SPT 2021 IN: Certain small power transformers

Statement of Reasons—Initiation of investigation

Concerning the initiation of investigation into the dumping of certain small power transformers originating in or exported from Austria, Chinese Taipei, and South Korea.

Decision

Ottawa,

Pursuant to subsection 31(1) of the Special Import Measures Act, the Canada Border Services Agency initiated an investigation on April 15, 2021, respecting the alleged injurious dumping of certain small power transformers originating in or exported from Austria, Chinese Taipei, and South Korea.

On this page

Summary

[1] On February 23, 2021, the Canada Border Services Agency (CBSA) received a written complaint from Transformateurs Delta Star Inc., Northern Transformer, PTI Transformers Inc., and PTI Transformers L.P. (hereinafter, the complainants) alleging that imports of certain small power transformers (SPT) originating in or exported from Austria, the Separate Customs Territory of Taiwan, Penghu, Kinmen and Matsu (Chinese Taipei), and South Korea are being dumped. The complainants alleged that the dumping has caused injury and is threatening to cause injury to the Canadian industry producing like goods.

[2] On March 16, 2021, pursuant to paragraph 32(1)(a) of the Special Import Measures Act (SIMA), the CBSA informed the complainants that the complaint was properly documented. The CBSA also notified the Governments of Austria, Chinese Taipei, and South Korea that a properly documented complaint had been received.

[3] The complainants provided evidence to support the allegations that SPT from Austria, Chinese Taipei, and South Korea have been dumped. The evidence also discloses a reasonable indication that the dumping has caused injury and is threatening to cause injury to the Canadian industry producing like goods.

[4] On April 15, 2021, pursuant to subsection 31(1) of SIMA, the CBSA initiated an investigation respecting the dumping of SPT from Austria, Chinese Taipei, and South Korea.

Interested parties

Complainants

[5] The name and address of the complainants are as follows:

Northern Transformer Corporation

245 McNaughton Rd E

Maple, ON L6A 4P5

PTI Transformers Inc.

1155 Park St

Regina, SK S4N 4Y8

PTI Transformers L.P.

101 Rockman St

Winnipeg, MB R3T 0L7

Transformateurs Delta Star Inc.

860 Lucien Beaudin

Saint-Jean-sur Richelieu, QC J2X 5V5

Northern Transformer Corporation

[6] Northern Transformer Corporation (Northern) is a manufacturer of SPT that has been located in Maple, Ontario, since 2016. Northern manufactures power transformers throughout the range covered by the scope of this complaint, and up to 200 mega volt amperes (MVA) and 240 kilo volts (kV).Footnote 1

[7] Northern was founded in 2012 when new ownership led by Giovanni Marcelli purchased the assets of Northern Transformer Inc., which was originally incorporated in Concord, Ontario in 1981 by Eric Borgenstein, Doug Hazelton and William Kemp.Footnote 2

PTI Transformers Inc.

[8] PTI Transformers Inc. and PTI Transformers L.P. (collectively, “PTI”), is the largest fully Canadian-owned manufacturer of power transformers in Canada. PTI produces power transformers at two facilities in Regina and Winnipeg. The Regina factory can produce SPT to as large as 40 MVA. The Winnipeg facility is a modern plant producing SPT throughout the range covered by this complaint, as well as up to 750 MVA.Footnote 3

[9] PTI was founded in 1989 in Regina, Saskatchewan. In 2015, PTI acquired the former CG Power Winnipeg transformer production facility and has been in operation since 1979. The Winnipeg facility was first established in 1946 when Pioneer Electric began producing small distribution transformers. The facility changed ownership over the years, from Pioneer to Schneider Electric, Pauwels Canada, and CG Power Systems Canada before its acquisition by PTI.Footnote 4

Transformateurs Delta Star Inc.

[10] Transformateurs Delta Star Inc. (Delta Star Canada) is a wholly owned subsidiary of Delta Star Inc., which is an employee-owned company, with its headquarters located in the United States of America (USA). Delta Star Inc. has three production facilities between the USA and Canada, the Canadian facility is located in Saint-Jean-sur-Richelieu, Québec. The facility in Québec is capable of producing the full range of transformers which are the subject of this complaint, as well as larger transformers of up to 175 MVA and 345 kV.Footnote 5

Other Canadian producers

[11] The following Canadian producers also manufacture SPT:

Transformateurs Pioneer Ltée.

612, Bernard Rd

Granby, QC J2J 0H6

Tel: 450-378-9018

Stein Industries Inc.

19 Artisans Cres

London, ON N5V 5E9

Tel: 519-659-3659

Transformateurs Pioneer Ltée.

[12] Transformateurs Pioneer Ltée. (Pioneer) is a subsidiary of Spire Power Solutions (Spire). Spire provides a full range of solutions to meet the most demanding needs of the commercial, industrial, and utility markets for power and distribution transformers.Footnote 6 As a part of Spire, Pioneer designs and manufactures liquid-filled transformers for unique applications.Footnote 7 Pioneer submitted a letter expressing its support to the complaint.Footnote 8

Stein Industries Inc.

[13] Stein Industries Inc. (Stein) designs and manufactures power and distribution transformers, preventive auto transformers, transit rectifier power transformers along with transformer rectifiers for electrostatic precipitators. It also offer expertise and guidance in designing to the customer’s specifications and requirements.Footnote 9 Stein submitted a letter expressing its support to the complaint.Footnote 10

Trade unions

[14] Northern’s workforce is represented by Unifor.Footnote 11

[15] PTI’s Winnipeg workforce is represented by the United Steel Workers.Footnote 12

Exporters

[16] The CBSA identified 11 potential exporters of the subject goods from CBSA import documentation and from information submitted in the complaint. All of the potential exporters were asked to respond to the CBSA’s Dumping request for information (RFI).

Importers

[17] The CBSA identified 12 potential importers of the subject goods from CBSA import documentation and from information submitted in the complaint. All of the potential importers were asked to respond to the CBSA’s Importer RFI.

Product information

DefinitionFootnote 13

[18] For the purpose of this investigation, subject goods are defined as:

Liquid dielectric transformers having a top power handling capacity equal to or greater than 3,000 kilovolt amperes (kVA) (3 megavolt amperes (MVA)), and less than 60,000 kilovolt amperes (kVA) (60 megavolt amperes (MVA)), and having a nominal high voltage rating of greater than 34.5 kilovolts (kV), whether assembled or unassembled, complete or incomplete, originating in or exported from the Republic of Austria, the Separate Customs Territory of Taiwan, Penghu, Kinmen and Matsu (Chinese Taipei), and the Republic of Korea.

Additional product informationFootnote 14

[19] For greater clarity, the subject goods include but are not limited to transformers manufactured to meet CSA standard C88-16, “Power transformers and reactors,” and superseding or equivalent standards, and similar proprietary specifications and standards that may be established by a customer for power transformers whether or not expressly based on or incorporating CSA C88-16.

[20] Incomplete SPT are subassemblies consisting of the active part and any other parts attached to, imported with, or invoiced with the active parts of the SPT. The “active part” of the SPT consists of one or more of the following when attached to or otherwise assembled with one another: the steel core or shell, the windings, electrical insulation between the windings, and/or the mechanical frame for an SPT.

[21] The product definition encompasses all SPT regardless of name designation, including but not limited to: Generation Station/Generator Step-Up Transformers, Step-Down Transformers, Auto-Transformers, Interconnection Transformers, Voltage Regulator Transformers, High-voltage Direct Current (“HVDC”) Transformers, and Mobile Transformers.

[22] The subject goods do not include reactors, as reactors are not like SPT. Reactors are used at the terminal end of a transmission line to neutralize the reactive power generated by the line capacitance. Rather than transform voltage from one level to another, as SPT do, reactors reduce voltage drop by consuming reactive power. Reactors, therefore, have very different end uses than SPT. Reactors are also produced differently than SPT. Reactors contain, in general, only one winding and are based on a completely different core concept than SPT. SPT, on the other hand, typically have more than one winding.

