production capacity was consistent in 2018 and 2019 before increasing in 2020. CT Canada’s capacity utilization rate dropped in 2019 and then increased in 2020. The utilization rate reported for the first three quarters of 2021 shows a capacity utilization rate which is just above the rate reported for 2018.Footnote 27

Imports into Western Canada

[40] The volumes and values of subject imports from the US during the POR presented in this section are based on the information provided to the CBSA by the importers and exporters in response to the ERQ. The data relating to imports from non-subject countries is based on the CBSA’s own import data.

[41] With respect to CGC, it should be noted that it did not provide separate data for sales of imports versus total imports into Western Canada during the POR. Despite this, CGC’s data was considered to be the best information available from the ERQ responses submitted by CGC and USG for the purposes of calculating the figures for Table 1 below. USG’s export data was considered to be unreliable due to issues encountered with the revised data it submitted.Footnote 28 It should be noted that CGC’s import volume and value during the POR as included in the figures presented in Table 1 may be slightly understated given it can take time to sell the goods from the warehouse inventories following their actual date of importation. In addition, CGC’s value is likely overstated given it represents the value of the sales made in the Western Canadian market during the POR and is not based on the prices paid to USG for the imported goods.

[42] In regards to CT Canada and GP Canada, both importers provided data relating specifically to imports and sales in Western Canada separately, as requested by the CBSA in the ERQ. Both companies’ import volume data was consistent with the export volume data submitted by their relative exporters and used in coming up with the total figures shown in Table 1.

[43] However, with respect to GP Canada, the values reported for the imports during the POR were inconsistent with the export values submitted by GP US. Specifically, GP Canada’s values, which were reported in CAD as requested in Appendix 1 of the ERQ, were too close to the USD values reported by GP US in its Appendix 3 of the ERQ to account for the foreign exchange rates in effect for the POR.

[44] The issue regarding the inconsistencies in the data provided by GP Canada and GP US in response to the ERQ was discussed in the case brief and reply submissions submitted on behalf of CT Canada and GP. In an attempt to address the issue as raised in CT Canada’s brief, GP’s reply submission suggested that the correct values were reported by GP US in the Appendix 3 of its ERQ response but did not provide any explanation regarding the discrepancies identified.Footnote 29 In an effort to use the best information available from the ERQ responses of the parties, the CBSA used the volume and values reported by GP US for purposes of Table 1 below and converted the USD figures to CAD using the Bank of Canada’s average annual exchange rateFootnote 30.

| Source | 2018 | 2019 | 2020 | 2021 (Jan 1 - Sep 30) | ||||

|---|---|---|---|---|---|---|---|---|

| Import volume (MSF) | Import value (CAD) | Import volume (MSF) | Import value (CAD) | Import volume (MSF) | Import value (CAD) | Import volume (MSF) | Import value (CAD) | |

| United StatesFootnote 31 | 194,873 | $59,349,980 | 124,456 | $37,923,733 | 134,789 | $40,758,220 | 133,004 | $38,465,966 |

| All other countriesFootnote 32 | 3,417 | $1,553,582 | 228 | $102,938 | 1 | $76,351 | 18 | $141,252 |

| Total imports | 198,290 | $60,903,562 | 124,684 | $38,026,671 | 134,790 | $40,834,571 | 133,022 | $38,607,218 |

[45] Based on the figures above, imports from the US accounted for over 99% of the total imports of certain gypsum board into Western Canada in every year except 2018 where they accounted for 98%. The dominance of US exports in terms of total imports into Western Canada during the POR is consistent with the CBSA’s findings in the original investigation where imports from the US represented 99.99% of imports in 2015.Footnote 33

[46] Import volumes in Table 1 also show that total imports fell by 37% in 2019 and then increased 8% in 2020. An extrapolation of the data available for the first three quarters of 2021 results in an annualized import volume of 177,363 MSF which translates into a 32% increase in imports year-over-year.

Enforcement data

[47] The enforcement data provided by the SIMA Compliance Unit (SCU) is presented in Table 2 below. It should be noted that the volume provided by SCU was reported in square meters (MTK) as that was the unit of measurement specified in the Customs Tariff and applicable to the goods imported during the POR. In order to allow comparison with other figures presented, those volumes have been converted to MSF and are also shown in the following table.

| 2018 | 2019 | 2020 | 2021 (Jan 1 - Sep 30) | |

|---|---|---|---|---|

| Volume of subject goods (MTK) | 15,229,665 | 13,572,346 | 15,072,777 | 13,381,253 |

| Volume of subject goods converted (MSF)Footnote 35 | 163,931 | 146,091 | 162,242 | 144,034 |

| Value of subject goods (CAD) | $41,972,980 | $35,545,475 | $36,896,741 | $31,948,568 |

| SIMA duty assessed (CAD) | $36,911 | $148 | $206,231 | $99,346 |

| SIMA duty remitted (CAD) | $0 | $4,184,637 | $3,956,787 | $3,155,163 |

[48] As shown in the table above, there are two different sets of values relating to SIMA duty, duty assessed and duty remitted. While the duty assessed amounts relate to anti-dumping duty owing and/or collected by the CBSA, the duty remitted amounts relate to anti-dumping duty paid or payable that was remitted in accordance with the remission order issued by the Governor General in Council on February 24, 2017.Footnote 36 As such, the remitted anti-dumping duty shown above is not ultimately collected by the CBSA.

[49] The remission order establishes reference values that are 32.17% lower than the normal values that were established by the CBSA in the original investigation. The remission order allows for the remission of anti-dumping duties that exceed the difference between the reference value and the export price, which essentially establishes a new minimum price for importation of subject goods into Western Canada that is lower than normal values established by the CBSA. The reference values are indexed annually based on the Industrial Product Price Index for gypsum product manufacturing. The applicable annual index factor is published on the CBSA’s website and the reference values continue to apply to the calculation of anti-dumping duty.Footnote 37

[50] Subsection 2(1) of SIMA defines dumped as “in relation to any goods, means that the normal value of the goods exceeds the export price thereof”. In terms of dumping, the SIMA duty remitted amount represents the portion of dumping calculated as the difference between the normal values and the export prices, but includes only the amount of dumping that exceeds the remission order reference values. The SIMA duty assessed amount represents the portion of dumping equal to the remission order reference values less the export prices.