[23] For greater clarity, the subject goods also do not include fully assembled mobile substations but do include SPT that are designed to be incorporated into mobile substations.

Product characteristics

[24] All SPT are capital goods that are made to order from a customer’s specifications based on the customer’s particular needs. They are used to increase, maintain or decrease electric voltage in high voltage transmission and distribution systems. Broadly speaking, the distribution of electricity requires transformers to first increase (or “step-up”) the voltage from the source of generation (e.g., a hydro dam) so that it can be transmitted more efficiently at higher voltages; and to second decrease (or step-down) voltage for purposes of distribution to users. SPT are also used to connect different parts of transmission and distribution networks.

[25] SPT use electromagnetic induction between circuits to increase, decrease or transfer the output voltage levels being transmitted. Induction occurs when the electromagnetic field caused by electricity moving through a conductor crosses a second electrical conductor and generates a voltage in the second conductor even though the two conductors are not directly connected. This requires a fluctuating magnetic field generated by alternating current entering into an input conductor.

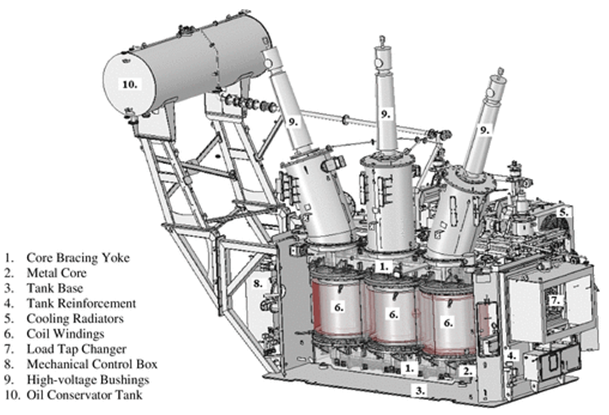

[26] SPT all share certain basic, key physical characteristics. All SPT have at least one “active part” where the electromagnetic induction occurs. This consists of a core, winding, electrical insulation between the windings, and a clamping system to hold the internal assembly together. The internal assembly is placed into a metal tank that is filled with an insulating media and has a cooling system attached. A diagram showing the major internal components of an SPT follows:

Figure 1—SPT showing major internal components

- Core bracing yoke

- Metal core

- Tank base

- Tank reinforcement

- Cooling radiators

- Coil windings

- Load tap changer

- Mechanical control box

- High-voltage bushings

- Oil conservator tank

[27] The core of an SPT is made of grain-oriented silicone steel and is laminated with an inorganic coating. The silicone steel is layered in pieces and shaped into the legs and yokes of the core. Cores typically consist of two, three, four, or five legs depending on the number of phases, capacity, and transport restrictions. SPT below 10 MVA may sometimes use wound cores in some applications where the core laminations are wound around the windings instead of stacked into legs and yokes.

[28] Upon the core are windings made of copper conductor covered in insulation paper and/or enamel coating to insulate the turns from one another. They provide both electrical power input and output. There are typically windings for each voltage level and there can also be one or more windings for voltage regulation. Winding can be done through layer winding, helical winding, disc winding or interleaved disc winding. The winding method employed depends on the capacity, voltage and tap range of each SPT as specified.

[29] The core and windings are placed in a tank, which protects the active parts of the SPT. The tank must be strong enough to withstand an internal pressure of a full vacuum and external factors such as weather. The tank is usually filled with fluid (typically oil) for cooling and insulation. The size of the tank varies depending on the size of the core, required voltage clearances, number of windings and type of regulation, which itself is a function of the energy being transformed and customer specification.

[30] Lastly, all SPT possess a cooling system which ensures that heat is dissipated and prevents exceeding the specified temperature rise in the SPT. The cooling method is determined by the customer’s requirements and use. SPT can employ several different cooling systems including: natural oil cooling/natural air cooling (often abbreviated as “ONAN”), natural oil cooling/forced air cooling (“ONAF”), forced oil cooling/forced air cooling (“OFAF”), directed oil cooling/forced air cooling (“ODAF”), and forced oil cooling/forced water cooling (“OFWF”). Other insulating fluids, such as ester-based fluids or silicone, will have the ‘O’ abbreviation substituted with other characters identifying the fluid (i.e. K or L).

[31] A number of raw materials are common to the construction of all SPT. The most significant raw materials used are copper, electrical (magnetic) steel, tank steel, and insulation material. Oil is also a very important insulation element often included in the sale of the SPT or purchased separately by the customer.

[32] Within the class of goods of SPT, there are 16 common customizable features or product characteristics, which can be manufactured to correspond to specified customer criteria. The precise specification required for each of these features may significantly affect the overall cost of producing the required transformer.

[33] The most common customizable features are:

- Maximum MVA rating

- Type

- Voltage

- Basic impulse level (BIL) voltage

- Number of windings

- Number of phases (either 1 or 3 phase)

- Impedance

- Regulation by tap changer

- Noise level

- Load losses (expressed in kilowatts)

- No load losses (expressed in kilowatts)

- Cooling class

- Overload capability requirement

- Frequency

- Type of current to be transformed (AC current or DC current)

Production processFootnote 15

[34] The production of SPT normally has five main steps, which entails: (1) design; (2) core fabrication; (3) coil fabrication and coil-and-core assembly; (4) tanking; and (5) testing.

1. Design

[35] The first step in the production process is the design of the SPT. As a customized product, engineers must set out the electrical and mechanical design of the SPT, subject to customer approval. The engineer prepares mechanical drawings, detailed and transport drawings, schematics control designs, cabling diagrams and control cabinet diagrams.

2. Core fabrication

[36] After the design phase, the manufacturing phase begins. The first step in the manufacturing phase is creating the core of the SPT. The core is made by cutting laminated electrical steel sheets and stacking them one upon the other in a well-defined way. The stacked sheets are then pressed together, and positioning equipment is used to set the core in an upright position. As noted above, SPT below 10 MVA may sometimes use wound cores where the core laminations are wound around the windings instead of stacked, although the functionality of the transformer remains the same.

3. Coil fabrication and coil-and-core assembly

[37] The next step is to prepare the windings (coil fabrication) and coil-and-core assembly. The windings are fabricated from copper wire and covered with insulation paper. They are dried to eliminate all moisture contents. The particular winding method employed can vary depending on the particular SPT design. The core-and-coil assemblies are held together by a specific design system.

4. Tanking

[38] The tank is usually painted inside and out to prevent corrosion. After assembly, the unit is dried a second time to eliminate any moisture. The coil-and-core assembly is then placed into a steel tank. The tank is equipped with a cooling system. The cooling media is the electrical insulating fluid. The cooling system used depends on the application of the SPT as specified by the customer.

5. Testing

[39] After the manufacturing steps are complete, the SPT is subjected to rigorous testing in accordance with the applicable standards defined by the customer before it is sent for delivery to the customer. For purposes of testing prior to shipment to the customer, the cooling media (usually insulating oil) must be added to the tank. However, for purposes of shipping, the cooling media is often drained and refilled on site with a local supply due to the added weight. In the case of imported SPT from the named sources, which must be shipped a much longer distance overseas and loaded and offloaded at ocean ports, the Complainants understand that the cooling media (e.g. insulating oil) is drained at the foreign factory and refilled onsite in Canada from a local supply.