[51] The enforcement data in Table 2 shows that the volume of subject imports decreased in 2019 by 11% and then increased by 11% in 2020. In extrapolating the data for the first three quarter of 2021, the annualized import volume in 2021 shows subject imports rising by nearly 30,000 MSF which represents an 18% increase year-over-year.

[52] With respect to dumping over the POR, the enforcement data shows that the total amount of duties in 2018, both assessed and remitted, equalled less than 1% of the total value of the subject goods. In 2019, the total SIMA duties increased significantly resulting in an annual average dumping margin of 11%, expressed as a % of the total value of the subject goods. The annual average dumping margin in 2020 was 11% and decreased to 10% in the first three quarters of 2021.

[53] Given the issues encountered regarding the potential accuracy and reliability of the data submitted by the exporters and importers, as discussed in the previous section, it is not surprising that the volume and value of subject imports shown in Table 1 differ from the data presented in Table 2. However, despite the differences, it should be noted that both sets of data show the same general trends respecting the level of importation of subject goods over the POR, albeit in different magnitudes.

Parties to the proceedings

[54] On December 14, 2021, a notice concerning the CBSA’s initiation of the expiry review investigation was sent to Canadian producers, importers, and exporters of certain gypsum board. All of these parties were also sent an ERQ.

[55] The ERQs requested information relevant to the CBSA’s consideration of the expiry review factors, as listed in subsection 37.2(1) of the Special Import Measures Regulations (SIMR).

[56] The only Western Canadian producer and complainant, CT Canada, participated in the expiry review investigation and provided an ERQ response. A case brief and reply submission were also received from counsel on behalf of CT Canada.

[57] Three other Canadian producers outside of Western Canada also provided ERQ responses, including Cabot, AWLP, and CGC. Of this group, the CBSA received case briefs from counsel on behalf of Cabot and USG/CGC. None of these parties provided a reply submission.

[58] The CBSA received one response to the importer ERQ from GP Canada. Both CGC and CT Canada also acted as importers during the POR but were not required to complete an importer ERQ given both parties provided responses to the Canadian producer ERQ. A case brief and reply submission were also received from counsel on behalf of GP Canada and GP US (collectively referred to as GP).

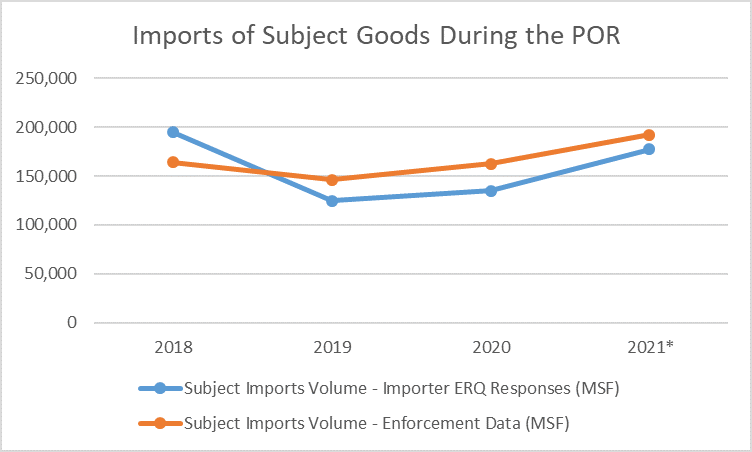

[59] The CBSA received responses to the exporter ERQ from three exporters, USG, CT US, and GP US. Case briefs were received from counsel on behalf of GP and USG/CGC. A reply submission was also received from counsel on behalf of GP.

Information considered by the CBSA

[60] The information considered by the CBSA for purposes of this expiry review investigation is contained in the administrative record. The administrative record includes the information on the CBSA’s exhibit listing, which is comprised of the CITT’s administrative record relating to the initiation of the expiry review, the CBSA’s exhibits and information submitted by interested parties, including information which the interested parties feel is relevant to the decision as to whether dumping is likely to continue or resume absent the CITT finding. This information may consist of expert analysts’ reports, excerpts from trade magazines and newspapers, news articles, orders and findings issued by authorities of Canada or of a country other than Canada, documents from international trade organizations such as the World Trade Organization (WTO) and responses to the ERQs submitted by Canadian producers, exporters and importers.

[61] For purposes of an expiry review investigation, the CBSA sets a date after which no new information submitted by interested parties will be placed on the administrative record or considered as part of the CBSA’s investigation. This is referred to as the “closing of the record date” and is set to allow participants time to prepare their case briefs and reply submissions based on the information that is on the administrative record as of the closing of the record date. For this investigation, the administrative record closed on February 2, 2022.

Position of the parties - dumping

Parties contending that continued or resumed dumping is likely

[62] CT Canada, the complainant and sole Western Canadian producer, made representations through its ERQ responses as well as in its respective case brief and reply submissions supporting its position that the dumping of certain gypsum board from the US is likely to continue or resume should the CITT’s finding expire. Cabot, a Canadian producer located outside Western Canada, submitted a case brief supporting CT Canada’s submissions and agreeing with CT Canada’s position that dumping will continue or resume should the CITT’s finding expire.Footnote 38

[63] The main arguments detailed by CT Canada and supported by Cabot can be summarized as follows:

- US Producers Continued to Dump into the Western Canadian Market

- Significant Volumes of Dumped Imports Will be Destined for Western Canada in the Absence of the Finding

- US Producers Have Shown Propensity to Engage in Aggressive Pricing Behaviour

- Trends in Import Volumes and Changes in Western Canadian Market Conditions Increase the Likelihood of Dumping

- The US Gypsum Board Industry has Significant and Growing Excess Capacity

- Weakening US Market Conditions Will Incentivize Exports to Canada

- Mexican Gypsum Board Will Displace US Production and Increase Diversion of US Production to Canada

- The Western Canadian Market is Particularly Attractive to Dumped US Imports

- Consolidation of Purchasers Widens the North American Footprint for Continued Dumping in Western Canada

US Producers Continued to Dump into the Western Canadian Market

[64] Referencing CBSA Enforcement Data, CT Canada noted that approximately $12 million worth of duties were either assessed or remitted over the POR, representing an average dumping margin greater than 11%. According to CT Canada, 452,000 MSF of subject goods imported over the POR with an average dumping margin over 11% is significant.Footnote 39

[65] With respect to the duties remitted, CT Canada noted that the duties would have been assessed and collected but for the remission order. They also pointed out that if dumping was not occurring, goods being exported to Western Canada at prices below the normal value, then there would have been no duties to remit. As such, CT Canada argued that remitted duties should be properly considered as evidence of dumping that occurred while the CITT’s finding was in place within the meaning of paragraph 37.2(1)(a) of SIMR.Footnote 40

Significant Volumes of Dumped Imports will be Destined for Western Canada in the Absence of the Finding

[66] CT Canada presented a chart demonstrating a negative correlation between the volume of imports and the changes in the remission order index factor over the POR. They noted that over the POR, when the index factor increased, causing exporters and importers to raise prices to receive the same level of remission as before, imports decreased. Conversely, when the index factor decreased and importers were eligible for greater remission at current prices, imports increased. As a result, CT Canada argues that absent the finding, there would be no price discipline and imports would likely increase at dumped prices.Footnote 41

[67] Referencing the differences between the duties remitted versus the duties assessed, CT Canada stated that US exporters consistently sell into Western Canada at the lowest price that avoids the payment of anti-dumping duties. CT Canada argued that this behaviour shows how price sensitive the Western Canadian market is and that US exporters were desperate over the POR to hold onto market share. CT Canada claimed that, absent the finding, US exporters would revert to dumped price levels to recapture as much market share as possible.Footnote 42

[68] Referencing evidence from the interim review request filed by CGC with the CITT, CT Canada argued that USG/CGC admitted that absent the finding, they would be shipping dumped goods from the US. CT Canada pointed to statements made by CGC indicating that shipping goods from its US production locations was more cost efficient than supplying the Western Canadian market from CGC’s Eastern Canadian production locations. The complainant also noted that the CITT, in its decision not to initiate an interim review, found that CGC’s shift to shipping goods from Eastern to Western Canada was nothing more than a temporary condition that arose as a result of the anti-dumping finding.Footnote 43

US Producers Have Shown Propensity to Engage in Aggressive Pricing Behaviour

[69] CT Canada argued that importers continue to engage in aggressive pricing behaviour to maintain or grow market, a behaviour consistent with the CITT’s observations made in the original finding.Footnote 44 CT Canada supported this argument by providing its own analysis of confidential pricing data available on the administrative record.

[70] CT Canada claimed CGC’s switch to supplying Western Canada from production in Eastern Canada also demonstrated aggressive pricing behaviour, which it supported with its pricing analysis. CT Canada also stated that in considering the freight costs from Eastern to Western Canada, CGC is likely selling its Eastern Canadian production into Western Canada at even lower ex-factory prices than presented in its analysis.Footnote 45

Trends in Import Volumes and Changes in Western Canadian Market Conditions Increase the Likelihood of Dumping

[71] According to CT Canada, US producers and exporters have gone to great lengths to maintain their market position in Western Canada as demonstrated by their continued significant dumping throughout the POR. CT Canada argued that absent the finding, US producers and exporters will resort to dumping to recapture their pre-finding position in the Western Canadian market.Footnote 46

[72] Based on Statistics Canada Data, CT Canada estimated that subject imports into Western Canada in 2015, before the finding, were substantially higher than imports in 2016. CT Canada indicated that imports had decreased further in 2017. CT Canada then noted that CBSA Enforcement data showed subject imports declined further to 146,091 MSF in 2018 before increasing slightly to 162,241 MSF in 2020. CT Canada noted that the data shows that subject imports declined significantly during the 2015-2020 period and attributed the decline to imports into the Western Canadian market being unable to compete at fully dumped prices. CT Canada highlighted that the drop in imports as a result of the finding has resulted in US imports losing market share.Footnote 47

[73] While the Western Canadian market exceeded 1 billion square feet (BSF) from 2013 to 2015, CT Canada noted that recent data shows market demand has declined as of 2020. CT Canada largely attributed the decline in demand for gypsum board between 2015 and 2020 to reductions in commercial real estate investment and housing demand driven by the collapse of oil prices in 2015/2016 and 2019/2020 and the Foreign Buyers’ Tax implemented in British Columbia in 2016.Footnote 48

[74] Recognizing that the Western Canadian market had improved in 2021, CT Canada argued that the increase was temporary and linked to COVID-induced increases in demand for housing and home renovation projects. Citing Bank of Canada housing projections, Canadian construction permit data for Western Canada, and housing starts information from Trading Economics, CT Canada maintained that the Western Canadian market for gypsum board is expected to decline in the next 12 to 24 months. Given the market trends, CT Canada contended that US producers and exporters would need to significantly dump subject goods in order to recapture lost sales volumes and market share.Footnote 49

The US Gypsum Board Industry has Significant and Growing Excess Capacity

[75] CT Canada claimed that the capacity data supplied by both USG and GP did not reflect true capacity and failed to show the greatest level of output that can be achieved. CT Canada supported the claim by referencing a variety of issues regarding the confidential information supplied by the exporters. As a result, CT Canada argued that the capacity data provided by USG and GP should not be relied upon in the CBSA’s analysis.Footnote 50

[76] CT Canada contended that data available from the Gypsum Association and the Gypsum Directory is likely more accurate and conservative than the data provided by the exporters in their ERQ responses and should be used instead. In addition, CT Canada noted that the data from those two sources accounts for capacity for all US gypsum board manufacturers and not just the exporters participating in the current review. Specifically, CT Canada noted that other US manufacturers such as National Gypsum, American Gypsum, and PABCO account for a significant portion of total US production capacity.Footnote 51