Product useFootnote 16

[40] All SPT are used to transform voltage from one level to another as a result of the electromagnetic induction coils. There are three types of applications for SPT in terms of how they transform voltages. SPT can be applied as a Generation Station Unit, as an Auto-Transformer or as a Substation Transformer. Generation Station Units are primarily used to step voltage from a generating station up to a high voltage transmission grid. Depending on the secondary voltage, an Auto-Transformer is sometimes used after the generator transformer to further step up the voltage. Auto-Transformers are also used to interconnect systems operating at different voltage classes. The third use of an Auto-Transformer is to gradually step voltage down to the substation units. Auto-Transformers work in both the step-up and step-down operations. Substation Transformers step the voltage down to the distribution grid. In general, the difference between Auto-Transformers and Substation Transformers is in the design. Substation Transformers are galvanically separated whereas an Auto-Transformer is based on common winding in two voltage systems.

Classification of imports

[41] Prior to 2019, imports into Canada of the subject goods were normally classified under the following tariff classification numbers: 8504.22.00.20 and 8504.23.00.00.

[42] Since 2019, imports into Canada of the subject goods are normally classified under the following tariff classification numbers: 8504.22.00.20 and 8504.23.00.10.

[43] Incomplete SPT and parts and components thereof may also be imported under the following tariff classification numbers: 8504.90.90.10, 8504.90.90.82 and 8504.90.90.90.

[44] The listing of tariff classification numbers is for convenience of reference only. The tariff classification numbers may include non subject goods. Also, subject goods may fall under tariff classification numbers that are not listed. Refer to the product definition for authoritative details regarding the subject goods.

Period of investigation

[45] The CBSA typically selects a period of investigation (POI) that covers a twelve-month period. However, due to the nature of the subject goods, the CBSA has selected an eighteen-month period POI from July 1, 2019 to December 31, 2020, for the purposes of the dumping investigation.

Like goods and class of goods

[46] Subsection 2(1) of SIMA defines “like goods” in relation to any other goods as goods that are identical in all respects to the other goods, or in the absence of any identical goods, goods the uses and other characteristics of which closely resemble those of the other goods.

[47] In considering the issue of like goods, the Canadian International Trade Tribunal (CITT) typically looks at a number of factors, including the physical characteristics of the goods, their market characteristics, and whether the domestic goods fulfill the same customer needs as the subject goods.

[48] In its past inquiry involving liquid dielectric transformers, the CITT determined that domestically produced power transformers with a top power handling capacity of 60 MVA or greater constituted a single class of “like goods” in relation to the subject goods.Footnote 17 This position was maintained in the liquid dielectric transformers Expiry Review in 2018, as indicated by its Order and Reasons.Footnote 18

[49] While all SPT have similar characteristics and uses, they are capital goods that are made to order from a customer’s specifications based on the customer’s particular needs. The goods produced in the named sources are used to increase, maintain or decrease electric voltage in high voltage transmission and distribution systems. Both the goods in Canada and in the named sources are produced following substantially the same production process and follow the same key steps of design. Given the same specifications, the goods produced by the complainants are completely substitutable with the subject goods imported from Austria, Chinese Taipei and South Korea.

[50] Although the goods produced by the Canadian industry may or may not be considered identical in all respects to the subject goods imported from the named sources, the CBSA has concluded that the Canadian goods closely resemble the subject goods. Further, after reviewing the raw material used to produce the goods, the production process, the physical characteristics of the goods, the end-uses and all other relevant factor, the CBSA is of the opinion that the subject goods constitute only one class of goods.

The Canadian industry

[51] The complaint includes data on domestic production and on domestic sales of SPT by the complainants, Stein,Footnote 19 and estimates of Pioneer total Canadian production.Footnote 20 Based on the available evidence, the CBSA is satisfied that the complainants and the supporting producers account for all known production of like goods.

Standing

[52] Pursuant to subsection 31(2) of SIMA, the following conditions must be met in order for an investigation to be initiated:

- the complaint is supported by domestic producers whose production represents more than 50% of the total production of like goods by those domestic producers who express either support for or opposition to the complaint and

- the production of the domestic producers who support the complaint represents 25% or more of the total production of like goods by the domestic industry

[53] As the complainants and the supporting producer represent all known production of like goods in Canada, the CBSA is satisfied that the standing requirements pursuant to subsection 31(2) of SIMA have been met.

Canadian market

[54] The complainants estimated the domestic market by supplementing their own internal sales information with the information provided by Stein, and their own estimates of Pioneer’s Canadian production. Using Statistics Canada data, the complainants estimated the total volume of imports of SPT from Austria, Chinese Taipei, South Korea, and all other countries for the full years of 2018 to 2020.Footnote 21

[55] The tariff classification numbers for SPT include both subject and non-subject goods. As such, the complainants made a number of adjustments in an effort to remove non-subject goods.Footnote 22

[56] The CBSA conducted its own analysis of imports of the goods based on CBSA’s import data, which demonstrated similar trends and volumes with respect to imports of SPT, compared to information provided in the complaint, with the notable disparity being the estimated imports from South Korea. This is due to the fact that the CBSA was able to identify imports that were subject to the CBSA’s Transformers measure in forceFootnote 23 and therefore were not subject to this case. Overall, the CBSA’s import data for the POI supports the complainants’ claim that imports of subject goods into Canada from named sources exceed the negligibility threshold of three percent.

[57] The table below summarizes the CBSA’s estimate of imports:

| Source | 2018 | 2019 | 2020 | H2 2019 | July 1, 2019 to Dec 31, 2020 (POI) |

|---|---|---|---|---|---|

| Austria | 7.8% | 6.9% | 0.0% | 11.0% | 5.2% |

| Chinese Taipei | 4.7% | 3.7% | 3.6% | 5.9% | 4.7% |

| South Korea | 21.1% | 30.1% | 33.4% | 26.0% | 29.9% |

| United States | 21.0% | 24.6% | 22.8% | 29.0% | 25.7% |

| All other countries | 45.5% | 34.8% | 40.2% | 28.1% | 34.4% |

| Total imports | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% |

[58] Detailed information regarding the volume and value of imports of SPT and domestic production cannot be divulged for confidentiality reasons. The CBSA, however, has prepared the following table to show the estimated import share of subject goods in Canada as well as the Canadian market as a whole.Footnote 24

| 2018 | 2019 | 2020 | |

|---|---|---|---|

| Domestic industry1 | 39.6% | 37.9% | 50.4% |

| Austria | 4.7% | 4.3% | 0% |

| Chinese Taipei | 2.8% | 2.3% | 1.8% |

| South Korea | 12.8% | 18.7% | 16.6% |

| Imports from other countries | 40.1% | 36.9% | 31.2% |

| Total imports | 60.4% | 62.1% | 49.6% |

| Total apparent Canadian market | 100.0% | 100.0% | 100.0% |

| 1As per the information provided in the complaintFootnote 25 | |||

[59] The CBSA will continue to gather and analyze information on the volume of imports during the POI of July 1, 2019 to December 31, 2020, as part of the preliminary phase of the dumping investigation and will refine these estimates.

Evidence of dumping

[60] The complainants alleged that the subject goods from Austria, Chinese Taipei and South Korea have been injuriously dumped into Canada. Dumping occurs when the normal value of the goods exceeds the export price to importers in Canada.

[61] Normal values are generally based on the domestic selling price of like goods in the source of export where competitive market conditions exist or as the aggregate of the cost of production of the goods, a reasonable amount for administrative, selling and all other costs, and a reasonable amount for profits.

[62] The export price of goods sold to importers in Canada is generally the lesser of the exporter’s selling price and the importer’s purchase price, less all costs, charges and expenses resulting from the exportation of the goods.

[63] Estimates of normal values and export prices by both the complainants and the CBSA are discussed below.