[77] Based on capacity and US domestic shipment volumes reported by the Gypsum Association and the Gypsum Directory, CT Canada estimated that in 2021, US producers had billions of square feet of excess capacity. CT Canada noted that this excess capacity was many times the size of the estimated Western Canadian market.Footnote 52

[78] In addition to the existing excess capacity, CT Canada also referenced plans by GP US to both build a new plant and close an existing plant in Texas which will result in a net increase in new capacity. CT Canada argued that the new plant will need to cannibalize demand from other GP US plants and that it will create a domino effect northward that will impact the Western Canadian market.Footnote 53

[79] CT Canada also cited numerous other expansions and improvements to be made to existing facilities by other producers in the US over the next couple of years. CT Canada concluded that such expansions and improvements would lead to greater excess capacity that could be targeted to Western Canada in the event the finding were to expire.Footnote 54

Weakening US Market Conditions Will Incentivize Exports to Canada

[80] According to CT Canada, US demand growth for gypsum board has slowed significantly since 2017. Citing reports from the Gypsum Association, CT Canada noted that US demand significantly increased between 2012 and 2016. Between 2017 and 2021, US demand also increased but at a less significant rate than the previous 2012-2016 period. CT Canada contended that a significant portion of the growth experienced between 2017 and 2021 was attributable to a temporary increase in demand for larger housing in 2021 caused by the COVID-19 pandemic. Referencing Q4 2021 data, CT Canada stated that that temporary demand has abated and that the data suggests continued softening in gypsum board demand for 2022 and 2023. CT Canada noted that shipments in the fourth quarter of 2021 were down from the previous quarter and from the second quarter. CT Canada claimed that these decreases were particularly notable given that the fourth quarter is traditionally a strong quarter for gypsum sales in the US.Footnote 55

[81] CT Canada also pointed out that US exports of gypsum board to Canada increased in 2020 and 2021 at the same time demand temporarily increased in the US. Given that US exporters increased shipments even as the US market grew, CT Canada argued that the level of dumping in the Western Canadian market would suffer should the US market deteriorate as they expect.Footnote 56

[82] Noting that demand for gypsum board in North America is primarily driven by construction activity and repair/remodelling demand, CT Canada argued that when analysing total construction activity, the analysis must account for inflation. According to the inflation-adjusted data presented by CT Canada, the total volume of construction is expected to decline in 2022 and 2023 by 2.5% in each year. CT Canada contended that US producers will return to the practice of using Western Canada as a way to fill capacity and offload excess production in response to the expected US declines in demand forecast for 2022 and 2023.Footnote 57

Mexican Gypsum Board Will Displace US Production and Increase Diversion of US Production to Canada

[83] CT Canada stated that the Mexican gypsum board industry is gaining a growing foothold in the US market at a time when the US industry is facing massive excess capacity and market prospects are in decline. CT Canada argued that the competitive pressure from Mexico will cause US manufacturers to divert production to Western Canada as they seek outlets to offload their excess capacity.Footnote 58

[84] CT Canada noted that US International Trade Commission (USITC) import data showed imports of gypsum board from Mexico into the US rise from 500,000 MSF in 2018 to 580,000 MSF in 2020. USITC data for January to November 2021 also showed that imports from Mexico jumped to 795,000 MSF. CT Canada pointed out that the increase in US imports from Mexico between 2018 and 2021 (January-November) of 297,000 MSF coincided with an increase in US exports of gypsum board to Canada by over 81,000 MSF. They claimed that the data demonstrated how Mexican imports displaced US production and resulted in the diversion of goods to Western Canada. Moreover, CT Canada noted that in 2021, Panel Rey announced plans to double capacity of its Ciudad Juárez plant located across the border from El Paso, Texas.Footnote 59

[85] CT Canada contended that the rise in Mexican imports into the US also coincided with the imposition of anti-dumping duties on Mexican gypsum board by Colombia and Brazil. They noted that Colombia originally imposed duties in October 2017 and extended those duties for an additional five years in August 2020. Brazil imposed anti-dumping duties on Mexican gypsum board starting in September 2018, duties which will remain in place for five years until 2023.Footnote 60

[86] CT Canada also cited reports indicating that growth in Mexico’s construction industry had been particularly soft as recently as April 2021 and that 2020 had marked a 10-year low in housing starts and inventory. CT Canada argued that reports of rising inflation in Mexico would also put pressure on growth in the construction industry. CT Canada concluded that the US gypsum industry will likely face increasing competition from Mexico over the next 12 to 24 months.Footnote 61

The Western Canadian Market is Particularly Attractive to Dumped US Imports

[87] CT Canada argued that Canada is the only viable export market for US gypsum board manufacturers. They also contended that after domestic demand in the US is fulfilled, nearly all excess gypsum board capacity in the US only competed for a single market, Canada. Referencing exports statistics from the USITC, CT Canada noted that US exports to Canada represented 92% or more of total US gypsum board exports between 2017 and January-November 2021. They also claimed that during that period, no other country accounted for more than 3% of US gypsum board exports. CT Canada also concluded that data available from ERQ responses corroborated the USITC data in demonstrating that Canada is the only viable outlet for US exports.Footnote 62

[88] CT Canada also argued that the established presence of US exporters in the Western Canadian market make it a natural and attractive dumping ground. CT Canada noted that both GP and USG/CGC indicated that channels of distribution remain unchanged and that GP and USG/CGC continue to supply to some of the largest gypsum distributors in Western Canada. CT Canada reiterated that US exporters continued to dump throughout the POR in order to hold onto market share in the Western Canadian market and asserted that the relationships with customers that led to significant dumping in the original investigation continue to exist.Footnote 63

Consolidation of Purchasers Widens the North American Footprint for Continued Dumping in Western Canada

[89] CT Canada noted that in 2018, the largest US distributor of gypsum board, GMS, acquired the largest Canadian gypsum board buyer and distributor, WSB Titan. They also noted that Foundation Building Materials Inc., one of the largest drywall distributors in North America, was acquired by a private equity firm in 2020. CT Canada claimed that the merger and acquisition of those two companies has resulted in consolidation of purchasing power and that the companies will be incentivized to use that increased purchasing power to leverage pricing available from dumped imports into Western Canada.Footnote 64

Parties contending that continued or resumed dumping is unlikely

[90] Both GP and USG/CGC made representations though their ERQ responses as well as in their respective case briefs and reply submission supporting their position that the dumping of certain gypsum board from the US in unlikely to continue or resume should the CITT’s finding expire.

[91] The main arguments detailed by GP and USG/CGC can be summarized as follows:

- Absence of Anti-dumping Duties Paid While Finding in Effect

- Role and Effects of the Remission Order

- Georgia-Pacific’s Sales Prices Do Not Demonstrate Dumping

- Demand Growth in the US Reduces Any Incentive for Dumping

- Strong Financial Performance of Exporters Reduces Any Incentive to Resume Dumping

- Minimal Excess Capacity Exists in the US That Could Be Used for Dumping into Western Canada

- No Basis to Expect Foreign Producers Will Switch Production of Other Goods to Subject Goods

- No Diversion Pressures or Circumvention Concerns

- Canadian Market Conditions Do Not Support Renewed Dumping

- The Western Canadian Market Faces a Shortage of Supply

- The Western Canadian Market is Supplied from Eastern Canada

- Consideration of Exports Must Distinguish Western Canada and Eastern Canada

- No Anti-dumping or Countervailing Measures Imposed in Canada Respecting Similar Goods

Absence of Anti-dumping Duties Paid While Finding in Effect

[92] GP asserted that despite the large volume of subject goods imported during the POR, virtually no anti-dumping duties were paid during that period. Specifically, GP noted that of the $146 million dollars worth of subject goods imported into Western Canada during the POR, only $342,636 of anti-dumping duties were paid, representing 0.2% of the value of imports. GP argued that the absence of duties paid and the fact that import volumes increased between 2019 and 2021 demonstrated that subject goods were able to fully compete with domestically produced goods and comply with SIMA restrictions.Footnote 65 USG also noted that nearly no SIMA duties were paid based on the compliance data and pointed out that exporters were still able to find customers to sell to at undumped prices while largely complying with the finding.Footnote 66

[93] GP noted that it was a major exporter of subject goods to Western Canada and that it had paid almost zero anti-dumping duties. Referencing its exporter ERQ response, GP also noted that its average selling prices to Western Canada in 2020 and the first nine months of 2021 were above GP’s average selling prices in the US in the same period.Footnote 67

[94] GP stated that the CITT’s finding followed a rapid change in the exchange rate between the US dollar and the Canadian dollar. GP claimed that the margins of dumping found in the original investigation could be attributed to the fact that the exchange rate from 2012 to 2013 was nearly 1:1, but had dropped approximately 25% between 2013 and 2015. GP indicated that exchange rates had remained relatively steady since 2016 and were not expected to significantly change in the foreseeable future. As such, GP argued that the original cause of the dumping was not likely to reoccur and trigger resumption of dumping.Footnote 68

Role and Effects of the Remission Order

[95] GP claimed that remitted duties are not evidence of continued or resumed dumping. GP contended that the anti-dumping protection from the finding and its consequences for imports of subject goods must take into account the remission order which was issued as a result of taking into account public interest considerations. GP stated that these two decisions are integrated and establish the level at which exporters are expected to sell into Canada. Noting that exporters have almost completely complied with the regime, GP argued that the conduct of exporters while the finding and remission order have been in place strongly supports that dumping is not likely to resumed should the finding be allowed to expire.Footnote 69

[96] GP claimed that the proceedings which led to the remission order arose because CertainTeed sought anti-dumping protection that would have allowed it to price at monopoly levels as the sole producer in Western Canada. GP stated that the remission order resulted from the CITT’s assessment of public interest issues and reflected the Canadian Government’s determination of a net level of import pricing that would provide appropriate protection against injury.Footnote 70

[97] GP argued that paragraph 37.2(1)(a) of SIMR, which refers to dumping that occurred during the finding, does not specifically address whether this assessment should be made on a gross or net basis in the unusual situation where a remission order had been issued. GP claimed that a purposive interpretation would favour the net approach because the Minister of Finance authorized exporters to price at that level. However, GP argued that even if the paragraph was not interpreted the manner it proposed, the exporters’ behaviour in relation to the remission order would still need to be examined as a relevant factor pursuant to paragraph 37.2(1)(j) which relates to any other factor relating to the behaviour of various parties such as exporters.Footnote 71

[98] GP noted that even if the finding were continued, the remission order would remain in force given it has no expiry date. As a result, GP argued that exporters would be able to continue to sell into Canada without paying anti-dumping duties by pricing at levels which reflect the combined effect of normal values and the remission order. GP concluded by pointing out that exporters had complied with the overall anti-dumping regime during the POR and that such behaviour could not be used to support an inference about likely future dumping in the event that the finding were allowed to expire.Footnote 72

Georgia-Pacific’s Sales Prices Do Not Demonstrate Dumping

[99] GP stated that CT Canada incorrectly interpreted GP’s data in its case brief. GP provided a table showing its confidential average sales values in both Eastern and Western Canada and provided its own confidential interpretation of the data.Footnote 73

Demand Growth in the US Reduces Any Incentive for Dumping

[100] GP stated that demand for construction materials has been high in the US and is expected to continue to be high in the foreseeable future. GP noted that an increase in domestic consumption of subject goods in the subject country has been a factor in past expiry reviews used to support a find of no continued or resumed dumping.Footnote 74

[101] USG/CGC stated that the US domestic market situation does not support resumed dumping as demand remains high in the US for gypsum wallboard products. USG/CGC argued that with a strong market in the US where it can sell at relatively high prices, little incentive exists to divert production away to Canada to sell at less profitable prices.Footnote 75