Normal values

Complainants’ estimatesFootnote 26

[64] The complainants submitted that it is not possible nor appropriate to calculate normal values pursuant to section 15 of SIMA. Specifically, it was argued that while all transformers have similar characteristics and uses, they are highly customized goods made to customer specification and therefore, each transformer is unique. As a result, it is not possible to compare sales of SPT in the named sources to sales of subject goods, for the purpose of estimating normal values pursuant to section 15 of SIMA. This position is consistent with the CBSA’s finding in the liquid dielectric transformers (2012), where the CBSA found that the goods produced by producers in named sources were “custom-made, produced to the specific needs of each of its customers and therefore, there are no domestic sales of like goods. As such, the complainants were unable to determine normal values pursuant to section 15 of SIMA based on domestic sales of like goods”.Footnote 27

[65] As a result, the complainants provided estimated normal values using a constructed cost approach based on the methodology prescribed under paragraph 19(b) of SIMA, calculated based on the aggregate of estimates of the cost of production of the subject goods, a reasonable amount for general, administrative, selling (GS&A), and other costs, and a reasonable amount for profits. The complainants’ estimated normal value, based on the methodology in paragraph 19(b) of SIMA, was constructed as detailed in the following paragraphs.

[66] The complainants estimated 17 transaction-specific normal values based on the methodology of paragraph 19(b) of SIMA, based on their own cost information adjusted to reflect conditions in the named sources. For all of the estimated normal values, at least one of the complainants submitted a competing bid to the customer. When submitting a competing bid to the customer, the complainants calculated, based on the specifications for that particular transformer, detailed estimates for the cost of raw materials, labour, and overhead. Where more than one producer participated in a bid, the complainants averaged the material, labour, and overhead from those producers in order to provide an average of the costs of production.Footnote 28

[67] Raw material costs were estimated based on the complainants’ estimated cost for each bid lost to an exporter from the named sources. Given the precise and mandatory nature of the specifications and requirements stipulated by procuring authorities, the complainants submitted that it is reasonable to assume that the quantities of materials used by producers in the named sources would not be materially different than the corresponding estimates by the complainants in their bid costing. Additionally, the key raw materials used in the production of SPT – electrical steel, core steel, and copper – are global in nature and comprised of both affiliated and unaffiliated suppliers. As such, the complainants believe that their costs for given materials and components would be representative to that of the producers of subject goods. As a result, no adjustments were made to the complainants’ costs for raw materials.Footnote 29

[68] Direct labour costs were estimated based on the complainants’ projected labour costs with respect to a given bid. These labour costs included the engineering and design costs. The labour costs have been adjusted using a ratio of Canada’s labour costs to the labour costs in the named source. The complainants used labour data reported by the International Labour Organization (ILO) or, where recent data was not available through the ILO, by TradingEconomics.com.Footnote 30

[69] Overhead costs were estimated based on the complainants’ projected overhead costs with respect to a given bid. The complainants adjusted the labour component of overhead using the same methodology as for labour costs.Footnote 31

[70] The GS&A, financial expenses, other costs and amount for profit estimated by the complainants were estimated based on publicly available financial statements for companies producing SPT in the respective named sources. Where available, segment-specific financial statements were used. Where this level of detail was not available, consolidated financial statements were used.Footnote 32 The information and amounts by source are explained below.

[71] For Austria, the GS&A, financial expenses, other costs and an amount for profit were estimated based on amounts reported by Siemens Energy AGFootnote 33, in a publicly available segment-specific financial statements.

[72] For Chinese Taipei, the GS&A, financial expenses, other costs and an amount for profit were estimated based on publicly available financial statements of SPT producer in Chinese Taipei Shihlin Electric & Engineering Corp.Footnote 34

[73] For South Korea, the GS&A, financial expenses, other costs and an amount for profit were estimated based on publicly available financial statements of South Korean SPT producers Hyundai Electric & Energy Systems Co. Ltd.Footnote 35 and Iljin Electric Co. Ltd.Footnote 36

CBSA’s estimates

[74] The CBSA agreed with the complainants that it is difficult, if not impossible, to calculate normal values pursuant to section 15 of SIMA for small powered transformers. As previously mentioned, transformers are highly customized capital goods made to customer specifications, therefore, each transformer is unique and cannot be compared directly to another. As such, the CBSA found the complainants’ estimated normal values on the basis of paragraph 19(b) of SIMA for the named sources to be reasonable and representative estimates.

[75] The CBSA agreed that the complainants’ normal value estimates are reasonable and representative for the purposes of initiation. As a result, the methodology used by the complainants to estimate normal values under their cost-plus approach described above was accepted by the CBSA without any further adjustments.

[76] The complainants provided normal value estimates for 17 transaction-specific products that each represented a cost estimate for a competing bid to a customer during the POI. The CBSA used a selection of these products to estimate a normal value for products it found to be exported during the POI from the named sources.

[77] In order to estimate a normal value for an imported good, the CBSA derived a methodology to reasonably match the imported product to one of the 17 products for which the complainants had estimated a normal value. As a result, the CBSA was able to construct a number of unique normal values that could be matched to the imported goods from the named sources during the POI.Footnote 37

Export price

[78] The export price of goods sold to an importer in Canada is generally determined in accordance with section 24 of SIMA as being an amount equal to the lesser of the exporter’s sale price for the goods and the price at which the importer has purchased or agreed to purchase the goods adjusted by deducting all costs, charges, expenses, and duties and taxes resulting from the exportation of the goods.

[79] The complainants were unable to estimate all export prices using conventional methods, such as price lists and Statistics Canada data. This was due to the fact that SPT is a customized capital good and as such, producers do not maintain price lists. Also, given that there is a wide range of sizes and other key characteristics of the goods reported under the applicable tariff items, pricing information provided by Statistics Canada had only limited use.Footnote 38

[80] The complainants were, however, able to estimate export prices for a representative sample of SPT models using a combination of Statistics Canada import data, available bid results from Canadian public utilities, which were made accessible through procurement portals, and by industry feedback on subject goods sales corresponding with past imports that they themselves had placed bids on, where it was believed that the producers in the named sources had won a bid and where the goods have been or eventually will be shipped to Canada.Footnote 39

[81] Furthermore, the complainants indicated that the potential exporters and importers may be related, therefore, the complainants also estimated export prices, pursuant to section 25 of SIMA. Detailed information regarding the section 25 export price estimations cannot be divulged for confidentiality reasons.Footnote 40

[82] In estimating export prices for the purposes of initiation, the CBSA used the value for duty (VFD) and quantity reported in the Facility for Information Retrieval Management (FIRM) data for each individual shipment imported during the POI. The CBSA made adjustments to the FIRM data to correct errors and to remove non-subject imports from the database based on its review.

Estimated margins of dumping

[83] The CBSA estimated the margin of dumping for the named sources by comparing the total estimated normal values with the total weighted average estimated export prices. Based on this analysis, it is estimated that the subject goods imported into Canada from each of the named sources were dumped. The estimated margin of dumping for each source is listed in the table below.

| Place of export | Estimated margin of dumping |

|---|---|

| Austria | 28.8% |

| Chinese Taipei | 17.9% |

| South Korea | 66.6% |

Evidence of injury

[84] The complainants allege that the subject goods from Austria, Chinese Taipei and South Korea have been dumped, and that the dumping has caused and is threatening to cause material injury to the domestic industry in Canada.

[85] SIMA refers to material injury caused to the domestic producers of like goods in Canada. The CBSA has concluded that small power transformers produced by the domestic industry are like goods to the subject goods from the named countries.

[86] In support of their injury allegations, the complainants provided evidence of: a substantial increase in subject imports; price undercutting and lost sales; price depression; price suppression; and negative impacts on financial performance, the ability to raise capital, return on investments, and on production, capacity, and market share.

Substantial increase in subject importsFootnote 41

[87] According to the complainants’ estimated imports of subject goods, they indicated that there was a significant increase in imports between 2018 and 2020 in both absolute and relative terms, including a particularly large increase in 2019.

[88] In absolute terms, the complainants estimated that subject imports rose by 138% from $12.9 million in 2018 to $30.7 million in 2019. While estimated subject imports fell by 28% to $22.2 million in 2020, they remained 72% higher than the total estimated imports in 2018.

[89] The complainants also compared estimated subject imports in terms relative to domestic sales of small power transformers from their domestic production. They noted that estimated subject imports relative to domestic sales from domestic production increased significantly in 2019 compared to 2018 and that while the relative level decreased in 2020, it remained high in comparison to 2018.

[90] The CBSA’s estimated value of imports showed lower values of imports overall, but a similar trend to the complainants’ estimates, particularly for the 2018-2019 period. According to the data available to the CBSA, estimated subject imports rose by 43% in 2019 compared to 2018 and then decreased year-over-year by 37% in 2020.

[91] As previously noted, the CBSA’s estimated import values for subject goods appear lower given that a review of information relating to subject imports uncovered a number of imports that were misclassified as subject goods but that did not in fact meet the product definition. As such, those imports were removed from the CBSA’s import data.

[92] The CBSA also notes that small power transformers are capital goods that are customizable and sold based on particular specifications required by customers. Moreover, small power transformers are often ordered to form part of large multi-year projects and there is often a year or more of lead time between order and delivery of the goods to customers. As such, comparing imports on a year-to-year basis remains meaningful, but trends over a longer periods can also be considered.

[93] While estimated subject imports fell in 2020, the complainants submitted evidence of a substantial number of significant sales that were lost to exporters of subject goods in 2020. While those sales were lost in 2020, the subject goods will not be imported into Canada until 2021 or later. Based on evidence contained in the complaint, the complainants argued that imports are set to spike in 2021 and identified millions of dollars in committed shipments of subject imports for 2021.

[94] Based on the analysis of the evidence in the complaint and the CBSA’s own import data, the CBSA is of the opinion that the complainants’ evidence reasonably demonstrates that import volumes of the subject goods have increased in both absolute and relative terms between 2018 and 2020 and are projected to increase in 2021.

Price undercutting and lost salesFootnote 42

[95] The complainants claimed that they faced significant price undercutting by subject imports on major Canadian bids for small power transformers. To demonstrate price undercutting, the complainants provided a table summarizing the instances of price undercutting based on lost sales allegations contained in their sworn declarations, which they believe were lost to subject imports.

[96] The complainants noted that the customized nature of small power transformers and the misreporting in the Statistics Canada data concerning the quantities of small power transformers prevented them from being able to accurately compare average unit selling values of the subject imports with the domestic industry’s average selling prices. Alternatively, the complainants provided a table summarizing instances of lost sales based on account-specific information to demonstrate that subject imports have significantly undercut the price of like goods. Greater details regarding each instance were provided in sworn declarations from company representatives of the complainants, submitted as exhibits, and included additional evidence in the form of attachments which supported claims made in the declarations.

[97] The complainants’ summary table showed 38 examples of price undercutting on small power transformers based on lost sales between October 2017 and December 2020. Based on the estimated import prices provided in the summary table, the complainants showed that in many cases the price of subject imports significantly undercut the price of like goods.

[98] Based on the above and the CBSA’s analysis of the evidence contained in the complaint, the CBSA is of the opinion that the complainants’ evidence reasonably demonstrates the complainants have faced significant price undercutting and have lost sales, both which can reasonably be linked to the imports of the allegedly dumped subject goods.

Price depressionFootnote 43

[99] The complainants stated that they have been forced to lower their prices to compete against the allegedly dumped pricing of the subject goods, which have continued to undercut their selling prices as noted above. In the sworn declarations provided in the complainant, the complainants presented several examples where they quoted lower prices on projects, given they were competing against subject imports, and still lost those sales despite lower pricing.

[100] According to the complainants, the price depression is exemplified in their financial results. They noted that their combined gross profit margins fell significantly in 2019 in comparison to 2018. While the gross margin rose in 2020, the complainants noted that their combined gross profit margin in 2020 remained significantly lower than the gross profit margin in 2018. The complainants concluded that this performance is the direct result of being forced to make bids at very low gross margins to compete with the subject imports, which they consider to be the price leaders in the Canadian market.

[101] Based on the above and the evidence contained in the complaint, the CBSA is of the opinion that the complainants’ evidence reasonably demonstrates that the complainants were forced to reduce their prices in order to compete with imports of allegedly dumped subject goods.

Price suppressionFootnote 44

[102] The complainants indicated that the presence of the allegedly dumped subject goods have suppressed prices and prevented them from being able to raise prices in order to cover rising production costs. Based on the information provided, the complainants showed that the cost of goods manufactured (COGM) to net sales ratio increased in 2019 compared to 2018 and forced a significant cost-price squeeze. They also noted that while the COGM to net sales ratio fell in 2020, it remained at an elevated level demonstrating that the complainants remained unable to raise prices to cover the elevated costs.

[103] The complainants cautioned that MVA based comparisons are not ideal given the product mix, but highlighted that material, labour, and overhead costs on a per MVA basis all showed increased and elevated costs over the period.

[104] Despite MVA being an imperfect basis of comparison given uniqueness of each small power transformer sold, the CBSA noted that the complainants’ net sales, cost of goods sold (COGS), and gross profit, expressed on a per MVA, all showed similar trends as the individual production costs referenced by the complainants. The CBSA found that while net sales per MVA rose over the 2018-2020 period, they failed to keep up with rising costs and gross profit on a per MVA basis fell significantly over the same period.

[105] The evidence of price suppression provided by the complainants could also be linked to the presence of subject imports, particularly when considering 2019. In 2019, the value of subject imports more than doubled compared to 2018 and while complainants’ COGS per MVA increased significantly, the complainants net sales per MVA increased only slightly.

[106] Based on the above and the CBSA’s analysis of the evidence contained in the complaint, the CBSA is of the opinion that the complainants’ evidence reasonably demonstrates that prices were suppressed and could not be raised to cover rising costs as a result of having to complete with the allegedly dumped pricing of the imports of subject goods.

Negative impact on financial performanceFootnote 45

[107] According to the complainants, the allegedly dumped subject imports have negatively impacted their financial performance as a result of the complainants having to lower their prices in order to compete with the subject goods.

[108] According to the evidence submitted by the complainants, their gross profit and net income decreased in 2019 compared to 2018. While gross profit and net income increased in 2020, they both remained at a level lower than in 2018.

[109] The complainants also expect their financial results in 2021 to be negatively impacted as sales lost in 2020 have impacted their order books for 2021. They noted that having a healthy order backlog is critical to financial health, given small power transformer producers have high fixed costs and skilled workforces that require a steady forward-looking order book to remain viable.

[110] Based on the above and the CBSA’s analysis of the evidence contained in the complaint, the CBSA is of the opinion that the complainants’ evidence reasonably demonstrates that the imports of the allegedly dumped subject goods have had a negative impact on the complainants’ financial results.

Negative impact on ability to raise capitalFootnote 46

[111] The complainants stated that the negative impacts on financial performance experienced as a result of the importation of allegedly dumped subject goods have significantly impeded their ability to raise capital and provided confidential evidence in support of that statement.

[112] Based on the confidential evidence contained in the complaint, the CBSA is of the opinion that the complainants’ evidence reasonably demonstrates that their ability to raise capital has been significantly impeded by the negatively impacted financial performance, which has been linked to the imports of the allegedly dumped subject goods.

Negative impact on the return on investmentsFootnote 47

[113] The complainants stated that they have made significant investments in their production facilities and plan to make further investments in the future. That statement was supported with confidential details about past investments as well as future plans. The complainants indicated that the subject goods have had a negative impact on their return on their investments.

[114] Based on the confidential evidence contained in the complaint, the CBSA is of the opinion that the complainants’ evidence reasonably demonstrates that their rate of return on investments has been negatively impacted by the negatively impacted financial performance, which has been linked to the imports of the allegedly dumped subject goods.