Strong Financial Performance of Exporters Reduces Any Incentive to Resume Dumping

[102] GP highlighted that it has been operating profitably and indicated its future profit expectations. GP argued that strong financial performance by foreign producers is an indicator that dumping is not likely to resume and noted that exporters are not incentivized to sell into Canada at dumped prices when they can do well selling domestically.Footnote 76

Minimal Excess Capacity Exists in the US That Could Be Used for Dumping into Western Canada

[103] Citing strong demand for gypsum board and high capacity utilization, GP argued that little excess capacity is available to produce additional volume for sale into Western Canada. To support this, GP referenced confidential Gypsum Association data. GP acknowledged plans to open a new plant in Texas but noted that it would also be closing a different plant in Texas. It noted the new plant would not be operational in 2022 and would take years to ramp-up once it is operational. It also claimed that the new plant would likely produce both subject and non-subject goods.Footnote 77

[104] USG/CGC contended that the only reason to reduce prices would be to fill unused capacity and that this is inapplicable given a number of confidential factors.Footnote 78

No Basis to Expect Foreign Producers Will Switch Production of Other Goods to Subject Goods

[105] GP claimed that foreign producers have no reason to change production from other gypsum products to the production of subject goods in order to dump into Canada. GP noted that during the POR, a certain percentage of its total production related to non-subject goods such as premium glass-mat faced gypsum board. It also noted that the non-subject goods it produced are important to the US market. As such, GP argued that this factor cannot be used as an indicator of any likelihood of resumption of dumping of the subject goods into Canada.Footnote 79

No Diversion Pressures or Circumvention Concerns

[106] GP noted that there are no anti-dumping or countervailing measures against US gypsum board or similar goods from countries other than Canada. GP argued that the fact that no other countries have a finding in place is a factor that weighs favorably in the conclusion that dumping is unlikely to resume. GP also argued that if a finding in another country were to be put in place, it would have little impact on exports to Canada. GP concluded by noting that no decisions regarding circumvention of a finding had been issued by Canada or any other jurisdiction and that this factor also supported a conclusion that dumping was unlikely to continue or resume.Footnote 80

Canadian Market Conditions Do Not Support Renewed Dumping

[107] Citing confidential Gypsum Association data, GP claimed that Western Canadian demand cannot be fulfilled by the sole domestic producer in that market and argued that this combined with expected demand growth in the Western Canadian market and declines in capacity means US producers will be able to continue to make sales at undumped prices.Footnote 81

[108] GP argued that its demand forecasts do not suggest that dumping is likely to resume. GP also noted that the only foreign competition in the Western Canadian market is between US exporters and that there is no risk that US exporters would need to lower their prices in order to compete with gypsum board from other countries.Footnote 82

The Western Canadian Market Faces a Shortage of Supply

[109] USG/CGC argued that the purpose of the expiry review is not to consider whether the expiration of the finding will result in increased imports but rather whether dumping will be likely if the finding expires. USG/CGC contended that strong demand with a shortfall in supply invites imports but does not invite dumped imports. Citing CGC’s ERQ response, USG/CGC noted that the Western Canadian market for gypsum board is undersupplied. USG/CGC argued that where demand is not being met, there is a strong incentive for imports to be priced at or above market prices and that there is no reason for importers to compete excessively or undercut domestic pricing given the current market conditions in Western Canada. As such, USG/CGC concluded that resumed dumping is highly unlikely in the event the duties are repealed.Footnote 83

The Western Canadian Market is Supplied from Eastern Canada

[110] USG/CGC contended that the current presence of Eastern Canadian production largely supplied by CGC in the Western Canadian market means dumping is unlikely to resume. USG/CGC argued that sales from Eastern Canada into Western Canada represent a fair market price in Canada and can provide a baseline for consideration of dumping and relevant price levels as they do not face dumped competition. As such, USG/CGC concluded that sales would likely be at or above undumped prices and that dumping is unlikely if the finding is rescinded.Footnote 84

Consideration of Exports Must Distinguish Western Canada and Eastern Canada

[111] GP argued that the estimated Canadian market for gypsum board, when separated into Western and Eastern Canada, showed that that Eastern Canada is a more attractive market for US exporters than the Western market. GP supported its argument citing confidential information which showed the estimated size of the Eastern Canadian market as compared to the total estimated Canadian Market.Footnote 85

No Anti-dumping or Countervailing Measures Imposed in Canada Respecting Similar Goods

[112] GP argued that the absence of anti-dumping or countervailing measures by Canada in respect of goods similar to the goods subject to this expiry review was a particularly relevant factor. GP noted that in 2018, CT Canada had sought anti-dumping protection concerning 54” gypsum board from the US but that the Canadian authorities had rejected CT Canada’s request. GP claimed that CT Canada’s original complaint as well as subsequent CBSA and CITT proceedings have included extensive evidence regarding domestic production in Eastern Canada along with exports from GP, USG and other US producers. GP contended that despite that evidence, no anti-dumping measures have been sought or granted in Canada with respect to the Eastern Canadian market. GP concluded by noting that pricing in the Eastern Canadian market had not been a problem from an anti-dumping perspective and reasoned that the higher market prices prevailing in Western Canada should not give rise to any concerns.Footnote 86

Consideration and analysis - dumping

[113] In making a determination under paragraph 76.03(7)(a) of SIMA whether expiry of the finding is likely to result in the continuation or resumption of dumping of the goods, the CBSA may consider factors identified in subsection 37.2(1) of the SIMR, as well as any other factors relevant in the circumstances.