Negative impacts on production, capacity, and market shareFootnote 48

[115] The complainants stated the trends in their capacity and production demonstrate that capacity utilization remains depressed despite efforts to secure throughput at any cost and use aggressive pricing to win bids. They noted that while production increased between 2018 and 2020, capacity utilization for the like goods decreased. They also pointed out that overall capacity utilization decreased for products produced on the same machinery and that excess capacity increased between 2018 and 2020.

[116] The CBSA analysed the production and capacity data provided by the complainants and found that while total production fell slightly in 2019, the decrease was mainly attributable to the production of other non-like goods. When focusing on the total production of like goods, production actually increased in 2019 compared to 2018, and increased slightly in 2020. When focusing on production of like goods for domestic sales only, production increased in both 2019 and 2020. As a result, there does not appear to be an obvious link between the importation of subject goods and a decline in the production of like goods sold in Canada, given that the production of like goods for sale domestically rose consistently over the 2018-2020 period.

[117] With respect to the slight but consistent decrease in capacity utilization noted by the complainants, the CBSA noted that total practical plant capacity consistently increased in both 2019 and 2020. As such, the decrease in capacity utilization over the 2018-2020 period appears to be more attributable to the increase in plant capacity than a decrease in total production given that production remained relatively flat over the period.

[118] The complainants also stated that they lost considerable market share due to the increasing presence of subject goods in the Canadian market. The complainants noted that subject imports significantly increased their market share in 2019 while the complaints lost a significant portion of their market share. The complainants also noted that in 2019, the total value of the market rose, showing that domestic industry not only lost market share but was unable to benefit from the increase in market demand. The complainants pointed out that domestic industry’s market share increased in 2020 but remained flat from 2018 to 2020 while subject import market share remained above 2018 levels.

[119] The CBSA’s estimated apparent Canadian market data included data for all domestic producers who provided information and not only the complainants’ share. The CBSA’s estimates showed a similar trend to the complainants’ estimates, particularly in 2019 where market share was lost to subject imports which had significantly increased compared to 2018. In 2020, the domestic industry’s market share increased while the market share attributable to subject imports decreased.

[120] Based on the above and the CBSA’s analysis of the evidence contained in the complaint, the CBSA is of the opinion that the complainants’ evidence of negative impacts on the their production and capacity utilization cannot reasonably be linked to the allegedly dumped subject goods.

[121] Based on the analysis of the evidence in the complaint and the CBSA’s own import data, the CBSA is of the opinion that the complainants’ evidence reasonably demonstrates that the imports of the allegedly dumped subject goods have had a negative impact on the complainants’ market share.

CBSA's conclusion-injury

[122] Overall, based on the evidence provided in the complaint and supplementary data available to the CBSA through its own research and customs documentation, the CBSA is of the opinion that the evidence discloses a reasonable indication that the allegedly dumped subject goods from Austria, Chinese Taipei, and South Korea have caused injury to the domestic industry in Canada in the forms of price undercutting and lost sales; price depression; price suppression; and negative impacts on financial performance, the ability to raise capital, return on investments, and on market share.

Threat of injury

[123] The complainants allege that the dumped goods threaten to cause further material injury to the domestic producers of small power transformers. The complainants provided the following information to support the allegation that imports of subject goods threaten to cause further injury to the Canadian industry.

Negatively impacted order backlog in 2021 and imminent imports of subject goodsFootnote 49

[124] The complainants noted that in Liquid Dielectric TransformersFootnote 50, the CITT recognized that having a healthy backlog or “plant loading” is critical to the financial health of power transformer manufacturers. The complainants submitted that the same is true of small power transformer manufacturers and that like other capital goods producers, they have high fixed costs and a skilled workforce which requires a steady forward-looking order book to be viable.

[125] The complainants stated that their negatively impacted backlog combined with sales lost to subject imports in 2020 to be delivered in the near future leave the domestic industry particularly vulnerable to injury. As a result of the negatively impacted backlog in 2021 and sales lost in 2020, they submitted that the threat of injury posed by the domestic industry’s significantly reduced plant loading is in of itself evidence that the alleged dumping of subject imports poses a threat to domestic industry.

[126] Based on the above and the evidence contained in the complaint, the CBSA is of the opinion that that the complainants’ evidence reasonably demonstrates that their negatively impacted order backlog in 2021, combined with the imminent importation of allegedly dumped subject goods into Canada, contributes to the possibility of a threat to the domestic industry.

Major upcoming blanket agreementsFootnote 51

[127] The complainants stated that as the domestic industry enters 2021 in a state of vulnerability, there are several important blanket agreements being issued and entered into over the next 12-24 months, which are critical to the future performance of the domestic industry. The complainants submitted that dumped imports threaten to injure the domestic industry for this reason alone. They noted that the CITT has previously recognized the importance of blanket agreements in the power transformers market.

[128] The complainants identified examples of upcoming large blanket agreements to be issued or renewed by major utilities across Canada and also cited examples in the past where they have had to aggressively compete on price with subject imports. The complainants stated that without anti-dumping protection in place, they will be forced to unfairly bid at lower prices to have a chance at being included in future blanket agreements. They argued that anti-dumping protection will cause the subject exporters to offer undumped prices, which will enable the complainants to achieve reasonable and fair prices.

[129] Based on the information presented in the complaint, the CBSA understands that blanket agreements are important to the power transformers market and can have an impact on financial performance. However, the information presented in that section of the complaint regarding this factor does not appear to clearly link the upcoming blanket agreements to the threat of injury. Overall, it appears the complainants are arguing that absent anti-dumping protection, the Canadian industry will be forced to drop prices if exporters continue to offer subject goods at dumped prices. As a result, the CBSA is of the opinion that upcoming blanket agreements as its own factor, as explained in the complaint, does not reasonably contribute to the possibility of a threat of injury.

Likelihood of substantially increased subject imports into CanadaFootnote 52

[130] The complainants stated that the CITT may consider a significant rate of increase of dumped goods imported into Canada as indicative of a likelihood of substantially increased imports to Canada. They reiterated that imports increased significantly over the 2018-2020 period, and noted that subject imports increased 138% in 2019 and in 2020 remained at a level nearly twice as high as in 2018.

[131] The complainants noted that, based on account specific examples, they have lost millions in sales to subject imports that are to be delivered in the near term. While the complainants submitted that these lost sales represent present injury, they claimed they are also an indication of an imminent significant increase in the volume of subject imports in 2021 and 2022.

[132] According to the complainants, the producers of subject goods have also become increasingly export oriented.

[133] With respect to South Korea, the complainants noted that Korean producer Iljin’s exports account for more than 50 percent of its total revenue. They also noted that Hyundai Electric announced plans to invest USD $33 million to expand production at its Alabama facility in the United States by 60%. In addition, the complainants pointed out that Hyosung Heavy Industries Corp (HICO) acquired a transformer plant in Tennessee in 2019 and committed to investing USD $103 million in that plant between 2020 and 2022. Accordingly, the complainants argued that any excess capacity that South Korean manufacturers (i.e. Hyundai Electric and HICO) now have due to lower volumes of transformer exports from South Korea to the US, due to expanded production in the US, will be diverted to other export markets, including Canada.

[134] The complainants stated that subject goods producers in Chinese Taipei are similarly export-oriented. They noted that both Shihlin’s and Fortune’s websites promoted the companies as global players looking to expand into overseas markets. They also noted that Fortune is listed as an “exporter” on Taiwan Trade; that Canada is identified as one of its main export markets; and that Fortune has even established a North American Division location in Pennsylvania from which it provides support to customer in Canada and the United States.