Likelihood of continued or resumed dumping

[114] Guided by the aforementioned factors and having considered the information on the administrative record, the following list represents a summary of the factors analyzed by the CBSA in conducting this expiry review investigation with respect to dumping:

- Dumping of Subject Goods During the POR

- Substantial Imports of Subject Goods During the POR

- Western Canada Remains an Important Market for US Exporters

- Significant Excess Capacity in the US

- US Market Demand

- Differences Between the Price of Exports to Western and Eastern Canada

[115] Each factor listed is discussed in the sections that follow. As indicated earlier in this report, the CBSA received an ERQ response from the complainant (CT Canada), three ERQ responses from other Canadian producers located outside Western Canada (Cabot, AWLP, CGC), one ERQ response from an importer (GP Canada), and three ERQ responses from US exporters (CT US, GP US, USG). While two of the Canadian producers also acted as importers (CGC, CT Canada), a response to the importer ERQ was not required since they responded to the Canadian Producer ERQ. Case briefs were received from CT Canada, Cabot, USG/CGC, and GP. Reply submissions were also received from CT Canada and GP. The CBSA relied on the ERQ responses and information submitted by these parties, as well as other information on the administrative record for purposes of this expiry review investigation.

Dumping of Subject Goods During the POR

[116] In accordance with subsection 2(1) of SIMA, goods are considered to be dumped when the normal value of the goods exceeds the export price of the goods. Conversely, subparagraph 37.2(1)(a)(iv) of SIMR refers to goods as being non-dumped when the export prices exceed the normal values of the goods.

[117] As explained earlier in the Enforcement Data section, the SIMA duty remitted amount represents the portion of dumping calculated as the difference between the normal values and the export prices, but includes only the amount of dumping that exceeds the remission order reference values. The SIMA duty assessed amount represents the amount of dumping equal to the remission order reference value less the export price. When those two amounts are combined, the total SIMA duty amount shown in Table 3 below represents the total amount by which the normal values exceeded the export prices, in other words, the total margin of dumping.

| 2018 | 2019 | 2020 | 2021 (Jan 1 - Sep 30) | |

|---|---|---|---|---|

| Value of subject goods (CAD) | $41,972,980 | $35,545,475 | $36,896,741 | $31,948,568 |

| SIMA duty assessed (CAD) | $36,911 | $148 | $206,231 | $99,346 |

| SIMA duty remitted (CAD) | $0 | $4,184,637 | $3,956,787 | $3,155,163 |

| Total SIMA duty (CAD) | $36,911 | $4,184,785 | $4,163,018 | $3,254,509 |

| Average margin of dumping (%) | 0.1% | 11.8% | 11.3% | 10.2% |

[118] As noted in the CBSA’s recent Statement of Reasons respecting its expiry review determination on large line pipe, remission of SIMA duties is typically only used in extraordinary circumstances and it is not used to override the legislated intent of SIMA, which is to remedy the injury caused by dumped goods to domestic producers of competing goods. The CBSA determines whether goods are dumped in accordance with the provisions of SIMA and the SIMR, as referenced above. The CBSA notes that the concept of duties paid versus those remitted as a result of a remission order is not provided for in determining whether goods are dumped in accordance with SIMA and SIMR. The CBSA’s approach is consistent with that of the CITT, which stated in its Finding and Reason respecting gypsum: “There is no “good” or “bad”, “passive” or “aggressive” dumping. There is only dumping as it is defined under SIMA and the underlying international agreement”.Footnote 88

[119] Despite the finding in place, US exporters continued to dump subject goods throughout the entire POR as shown in Table 3 above. Moreover, between January 2019 and September 2021, the average margin of dumping was significant, ranging between 10.2% and 11.8%. The significant amount of dumping that occurred during the POR demonstrates an inability or unwillingness by US exporters to sell gypsum board into Western Canada at undumped prices.

Substantial Imports of Subject Goods During the POR

[120] During the POR, substantial volumes of subject goods continued to be imported into Western Canada with volumes continuing to trend upwards towards the end of the POR. As previously noted with respect to Table 1 and Table 2, both the enforcement data and data submitted by importers in response to the CBSA’s ERQ showed the same general trends in import volumes over the period.

[121] The chart above shows that the volume of subject imports decreased in 2019 but has consistently trended upward in the years following, including in the most recent period. According to the data provided by the importers in their ERQ responses, subject imports fell by 37% in 2019, increased by 8% in 2020, and are expected to rise by 32% in 2021 when annualizing their data. Enforcement data shows a smoother transition with imports decreasing by 11% in 2019, increasing by 11% in 2020, and an expectation that imports will increase by 18% in 2021 based on annualized data.

[122] Based on the above, the data shows that a significant volume of subject goods were imported throughout the POR and that volumes were trending upward for most of the period. The previous section also showed that these significant imports into Western Canada were dumped throughout the POR. The consistent trends of dumping significant volumes of subject goods into Western Canada over the majority of the POR, including in the most recent period, indicates that dumping is likely to continue should the finding be rescinded.

Western Canada Remains an Important Market for US Exporters

[123] As noted above, US exporters continued to export significant volumes of subject goods during the POR which demonstrates their continued interest in the Western Canadian market. Those import volumes combined with market share data and the lack of US exports to other countries, discussed below, further demonstrates that Western Canada remains an important market for US exporters of subject goods. Moreover, the US is essentially the only source of imports of gypsum board in commercial quantities into the entire Western Canadian market.

[124] Import data presented earlier in Table 1 shows that subject exports from the US represented 99.5% of the total imports into Western Canada during the POR. The confidential details of that data also show that exports from GP US to its related importer GP Canada combined with the exports from USG to its Canadian subsidiary CGC accounted for the vast majority of the total volume of subject goods imported during the POR. While the size of the estimated apparent market in Western Canada fluctuated over the POR, the combined market share of GP and USG/CGC remained relatively consistent throughout the period.

[125] Between 2018 and 2020, GP’s share of the Western Canadian market increased steadily. In addition, data for 2021 shows that GP has managed to maintain that market share growth. The trend in GP’s market share growth is directly attributable to the increase in its imports over the POR.

[126] With respect to USG/CGC, their ability to maintain market share in Western Canada during the POR was not directly tied to the sales of subject exports. While CGC continued to import significant volumes from USG throughout the POR, the volumes between 2019 and 2021 were significantly less than what was imported in 2018. This is due to the fact that USG/CGC moved towards supplementing their sales of subject imports with Canadian gypsum board produced outside Western Canada. Specifically, the goods produced in Eastern Canada were sourced from CGC’s Ontario facility along with goods produced for CGC by AWLP in New Brunswick. The willingness to absorb the increased costs associated with sourcing goods from Eastern Canadian versus US plants located in much closer proximity to the Western Canadian market demonstrates that the Western Canadian market remains an important market to USG/CGC.

[127] In the event the finding is rescinded, it is important to note that USG/CGC would likely cease to source large volumes of goods from Eastern Canada and would likely resume supplying the Western Canadian market almost entirely with subject imports. In its October 2020 order not to conduct an interim review, the CITT found that CGC’s shipments from Eastern to Western Canada resulted from the implementation of anti-dumping duties. The CITT noted that no evidence had been presented showing that such shipments would continue absent the duties in place. Conversely, the CITT also noted that CGC had itself admitted in its request for the interim review that it was more cost efficient to supply the Western Canadian market from USG plants located in the Pacific Northwest and Midwest US.Footnote 89

[128] Information on the administrative record also shows that Canada is the primary target market for US exports for gypsum board. As noted earlier by CT Canada, export data from the USITC showed that during the POR, US exports to Canada consistently accounted for 92% to 93% of total US paper-faced gypsum board exports.Footnote 90 In the second quarter of 2021, Global Gypsum reported that exports of gypsum wallboard to Canada had reached 95% of total US exports.Footnote 91 Data supplied by the exporters in response to the CBSA’s ERQ also showed very little exports to countries other than Canada during the POR.

Significant Excess Capacity in the US

[129] Based on confidential capacity and domestic shipment information available from the Gypsum Association and public information regarding exports available from USITC, capacity utilization rates for US producers of gypsum board consistently rose over the POR and, as a result, excess production capacity fell. Despite the significant decrease in excess production capacity in the US over the POR, excess capacity estimated for the most recent period remains many times the entire size of the Western Canadian market for certain gypsum board.Footnote 92

[130] As noted earlier in the arguments put forth by CT Canada, the capacity data submitted by the exporters in their ERQ appendices did not present the true maximum capacity to produce gypsum board. Rather, both USG and CGC provided annual production capacity figures in their respective appendices which they calculated by taking into account annual production resulting in capacity figures which fluctuated over the POR. These fluctuating figures stood out given that both exporters had stated in their respective ERQ responses that neither company had added capacity nor had they closed any facilities during the POR.Footnote 93

[131] While no further information regarding actual maximum capacity was available from the information submitted by USG, GP US provided a reference to its maximum capacity in its reply brief for 2020 based on information it submitted to the Gypsum Association. In order to consider the estimated excess capacity of the two main exporters of subject goods to Canada, the CBSA relied upon GP US’s company specific information submitted to the Gypsum Association. As similar information was not available with respect to USG, the CBSA relied upon the total capacity of USG reported in the Gypsum Directory. The CBSA used that capacity information combined with the production data submitted by both USG and GP US to estimate the excess capacity for those two exporters throughout the POR.Footnote 94

[132] The data for USG and GP showed a consistent trend with the total estimated US excess capacity whereby estimated excess capacity fell significantly over the POR. Despite that fall, total estimated excess capacity from those two exporters remains much greater than the entire size of the Western Canadian market.

[133] In the event the finding is rescinded, any of the facilities operated in the US would be able to export to Canada. However, given that some of the facilities are located far away from the Western Canadian market, such as those in the Southeastern US in states like Florida, the CBSA also conducted an analysis of excess capacity based on the current US facilities which have normal values established. While it is possible that other facilities near to those which do not have normal values would ship absent the finding, it is even more likely that the facilities currently with normal values and that have exported in the past would export to Western Canada in the future.

[134] The excess capacity analysis for those facilities with normal values was based on the plant specific capacity figures available in the Gypsum Directory for the two most recent years along with the estimated capacity utilization rates for each exporter. The capacity utilization rates were calculated as noted above and based on the Gypsum Association capacity figures and actual production data supplied by the exporters. The results of the analysis showed a significant excess amount of capacity available from those facilities which was nearly equal to the entire size of the estimated apparent Western Canadian market.

[135] Based on the analysis discussed in the preceding paragraphs, there is significant excess capacity for gypsum board in the US. Given the dumping that occurred and the significant volume of subject goods exported over the POR, significant excess capacity in the US would likely result in even greater volumes of subject goods being dumped into Western Canada should the finding be rescinded.

US Market Demand

[136] Total US domestic shipments of gypsum board increased each year throughout the entire POR.Footnote 95 As shown earlier in Table 1, imports of subject goods into Canada decreased significantly in 2019 and then increased annually over the remainder of the POR. Given that subject imports rose over most of the POR at the same time when demand was also significantly increasing in the US, there does not appear to be a strong correlation between US demand and export volumes to Western Canada. This is likely attributable to the fact that the US market as a whole is exponentially larger than the Western Canadian market.

[137] Despite almost no correlation between US demand and Western Canadian import volume, future demand in the US would have an impact on excess capacity which could effect the potential additional volumes of subject goods available for export to Western Canada. The following paragraphs summarize expectations regarding US demand in the near-term as expressed by interested parties and address the impact such expectations could have the availability of gypsum board from the US.

[138] GP US submitted a confidential forecast regarding US demand for gypsum board in the coming years. To support its forecast, GP US provided a set of charts based on information published by a variety of sources such as RISI, IHS Markit, US Census Bureau, etc. According to the forecast and GP US’s own mass demand-supply balance report, the information demonstrated that excess capacity would remain in significant amounts when compared to the annual estimated size of the apparent Western Canadian market.Footnote 96

[139] USG provided little information with regards to its forecasts for the US gypsum board market in the near term. In considering USG’s limited forecast for US market demand and the capacity and production data it provided in its ERQ appendices, USG’s excess capacity in the near term is still expected to be significant when compared to the annual estimated size of the apparent Western Canadian market.Footnote 97