[135] Concerning Austria, the complainants noted that Siemens is a major global player in the transformers market and operates two large production plants in Austria in Linz and Weiz. The complainants also pointed out that in 2018, 51.5% of Siemens’ total revenue for all products came from exports outside of Europe. They noted that in a 2019 report, Siemens stated that sales to North America from its Linz plant has doubled since 2015. They also referenced a 2020 news article which stated that 80% of Linz’s production was destined for the export market.

[136] The complainants also submitted that the producers of subject goods have sufficient freely disposable capacity, indicating a likelihood of a substantial increase in exports. The complainants stated that there has been significant global overcapacity in the power transformers market since 2017 and that market conditions have not changed significantly since then to allow that overcapacity to be absorbed. In addition to the capacity expansions noted above, the complainants also noted that all liquid dielectric transformers are produced on the same equipment and while producers of medium and large power transformers can easily switch to producing small power transformers, the reverse is less likely given medium and large power transformers require significantly larger production plants.

[137] Based on the above and the evidence contained in the complaint, the CBSA is of the opinion that that the complainants’ evidence reasonably demonstrates that there is a likelihood of substantially increased subject imports into Canada in the near future, which contributes to the possibility of a threat to the domestic industry.

Domestic and international market conditionsFootnote 53

[138] The complainants submitted that the market conditions in the named sources will encourage exports to Canada and that Canada remains an attractive market for dumped subject goods.

[139] In relation to the global economy, the complaints noted that the World Bank’s January 2021 Global Economic Prospects projects worse economic outlooks over 2021 compared to previously already negative assessments. Also, given that the subject goods are used in a variety of energy related sectors, the complainants also noted that International Energy Agency found global energy demand declined by 5 percent over 2020 and projected global energy demand not to reach 2019 levels until 2022 at the earliest.

[140] With respect to South Korea, the complainants noted that in October 2019, prior to COVID-19, the International Monetary Fund (IMF) had projected South Korea’s economy to grow 2.2% in 2020. However, in its October 2020 Economic outlook, the IMF projected a 1.9% contraction in South Korea’s economy in 2020 followed by projected growth of 2.9% in 2021. The IMF’s outlook also showed that projected growth for South Korea in 2021 is below many other countries in the region (e.g. China, India, Australia, etc.). The complainants also noted that major transformer end-user sectors in South Korea are struggling, including the industrial power and construction sectors.

[141] According to 2020 second quarter report by Hyundai Electric, there was a 205% increase in the value of their exports. That report indicated that the company’s overall exports of power equipment increased from KRW $30.6 million to KRW $93.2 billion and noted that power equipment exports to North America and Europe had increased in the quarter. While the company noted that third quarter 2020 export revenue had declined, the year-over-year decline in North American sales were due to base effects such as inflation and not a market decline.

[142] With respect to Chinese Taipei, the complainants noted that in October 2019, prior to COVID-19, the IMF had projected Chinese Taipei’s economy to grow 1.92% in 2020. However, in IMF’s April 2020 Economic outlook, the IMF projected a 4% contraction in Chinese Taipei’s economy in 2020, followed by projected growth of 3.5% in 2021.

[143] The complainants noted that Shihlin’s monthly sales report for 2019 and 2020, as published on its website, showed that overall sales declined by 1% in 2020, year-over-year. They also pointed out that if the drastic 30% increase in sales in December 2020 is ignored, as they suggest those sales may be related to annual inventory offload, the overall sales at Shihlin in 2020 decreased by 4%.

[144] With respect to Austria, the complainants noted that in October 2019, prior to COVID-19, the IMF had projected Austria’s economy to grow 1.7% in 2020. However, in IMF’s October 2020 Economic outlook, the IMF projected a 6.7% contraction in Austria’s economy in 2020 followed by projected growth of 4.7% in 2021. The complainants also indicated that like South Korea, the European construction sector is struggling. The complainants noted that EUROFER reported a drop of 5.7% in European Union construction output in 2020 and forecast output to rebound by only 4.3% in 2021.

[145] With respect to Canada, the complainants noted that the IMF’s October 2020 Economic outlook projected a 7.1% contraction in Canada’s economy followed by projected growth of 5.2% in 2021.

[146] According to the complainants, the end-user markets for Canadian transformers, such as the electricity and renewable energy sectors, were among the least affected by the economic slowdown. The complainants noted that COVID-19 had a minimal impact on residential electricity demand, which was in fact the only type of energy to see an increase in 2020. The complainants noted that the minimal impact of the pandemic is evidenced by the continuation of planned tenders and steady purchases of like goods in Canada in 2020 as well as the projected sales of like goods into 2021 and 2022.

[147] The complainants also noted that reports issued prior to the pandemic, which have not yet been updated, stated that the National Energy Board, the Association de l’Industrie Électrique du Québec, and the Canada Energy Regulator projected demand for electricity generation in Canada to increase beyond 2030. The complainants also pointed out that the Canadian Electricity Association expects capital expenditures in new electrical infrastructures, including transformers, to exceed $350 billion over the next 20 years.

[148] Moving forward, with electricity generation expected to increase and resulting in greater demand for power transformers, the Canadian market for small power transformers will likely remain an attractive export market. Given the market conditions in the domestic and key export markets of the producers of subject goods, the complainants submitted that not only will subject producers’ interest in the Canadian market remain, there will be additional motivation to export to Canada over the next 12-24 months.

[149] Based on the above and the evidence contained in the complaint, the CBSA is of the opinion that that the complainants’ evidence reasonably demonstrates that domestic and international market conditions could result in greater interest in the Canadian market from the producers of the allegedly dumped subject goods, which contributes to the possibility of a threat to the domestic industry.

Likelihood of subject goods having a significant depressing or suppressing effect on the price of like goods in CanadaFootnote 54

[150] The complainants noted that the subject goods significantly undercut and depressed domestic industry prices based on the evidence presented in complaint. They submitted that such negative price effects caused by the subject goods would significantly worsen in the next 12-24 months, particularly when examined in the context of the complainants’ negatively impacted order backlog. As a result, the complainants contended that absent anti-dumping protection, subject imports will continue to and increasingly cause negative price effects in the Canadian market over the next 12-24 months.

[151] Based on the evidence contained in the complaint, the CBSA is of the opinion that the complainants’ evidence reasonably demonstrates that there is a likelihood of subject goods having a significant depressing or supressing effect on the price of like goods in Canada, which contributes to the possibility of a threat to the domestic industry.

Measures in Force in other jurisdictionsFootnote 55

[152] The complainants noted that in November 2019, Australia extended its anti-dumping measure against Chinese Taipei that was originally put in place in 2014. The goods subject to that measure are liquid dielectric power transformers with power ratings of equal to or greater than 10 MVA and a voltage rating of less than 500kV and the rate of duty ranges from 7.6% to 8.8%.

[153] They also indicated that Argentina extended its anti-dumping measure against South Korea in November 2019 that was originally put into place in 2014. The goods subject to that measure are three-phase liquid dielectric transformers with power greater than 10,000 kVA but not exceeding 600,000 kVA and the rate of duty is 52%.

[154] The complainants also noted that the United States has a measure in place against large power transformers from South Korea that was extended in 2018. While it does not include small power transformers, the complainants pointed out that large power transformer producers can easily shift production to small power transformers.

[155] In addition to the anti-dumping measures, the complainants stated that in May 2020, the United States had initiated a Section 232 investigation on stacked and wound cores incorporated into transformers. The complainants submitted that should subject producers face restrictions as a result of the Section 232 investigation, it will provide additional incentive for those producers to export to Canada.

[156] The complainants concluded that the existence of the anti-dumping measures in other jurisdictions as well as the ongoing Section 232 investigation are evidence of the propensity of subject exporters to engage in injurious dumping and represents a risk of increased diverted exports to Canada.

[157] Based on the above, the CBSA is of the opinion that that the complainants’ evidence reasonably demonstrates that the measures in other jurisdiction could lead to the increased diversion of subject exports to Canada, which contributes to the possibility of a threat to the domestic industry.

Magnitude of the margin of dumpingFootnote 56

[158] The complainants submitted that the magnitude of their estimated dumping margins; 12.1% for Austria; 12.5% to 46.9% for Chinese Taipei; 7.9% to 55.8% for South Korea; indicate that the threat posed by the dumped subject goods is real, foreseeable, and imminent.

[159] The CBSA’s estimated weighted average margins of dumping for the named sources are 28.8% for Austria, 17.9% for Chinese Taipei, and 66.6% for South Korea. These estimated weighted average margins are comparable in terms of magnitude to the range of margins estimated by the complainants on individual transactions.

[160] Based on the above, the CBSA is of the opinion that that the complainants’ evidence reasonably demonstrates that the subject goods contribute to the possibility of a threat to the domestic industry, given the magnitude of the estimated margins of dumping for each of the named sources.

CBSA's conclusion-threat of injury

[161] The CBSA is of the opinion that the evidence disclosed in the complaint reasonably indicates that imports of allegedly dumped subject goods pose a threat of injury to the domestic industry based on a negatively impacted order backlog in 2021 and imminent imports of subject goods; the likelihood of a substantial increase in subject imports; domestic and international market conditions; the likelihood of subject goods having a significant depressing or suppressing effect on the price of like goods in Canada; measures in force in other jurisdictions; and the magnitude of the margin of dumping.

Causal link-dumping and injury/threat of injury

[162] The CBSA finds that the complainants have reasonably linked the injury they have suffered to the alleged dumping of subject goods imported into Canada. The injury includes price undercutting and lost sales; price depression; price suppression; and negative impacts on financial performance, the ability to raise capital, return on investments, and on market share.

[163] The complainants submitted that the continued dumping of goods from the named sources will cause further injury to the Canadian domestic industry in the future. As discussed above, the CBSA is of the opinion that the evidence disclosed in the complaint reasonably indicates that imports of allegedly dumped subject goods pose a threat of injury to the domestic industry.

[164] In summary, the CBSA is of the opinion that the evidence submitted by the complainants has disclosed a reasonable indication that the alleged dumping has caused injury and is threatening to cause injury to the Canadian domestic industry.

Conclusion

[165] Based on information provided in the complaint, other available information, and the CBSA’s import documentation, the CBSA is of the opinion that there is evidence that SPT originating in or exported from Austria, Chinese Taipei and South Korea have been dumped. Further, there is a reasonable indication that such dumping has caused and is threatening to cause injury to the Canadian industry. As a result, pursuant to subsection 31(1) of SIMA, a dumping investigation was initiated on April 15, 2021.

Scope of the investigation

[166] The CBSA is conducting an investigation to determine whether the subject goods have been dumped.

[167] The CBSA has requested information from all potential exporters and importers to determine whether or not subject goods imported into Canada during the POI of July 1, 2019 to December 31, 2020, were dumped. The information requested will be used to determine the normal values, export prices and margins of dumping, if any.

[168] All parties have been clearly advised of the CBSA’s information requirements and the time frames for providing their responses.

Future action

[169] The CITT will conduct a preliminary inquiry to determine whether the evidence discloses a reasonable indication that the alleged dumping of the goods has caused or is threatening to cause injury to the Canadian industry. The CITT must make its decision on or before the 60th day after the date of the initiation of the investigation. If the CITT concludes that the evidence does not disclose a reasonable indication of injury to the Canadian industry, the investigation will be terminated.

[170] If the CITT finds that the evidence discloses a reasonable indication of injury to the Canadian industry and the CBSA’s preliminary investigation reveal that the goods have been dumped, the CBSA will make preliminary determinations of dumping within 90 days after the date of the initiation of the investigation, by July 14, 2021. Where circumstances warrant, this period may be extended to 135 days from the date of the initiation of the investigation.

[171] Under section 35 of SIMA, if, at any time before making a preliminary determination, the CBSA is satisfied that the volume of goods of a country is negligible, the investigation will be terminated with respect to goods of that country.

[172] Imports of subject goods released by the CBSA on and after the date of a preliminary determination of dumping, other than goods of the same description as goods in respect of which a determination was made that the margin of dumping of the goods is insignificant, may be subject to provisional duty in an amount not greater than the estimated margin of dumping on the imported goods.

[173] Should the CBSA make a preliminary determination of dumping, the investigation will be continued for the purpose of making final decisions within 90 days after the date of the preliminary determinations.

[174] After the preliminary determination, if, in respect of goods of a particular exporter, the CBSA’s investigation reveal that imports of the subject goods from that exporter have not been dumped, or that the margin of dumping is insignificant, the investigation will be terminated in respect of those goods.

[175] If a final determination of dumping is made, the CITT will continue its inquiry and hold public hearings into the question of material injury to the Canadian industry. The CITT is required to make a finding with respect to the goods to which the final determination of dumping applies, not later than 120 days after the CBSA’s preliminary determination.

[176] In the event of an injury finding by the CITT, imports of subject goods released by the CBSA after that date will be subject to anti-dumping duty equal to the applicable margin of dumping on the imported goods.

Retroactive duty on massive importations

[177] When the CITT conducts an inquiry concerning injury to the Canadian industry, it may consider if dumped goods that were imported close to or after the initiation of an investigation constitute massive importations over a relatively short period of time and have caused injury to the Canadian industry.

[178] Should the CITT issue such a finding, anti-dumping duties may be imposed retroactively on subject goods imported into Canada and released by the CBSA during the period of 90 days preceding the day of the CBSA making a preliminary determination of dumping.

Undertakings

[179] After a preliminary determination of dumping by the CBSA, other than a preliminary determination in which a determination was made that the margin of dumping of the goods is insignificant, an exporter may submit a written undertaking to revise selling prices to Canada so that the margin of dumping or the injury caused by the dumping is eliminated.

[180] An acceptable undertaking must account for all or substantially all of the exports to Canada of the dumped goods. Interested parties may provide comments regarding the acceptability of undertakings within nine days of the receipt of an undertaking by the CBSA. The CBSA will maintain a list of parties who wish to be notified should an undertaking proposal be received. Those who are interested in being notified should provide their name, telephone and fax numbers, mailing address and e-mail address to one of the officers identified in the “Information” section of this document.

[181] If undertakings were to be accepted, the investigation and the collection of provisional duties would be suspended. Notwithstanding the acceptance of an undertaking, an exporter may request that the CBSA’s investigation be completed and that the CITT complete its injury inquiry.

Publication

[182] Notice of the initiation of this investigation is being published in the Canada Gazette pursuant to subparagraph 34(1)(a)(ii) of SIMA.

Information

[183] Interested parties are invited to file written submissions presenting facts, arguments, and evidence that they feel are relevant to the alleged dumping. Written submissions should be forwarded to the attention of the SIMA Registry and Disclosure Unit.

[184] To be given consideration in this investigation, all information should be received by the CBSA by August 24, 2021.

[185] Any information submitted to the CBSA by interested parties concerning this investigation is considered to be public information unless clearly marked “confidential”. Where the submission by an interested party is confidential, a non-confidential version of the submission must be provided at the same time. This non-confidential version will be made available to other interested parties upon request.

[186] Confidential information submitted to the CBSA will be disclosed on written request to independent counsel for parties to these proceedings, subject to conditions to protect the confidentiality of the information. Confidential information may also be released to the CITT, any court in Canada, or a WTO or Canada-United States-Mexico Agreement (CUSMA) dispute settlement panel. Additional information respecting the CBSA’s policy on the disclosure of information under SIMA may be obtained by contacting the SIMA Registry and Disclosure Unit or by visiting the CBSA’s website.

[187] The schedule of the investigation and a complete listing of all exhibits and information are available at on the CBSA's website. The exhibit listing will be updated as new exhibits and information are made available.